Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

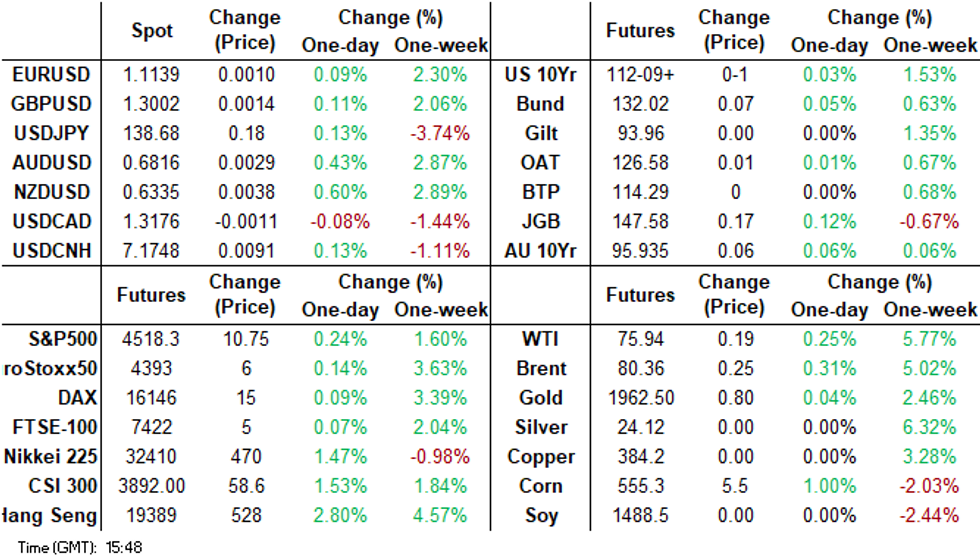

- Cash tsys sit 4bps richer to 1bp cheaper across the major benchmarks, the curve has twist steepened pivoting on 20s. The short end of the curve marginally extended its move seen post US CPI yesterday. This has weighed on broader USD sentiment, although USD/JPY dips have been supported today. Yen is down noticeably against the likes of NZD and AUD amid supportive risk appetite in the equity space.

- Weaker China June trade figures haven't deterred broader risk appetite, although commodity imports look to be holding up. Like USD/JPY, USD/CNH dips have been supported, weighing on the yuan from a NEER standpoint. The BoK left rates at 3.50%, as widely expected.

- Looking ahead, in Europe today May's GDP release from the UK provides the highlight. Further out we have June PPI and Weekly Initial Jobless Claims. Fedpseak from SF Fed President Daly crosses. We also have the latest 30-Year Supply.

MARKETS

US TSYS: Curve Marginally Steeper In Asia

TYU3 deals at 112-11, +0-02+, a touch off the top of the 0-05 range on volume of ~65k.

- Cash tsys sit 4bps richer to 1bp cheaper across the major benchmarks, the curve has twist steepened pivoting on 20s.

- The short end of the curve marginally extended its move seen post US CPI yesterday, TU sits above Wednesday's high.

- Ranges were narrow with little follow through on moves for the majority of the session. Little meaningful macro news flow crossed in Asia today.

- In Europe today May's GDP release from the UK provides the highlight. Further out we have June PPI and Weekly Initial Jobless Claims. Fedpseak from SF Fed President Daly crosses. We also have the latest 30-Year Supply.

STIR: $-Bloc Markets Softens After US CPI Miss, BoC Hikes

$-Bloc STIR softens after lower than anticipated US CPI data, despite a 25bp hike from the BoC.

- US headline inflation declined from 4% y/y to 3% y/y (3.1% est) in June, marking the slowest rate of inflation since March 2021. Core inflation also fell short of expectations at 4.8% y/y with core services ex-rent printing a modest annualized growth rate of 2.9% during the three months leading up to June.

- The CPI report led the market to think that the forthcoming 25bp hike from the Federal Reserve would be the final one. The market places the chance of a July Fed hike at 90%, but the odds of further hikes softened. November cumulative tightening eased to 29bp from 35bp.

- BoC Governor Macklem said Wednesday he's getting close to rebalancing the economy with monetary policy restraining a stronger-than-expected expansion, and it "made sense" to pause rate hikes earlier this year before returning this week with a second straight tightening, as generally expected. Terminal rate expectations were little changed at 5.13%.

- RBNZ dated OIS pricing is 1-7bp softer across meetings today, with terminal OCR expectations at 5.56% versus 5.69% before yesterday’s decision by the RBNZ to leave policy unchanged.

- RBA-dated OIS pricing is 4-9bp softer beyond November with terminal rate expectations at 4.44%, the lowest since early June.

Figure 1: $-Bloc STIR: Terminal Rate Expectations & Mar’24 Pricing

Source: MNI – Market News / Bloomberg

JGBS: Futures Holding Stronger, Range Bound Tokyo Session Despite Solid Demand For 20Y Supply

JGB futures are richer, +22 compared to settlement levels, but have pared their gains in the Tokyo afternoon session. This comes despite today’s 20-year supply showing stronger demand.

- As mentioned in our preview, today's auction likely benefited from factors such as a higher outright yield, a steeper 10/20 yield curve, and the 20-year bond becoming relatively cheaper in relation to the 10/20/30-year butterfly. The allure of a new bond issue might have also played a role.

- Bloomberg reports that 10-year OIS, popular with international funds, have climbed well beyond the central bank’s ceiling for equivalent yields. That’s a sign that at least some market players think the BOJ may choose to reshape its policy of holding down 10-year yields. (See link)

- Cash JGBs exhibit a mixed performance along the yield curve, with the futures-linked 7-year zone, outperforming (1.3bp richer), while the 40-year zone underperforms (1.5bp cheaper).

- The 20-year zone is 0.8bp richer, after richening around 3bp in early post-auction trade.

- The swaps curve twist steepened, pivoting at the 20-year. Swap spreads are tighter across the curve, apart from the 7-year.

- Tomorrow the local calendar sees Industrial Production and Capacity Utilisation data for May along with BoJ Rinban operations covering 1-10-year and 25-Year+ JGBs.

AUSSIE BONDS: Sharply Richer, Narrow Range In Sydney Session, US PPI Due

ACGBs are holding sharply richer (YM +10.0 & XM +7.0) in a narrow range in the Sydney session after tracking US tsys stronger following the release of lower-than-expected US CPI data. Without meaningful domestic drivers, local market participants have been on US tsys watch ahead of June US PPI and weekly Jobless Claims data later today.

- US cash tsys sit 4bp richer to 1bp cheaper across the major benchmarks, with the curve twist steepening, pivoting on 20s. The short end of the curve marginally extended its move seen post-US CPI yesterday, Ranges have been narrow with little follow-through on moves for the majority of the session. Little meaningful macro news flow crossed in Asia today.

- Cash ACGBs are 7-9bp richer with the AU-US 10-year yield differential +3bp at +21bp.

- Swap rates are 5-8bp lower with the 3s10s curve steeper.

- The bills strip bull steepens with pricing +3 to +11.

- RBA-dated OIS pricing is 4-10bp softer for meetings beyond August.

- (ABC) Opposition Leader Peter Dutton says two of the government's potential picks to replace Philip Lowe as Reserve Bank governor would not be able to operate independently because of their established relationships with the government. (See link)

- Tomorrow the local calendar sees no data.

NZGBS: Closed On A Positive Note, Solid Demand Seen At Weekly Auction

NZGBs closed on a strong note with benchmark yields 9-11bp lower despite retail card spending rising 1% m/m in June versus -1.7% in May. Core retail card spending was however unchanged m/m. Food prices rose 1.6% in June versus +0.3% prior, while Business NZ manufacturing PMI declined to 47.5 from a revised 48.7.

- Today’s weekly auction saw solid demand for the May-31 and May-51 lines with cover ratios of 3.35x and 3.71x respectively. The cover ratio for the May-26 bond was 2.49x. The longer-dated cash lines were 2-4bp richer post-auction.

- NZ-US and NZ-AU 10-year yield differentials closed 1bp and 3bp tighter respectively.

- Swap rates closed 7-11bp lower with the 2s10s curve 1bp flatter and implied swap spreads wider.

- RBNZ dated OIS closed 6-14bp softer for meetings beyond October with terminal OCR expectations at 5.64%.

- Bloomberg reports that economists have called an end to New Zealand’s housing slump, saying the latest data show the market has found a floor and prices are starting to recover. A REINZ report released Thursday in Wellington showed house prices rose 0.4% in June while sales continued to recover. (See link)

- Tomorrow is a public holiday in NZ.

- Later today sees the market attention tuned to June US PPI and US Jobless Claims data.

FOREX: Greenback Pressured In Asia

The post-CPI move lower in the USD has marginally extended in Asia on Thursday, BBDXY has breached post CPI lows and sits down ~0.15%.

- Kiwi is the strongest performer in the G-10 space at the margins. NZD/USD is up ~0.5%, the pair last prints at $0.6325/30. Bulls now target the high from 11 May ($0.6385).

- AUD/USD is ~0.4% firmer, the pair has extended gains through the session and sits at session highs. A move above 0.6828 a retracement level, would open up mid June highs around 0.6900.

- Yen is little changed, USD/JPY briefly dealt below its post CPI lows before support was seen and losses were pared.

- Elsewhere in G-10 EUR and GBP are ~0.2% firmer and CHF printed its highest level in 8 years. USD/CHF sits at 0.8650/60.

- Cross asset wise; regional equities and US equity futures are firmer benefitting from the improving risk sentiment. Hang Seng is up ~2.5% and e-minis are up ~0.3%. 2 Year US Tsy Yields are ~4bps lower.

- In Europe today we have May GDP from the UK, further out US PPI and Initial Jobless Claims cross.

JAPAN DATA: Local Investors Sell Foreign Bonds & Stocks

Japan weekly investment flows showed further inflows into local stocks from offshore investors. ¥181.7bn came into local stocks, following last week's +¥195bn last week, see the table below. Offshore flows into local bonds were stronger at ¥705bn, which follows last week's ¥485bn in inflows. The flows to end July 7 was the strongest since mid-May.

- In terms of Japan outbound flows, we saw -¥951bn in terms foreign stock selling, and -¥950.5bn in terms of foreign bonds. The selling of foreign stocks was the largest since mid-April.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending July 7 | Prior Week |

| Foreign Buying Japan Stocks | 181.7 | 195 |

| Foreign Buying Japan Bonds | 705.0 | 484.7 |

| Japan Buying Foreign Bonds | -950.5 | 1252.7 |

| Japan Buying Foreign Stocks | -951.0 | -158.9 |

Source: MNI - Market News/Bloomberg

EQUITIES: Strong Gains For Most Asia Pac Indices On Positive Wall St Spillover/China Optimism

Asia Pac equities are virtually a sea of green in Thursday trade. At this stage only Indonesian markets are tracking lower within the region. The HSI is the strongest performer, while US futures have seen positive gains so far. Eminis were last near 4518, +0.24% for the session, building on positive momentum from Wednesday's US session. Nasdaq futures are outperforming, +0.40%, showing greater sensitivity to lower US yield moves.

- Outside of positive global equity sentiment post the US CPI miss, HK and China shares have also been buoyed by the focus of the authorities on stimulating the private sector. This follows meetings between senior China tech officials and China's Premier. President Xi Jinping has also stated the country should open up to more foreign investment earlier in the week.

- At the break, the HSI is up 2.49%, with the tech sub-index +3.43%. The China Enterprise index is +2.48% higher, while the CSI 300 is +1.12% higher at the break.

- Tech sensitive plays are doing better elsewhere as well, the Taiex +1.40%, the Kospi slightly weaker at +0.80%, but the Kosdaq is +1.50%. Japan shares are also up +1.5% for Nikkei 225.

- In SEA trends are slightly more mixed. Singapore stocks are +1.60%, but flat in Malaysia. Thailand shares are a touch higher, as the market focuses on the parliament PM vote. Indonesian shares are down a touch.

OIL: Brent Consolidates Above $80/bbl

Brent crude has spent most of the session pushing higher. We were last in the $80.40/45/bbl region, with highs at $80.54/bbl, against an earlier low near $80/bbl. This puts us +0.40% higher for the session and follows Wednesday's aggregate gain of 0.89%. At this stage, Brent is tracking comfortably higher for the week. WTI is currently at $76/bbl, which is +0.34% firmer for the session.

- The technical back drop looks positive for oil, as Brent consolidates gains above the $80/bbl level. Late April highs just above $83/bbl may present as the next upside target, although the 200-day EMA around $82.30/bbl has to be cleared first.

- China June trade data showed solid y/y gains for crude oil (+11.7% and oil product (+44.7%) imports in volume terms. This may help sentiment at the margin.

- Looking ahead we have the IEA and OPEC oil market reports on tap.

GOLD: 3-Week High After US CPI Undershoot

Gold is +0.2% in the Asia-Pac session, after rising to the highest in three weeks following lower-than-expected US inflation data. The CPI report fuelled speculation that the forthcoming 25bp hike from the Federal Reserve would be the final one. The market places the chance of a July Fed hike at 90%, but the odds of further hikes softened. November cumulative tightening eased to 30bp from 35bp.

- US headline inflation declined from 4% to 3% in June, marking the slowest rate of inflation since March 2021. The market expected 3.1%. Core inflation also fell short of expectations, printing 4.8%. The decrease was primarily driven by softer airfare, hotel costs, and a decline in used vehicle prices. Notably, prices for core services ex-rent experienced a modest annualized growth rate of 2.9% during the three months leading up to June.

- The dollar and US tsy yields dropped following the report, boosting bullion, which closed 1.3% higher.

CHINA DATA: Export & Imports Weaker Than Forecast, But Commodity Imports Firm

China headline exports were weaker than expected in June (in USD terms). We printed at -12.4% y/y, versus -10.0% forecast and -7.5% prior. This is the weakest y/y print since early 2020. On the import side, we were also a touch weaker than expected, -6.8% y/y in USD terms, against a -4.1% forecast and -4.5% prior. This left the trade balance at $70.62bn, versus a consensus estimate of $74.90bn.

- The export result is arguably not that surprising, given trends elsewhere in Asia, although South Korea is showing some signs of export growth basing, see the chart below (China is the pink line).

- This and the fact that the CNY NEER is already at cyclical lows, may be limiting the initial fall out for CNH, which hasn't seen any material selling pressure post the data prints (last around 7.1700/10). Broader USD trends, post the CPI print on Wednesday are also dominating to some extent.

- On the import side, despite the headline miss, commodity imports appear to be holding up reasonably well. Iron ore +7.7% y/y, copper +7.9% y/y and crude oil +11.7% y/y. Coal is also up very storngly, over 90% y/y. This may give some sense that the domestic demand backdrop is not faltering too rapidly.

Fig 1: China Exports Weaken, In Line With Other NEA/Export Orientated Economies

Source: MNI - Market News/Bloomberg

BOK: Maintaining A Restrictive Stance For A Considerable Time

The BoK statement continued to push back against any near term notion of rate cuts. The central bank stated that: "The Board, therefore, will maintain a restrictive policy stance for a considerable time with an emphasis on ensuring price stability." In assessing whether to tighten rates further, the board will consider the pace of the inflation slowdown, financial stability risks, the impact of previous tightening's, and the monetary policy changes in major economies.

- In terms of the inflation backdrop, the board noted evolution of headline inflation is consistent with the May forecast of 3.5%. However, core inflation is set to be slightly higher than the 3.3% forecast. The central bank stated that "Although inflation has slowed, it is forecast to pick up again to around the 3% level since August and to remain above the target level for a considerable time."

- On the economy, the domestic backdrop has improved somewhat, but the recovery is expected to be gradual. For this year, GDP growth is consistent with the May forecast of 1.4%.

- The global economy has proven more resilient than expected, but is still expected to slow gradually.

ASIA FX: CNH Underperforms Further USD Weakness

Most USD/Asia pairs are lower, although USD/CNH has rebounded from fresh lows, as the fixing bias was tempered and trade figures disappointed. Spot KRW and MYR are up around 1% against the USD. THB has also recovered some ground but is still lagging broader USD trends. Spot INR is also showing a lower beta to USD weakness. Still to come is the Thai parliamentary PM vote. Tomorrow, Indian wholesale prices and trade figures print, along with South Korean money supply data. Singapore Q2 GDP is also out.

- USD/CNH sits above session lows, last in the 7.1740/50 region. The rough range for the session has been 7.16/7.18. CNH has underperformed despite a strong onshore equity tone and softer USD sentiment elsewhere. We had weaker than expected June trade figures, although the direct impact on CNH has been limited so far. The CNY fixing was firmer than forecast, but the miss narrower than the first part of July.

- 1 month USD/KRW hasn't been able to break sub 1270 so far today, although earlier moves above 1277 drew selling interest. The BoK left rates on hold at 3.50% as expected. The central bank expects to stay restrictive for some time. The statement and Governor Rhee's speech were slightly hawkish, as the bank left the door ajar for another rate hike and stated core inflation was slightly firmer than expected compared to May estimates.

- USD/THB got to fresh lows near 34.50, but has rebounded back to 34.64/65 since. The baht is lagging broader USD trends, as the market awaits the outcome of the parliamentary PM vote. Pita has been the only candidate put forward at this stage. The vote is scheduled for 5pm local time.

- The Rupee has firmed in early dealing as softer US CPI and a firmer than expected Indian CPI print weigh on USD/INR. The pair now sits a touch above the 82 handle printing its lowest level since 4 July. USD/INR is ~0.2% lower than Wednesday's closing levels. Indian CPI rose in June and was firmer than expected, printing at 4.81% Y/Y vs 4.60% exp ticking higher from May's print which was a 25-month low. The uptick in CPI may delay any potential rate cuts as RBI will have to wait longer for CPI to reach the mid-point of its 2-6% target band. Also on the wires yesterday was May Industrial Production which rose to 5.2% Y/Y from 4.2% in April.

- Weaker than forecast US CPI which crossed after yesterdays close is weighing on USD/MYR in early trade. The pair last prints at 4.6000/50 and is down ~1.1% thus far. On the wires yesterday May Industrial Production printed at 4.7% Y/Y, a print of 0.0% had been expected. Manufacturing Sales Value rose 3.3% Y/Y in the month. Looking ahead the data local calendar is empty until June Trade Balance which crosses next Thursday.

- The SGD NEER (per Goldman Sachs estimates) has retreated from fresh cycle highs, printed in the aftermath of yesterday's US CPI print, to sit a touch softer in early trade on Wednesday. We sit ~0.5% below the top of the band. Broad based USD weakness post US CPI saw USD/SGD fall ~0.7% to print a fresh month to date low, the pair sits on the $1.33 handle and is at its lowest level since 11 May. Looking ahead; on the wires early tomorrow we have the Advance Q2 GDP print, a fall of 0.2% Q/Q is expected.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/07/2023 | 0600/0700 | ** |  | UK | UK Monthly GDP |

| 13/07/2023 | 0600/0700 | ** | | UK | Index of Services |

| 13/07/2023 | 0600/0700 | *** | | UK | Index of Production |

| 13/07/2023 | 0600/0700 | ** | | UK | Trade Balance |

| 13/07/2023 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 13/07/2023 | 0645/0845 | *** |  | FR | HICP (f) |

| 13/07/2023 | 0900/1100 | ** |  | EU | Industrial Production |

| 13/07/2023 | - | *** |  | CN | Trade |

| 13/07/2023 | - | | EU | ECB Lagarde & Panetta in Eurogroup Meeting | |

| 13/07/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 13/07/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 13/07/2023 | 1230/0830 | *** | | US | PPI |

| 13/07/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 13/07/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 13/07/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 13/07/2023 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 13/07/2023 | 1800/1400 | ** | | US | Treasury Budget |

| 13/07/2023 | 2245/1845 | | US | Fed Governor Christopher Waller |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.