Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

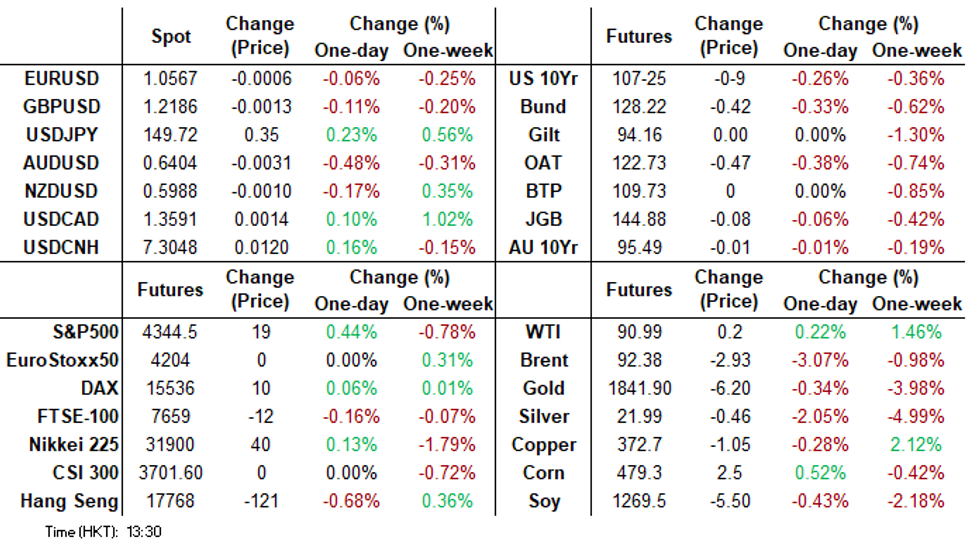

- US Tsy Yields ticked higher after an agreement in US Congress to avert a government shutdown passed over the weekend. The Senate voted to pass the bill on a 88 to 9 margin after the House had voted 335-91. The deal funds govt to the 17 November 2023.

- There was spillover to regional fixed income with Kiwi Bonds and JGBs pressured. Trading in ACGBs was limited due to the NSW holiday, cash markets were closed and futures observed narrow ranges. The USD was a touch firmer, however gains have been trimmed in recent trade.

- In the equity space Asian equity markets are mixed today but S&P e-minis are up 0.6% and NASDAQ +0.7%. China, HK and India are all closed for holidays as is most of Australia, although the ASX is open. China is closed all week.

MARKETS

US TSYS: Cheaper In Asia

TYZ3 deals at 107-25, -0-09, a 0-08 range has observed on volume of ~93k.

- Cash tsys sit ~4bps cheaper across the major benchmarks.

- Tsys were pressured in early trade after an agreement in US Congress to avert a government shutdown passed over the weekend.

- Narrow ranges were observed for the remainder of the session with little follow through on moves. There was no meaningful macro news flow.

- On the wires today we have the final read of S&P Global Mfg PMI for September as well as the latest ISM Mfg Survey. There are a number of Fed speakers today including Fed Chair Powell and NY Fed President Williams.

JGBs: Losses Pared On BOJ Bond Buying

JGB Futures pared losses in recent trade after an announcement from the BOJ that they will conduct additional bond buying for 5-10 Year JGBs on October 4.

- This leaves JB1 at 144.83, -0.13, the contract has recovered off its session low at 144.76 after ticking lower from opening levels through the session as spillover from US Tsys weighed.

- The 10 Year Yield is unchanged at 0.76%, with other major benchmarks 1-3bps cheaper.

- Looking ahead, the data docket is relatively light this week. Labor Cash earnings on Friday are the highlight.

- On the supply side tomorrow we have a Y2.7tn 10 Year Bond Auction and on Thursday Y900bn of 30-Year JGBs will come to market.

AUSSIE BONDS: Cash Closed Today, Muted Session For Futures

XM and YM observed narrow ranges today with little follow through on moves. Cash was closed today due to the holiday in NSW.

- XM sits at 95.475, -0.025, and YM at 95.88, -0.03, both contracts have observed narrow ranges in a muted Asian session on Monday.

- RBA dated futures price no change in the cash rate ahead of tomorrow's monetary policy decision. A terminal rate of 4.35% is seen in June 2024.

- Looking at the data docket the aforementioned RBA decision provides the highlight. We also have Trade Balance crossing on Thursday.

NZGBs: Cheaper, RBNZ In View

NZGBs have finished dealing 5-7bps cheaper across the major benchmarks, the curve has bear steepened.

- A cheapening in US Tsys, after a deal to avert a govt shutdown pass Congress over the weekend, spilled over into the wider space.

- August Building Permits fell 6.7% M/M, the prior read was revised lower to -5.4%. A reminder that early this morning the NZIER Shadow Board recommended that the OCR be held unchanged this week, 2 of the board said that the OCR should be hiked 25 bps with 6 members voting for unchanged.

- RBNZ OIS price no change at this week's meeting, a terminal rate of 5.75% is seen in February 2024.

- The aforementioned RBNZ meeting on Wednesday headlines an otherwise thin docket this week.

GOLD: Bullion Continues To Weaken As Rate Cut Expectations Postponed

Gold prices fell 0.9% on Friday driven by a stronger greenback during the NY session. It is down another 0.3% to $1843.84/oz during the APAC session today although trading is thin with a number of holidays across the region. It is off its intraday low of $1842.94 but is still at its lowest since before US banking troubles erupted in early March. The USD index is 0.1% higher.

- The fall in bullion to below $1900/oz triggered ETF outflows, and exacerbated the sell-off, according to Bloomberg.

- S&P e-minis are up 0.6% today as risk appetite improved following the avoidance of a US government shutdown on the weekend.

- Expectations that interest rates will be higher for longer thus postponing the start of monetary easing has pushed bond yields higher across the OECD and weighed on gold prices. They are approaching support at $1839.

- Later Fed Chairman Powell and Fed’s Harker and Williams speak. US manufacturing ISM/PMIs for September and August construction spending print. European manufacturing PMIs are also released and the euro area unemployment rate. BoE’s Mann is scheduled to speak.

OIL: Thin Asian Trading, Crude Supported By Supply Fundamentals

Oil prices are up around 0.3% during APAC trading today and are off their intraday lows. WTI is trading around $91.08/bbl after falling to $90.80 earlier. Brent is $92.44 after falling to $92.17. Trading is thin with a number of markets closed. The USD index is slightly higher.

- The Adipec energy summit being held from October 2 to 5 in Abu Dhabi is expected to provide some insight into how oil producers are viewing the market currently. UAE energy minister Al Mazrouei and OPEC secretary general Al-Ghais are scheduled to speak, according to Bloomberg.

- Crude continues to be supported by tight supply, falling inventories and Russia’s ban on diesel exports. There are also signs of increasing demand and this week’s week-long holiday in China will be watched closely for traveller numbers. Prompt spreads remain in backwardation implying a tight market.

- Later Fed Chairman Powell and Fed’s Harker and Williams speak. US manufacturing ISM/PMIs for September and August construction spending print. European manufacturing PMIs are also released and the euro area unemployment rate. BoE’s Mann is scheduled to speak.

FOREX: USD, Tsy Yields Marginally Firmer As Shutdown Avoided

The USD has ticked marginally higher alongside US Tsy Yields after a US Government shutdown was avoided. .Yesterday Congress passed a stopgap funding bill Saturday evening. The Senate voted to pass the bill on a 88 to 9 margin after the House had voted 335-91. The deal funds govt to the 17 November 2023.

- AUD/USD is pressured and sits at $0.6415/20, the pair is down ~0.3%. For now short term gains are considered corrective, and the trend condition remains bearish. Support comes in at $0.6331, low from Sep 27 and bear trigger. Resistance is at $0.6487 the 50-Day EMA.

- Kiwi is little changed, NZD/USD has see-sawed around the $0.60 handle in thin trade this morning. It is likely that pre-RBNZ positioning will dominate flows this week.

- The Yen is pressured, USD/JPY is up ~0.4% and sits at ¥149.75/80. The trend outlook for USD/JPY is unchanged and remains bullish. Resistance comes in at ¥149.71, high from October 24 2022, then 150 which is round number resistance. Support is seen at ¥147.82 the 20-Day EMA.

- Cross asset wise; US Tsy Yields are ~4bps firmer across the curve. E-minis are up ~0.6%. BBDXY is ~0.1% firmer.

- Looking ahead, the docket is mostly thin in Europe today, the September ISM MFG Survey is due further out.

EQUITIES: APAC Higher But Major Markets Closed, US Futures Rally

Asian equity markets are mixed today but S&P e-minis are up 0.6% and NASDAQ +0.7% as risk appetite improved following the avoidance of a US government shutdown on the weekend. China, HK and India are all closed for holidays as is most of Australia, although the ASX is open. China is closed all week. The USD index is up slightly.

- APAC is higher overall with the MSCI APEX up 0.4%.

- Japan’s Nikkei is up 0.8% following a better than expected Tankan survey and USDJPY weakening towards 150, but is off its intraday highs. The weaker yen has supported exporters and services companies on the back of increased tourism.

- The ASX is down 0.2% in thin trading with financials, energy and health weak. The NZX is 0.6% lower.

- Korea’s KOSPI is up 0.1% while Taiwan’s TAIEX has outperformed rising 1.3%.

- ASEAN is mixed with the Jakarta comp up 0.3% but the SE Thai flat. Singapore’s Straits Times and Philippines PSEi are 0.1% higher while Malay KLCI is 0.2% lower.

ASIA: Weak New Orders Weigh On ASEAN Manufacturing

The Asian S&P Global manufacturing PMIs for September were mixed but generally deteriorated and the ASEAN aggregate fell into contractionary territory at 49.6 from 51 for the first time in over 2 years. Business confidence is also subdued. Indonesia continues to show the strongest manufacturing growth in the region. The Bank of Thailand is the last major Asian central bank to continue hiking rates but with output falling more sharply in the latest month, pressure is building for a pause.

- Indonesia’s September manufacturing PMI eased to 52.3 from 53.9, as demand and employment continued to rise. Importantly the growth in new orders picked up. There was an increase in input cost inflation due to transport and raw materials and some of this was passed on in selling prices, but both remain subdued and below average.

- Thailand’s manufacturing PMI fell further to 47.8 from 48.9, the fifth straight monthly fall, indicating the slowest output growth since May 2021. New orders fell at their fastest pace since mid-2020 with both domestic and foreign demand weak. Employment continued to decline too. Business confidence improved though to its highest in four months, according to S&P Global. Cost and selling price pressures were subdued.

- Malaysia and Vietnam saw deteriorations in their indices at 46.8 from 47.8 and 49.7 from 50.5 respectively. The Philippines bucked the trend rising to 50.6 from 49.7.

- Taiwan’s PMI showed a smaller decline in manufacturing in September rising to 46.4 from 44.3.

- See ASEAN PMI press release here.

Source: MNI - Market News/Bloomberg

JAPAN: Weak Yen Supporting Business

The Tankan report showed generally better economic conditions for Japan’s companies in Q3 and most of the data was stronger than expected as the recovery continues. The large manufactures’ index saw the second straight rise to 9 from 5 in Q2, the highest since Q2 2022, while the outlook rose to 10 from 9. Non-manufactures outperformed as they are more immune to uncertain global demand.

- Non-manufacturers’ conditions improved to 27 from 23, the strongest since 1991, while the outlook for Q4 rose 1 point to 21. Services businesses continue to benefit from pandemic-related pent up demand.

Source: MNI - Market News/Refinitiv

- The weak yen is also supporting many industries as it is encouraging both domestic and foreign tourism and boosting goods exporters. For example, auto manufacturers saw strong results. USDJPY continues to approach 150 and is up 0.2% today to 149.62.

- Small companies were not as strong but reported robust readings, although pessimists outweigh optimists in the manufacturing sector with it holding steady at -5 with the outlook deteriorating 1 point to -2. Small non-manufacturers also outperformed though rising to 12 from 11 and the outlook to 8 from 7.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/10/2023 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Manufacturing PMI |

| 02/10/2023 | 0630/0830 | ** |  | CH | Retail Sales |

| 02/10/2023 | 0700/0900 |  | EU | ECB's de Guindos speaks at Foro Empresarial El Diario Vasco | |

| 02/10/2023 | 0715/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 02/10/2023 | 0730/0930 |  | SE | Riksbank monetary policy minutes | |

| 02/10/2023 | 0745/0945 | ** |  | IT | S&P Global Manufacturing PMI (f) |

| 02/10/2023 | 0750/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 02/10/2023 | 0755/0955 | ** |  | DE | IHS Markit Manufacturing PMI (f) |

| 02/10/2023 | 0800/1000 | ** | | EU | IHS Markit Manufacturing PMI (f) |

| 02/10/2023 | 0830/0930 | ** |  | UK | S&P Global Manufacturing PMI (Final) |

| 02/10/2023 | 0900/1100 | ** | | EU | Unemployment |

| 02/10/2023 | 1345/0945 | *** |  | US | IHS Markit Manufacturing Index (final) |

| 02/10/2023 | 1400/1000 | *** | | US | ISM Manufacturing Index |

| 02/10/2023 | 1400/1000 | * | | US | Construction Spending |

| 02/10/2023 | 1500/1600 | | UK | BOE's Mann speaks at Redburn/Rothschild event | |

| 02/10/2023 | 1500/1100 | | US | Fed Chair Jerome Powell | |

| 02/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 02/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 02/10/2023 | 1700/1300 | | US | Fed Vice Chair Michael Barr | |

| 02/10/2023 | 1730/1330 | | US | New York Fed's John Williams |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.