Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

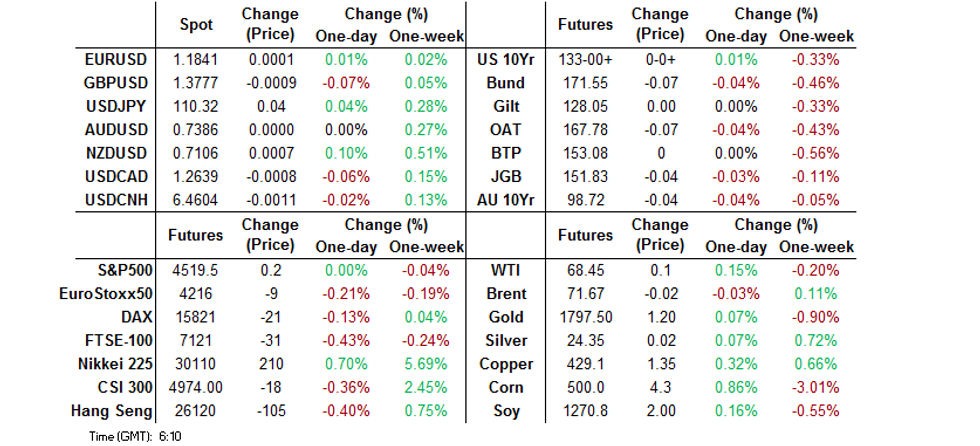

- Tight overnight trade sees U.S. Tsys little changed and most of the major global equity indices nudge slightly lower. FX trade has been muted.

- Tier 1 headline flow was light, with St. Louis Fed President Bullard ('22 voter) reiterating his stance re: the need press on with tapering, despite the recent NFP miss.

- The BoC monetary policy decision, comments from Fed's Williams & Kaplan and the latest BoE Treasury Select Committee hearing headline on Wednesday.

BOND SUMMARY: Stabilisation For Core FI In Asia

The longer end of the Tsy curve has ticked away from best levels in recent trade. It would seem that the reason behind the move may have been Abu Dhabi starting the marketing of a 2-part round of 10- & 30-Year US$ issuance, with the downtick starting before the marketing announcement hit the wider screens. T-Notes are now flat with yields virtually unchanged on the day across the cash Tsy curve at typing. Fed's Bullard ('22 voter) reiterated his view that the central bank should "press ahead with a plan to dial down its massive pandemic stimulus programme despite an abrupt slowdown in U.S. jobs growth last month," via an interview with the FT. Broader macro news flow was on the light side, while the only real market flow of note came in the form of a 4.0K screen lift in TY. The NY session will bring the JOLTS job openings print and the release of the Fed's beige book. Wednesday will also bring 10-Year Tsy supply, while Fedspeak from Williams & Kaplan rounds off the local docket.

- The JGB space looked through local data releases, with futures a touch above their overnight closing levels, last dealing -7 on the day. Yields are little changed across the JGB curve, sitting within -/+0.5bp of Tuesday's closing levels. One of the more notable candidates in the race to become leader of Japan's ruling LDP Party, Fumio Kishida, reiterated his desire to deploy a spending package worth tens of trillion yen, a need to retain bold monetary easing policies and a rethink of tax on financial income. All in all there was no fresh notable information in the address, with the central tenants of Kishida's ideals surrounding these matters already known, and no pressing need for notable tax overhauls observed e.g. consumption tax. The latest round of BoJ Rinban operations revealed the following offer/cover ratios: 1- To 3-Year: 2.30x (prev. 2.60x), 5- To 10-Year: 2.51x (prev. 2.93x).

- Aussie bond futures have stabilised in Sydney dealing, aided by the modest Asia-Pac bid in U.S. Tsys, leaving YM -1.0 and XM -3.0 at typing. The longer end of the cash ACGB curve has cheapened by ~4.0bp. There hasn't been much in the way of local news flow, with focus still on yesterday's RBA decision. The latest round of ACGB Sep '26 supply saw the weighted average yield price 0.45bp through prevailing mids at the time of supply, while the cover ratio ticked higher, moving above 6.00x, even as the auction size lifted. Another smooth takedown for ACGB supply, with well-trodden factors set to support primary demand in the coming months. Corporate and semi-issuance continued to tick over, headlined by the launch of QTC's new green Mar '32 line.

FOREX: NZD & GBP Land At Opposite Ends Of G10 Scoreboard In Quiet Asia-Pac Trade

Headlines which crossed the wires in Asia-Pac hours failed to provide market-moving signals and catalyse volatility across G10 FX space. Major currency pairs hugged tight ranges, with participants assessing the global Covid-19 outlook.

- NZD was marginally firmer as New Zealand's daily case count continued to ease. The country declared 15 new infections with the coronavirus, all of them detected in Auckland.

- GBP trailed its G10 peers ahead of a House of Commons vote on the government's new tax package, which includes 1.25pp hikes to National Insurance contributions and the dividend tax.

- Focus turns to Bank of Canada monetary policy decision and comments from Fed's Kaplan & Williams, RBA's Debelle and a slew of BoE speakers including Gov Bailey.

FOREX OPTIONS: Expiries for Sep08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1785-00(E910mln)

- USD/JPY: Y109.55($620mln), Y110.00($781mln)

- AUD/USD: $0.7070(A$1.0bln), $0.7220(A$1.0bln), $0.7425(A$673mln)

- USD/CAD: C$1.2560-75($721mln), C$1.2600($547mln), C$1.2640($750mln)

- USD/CNY: Cny6.5540($500mln)

ASIA FX: Slipped In Risk Off Environment

The won props up the performance tables in a broadly risk off session with the greenback holding its gains from Tuesday.

- CNH: Offshore yuan held a narrow range in Asia-Pac trade, hovering around neutral levels after weakening overnight. Officials said yesterday China's market liquidity will remain basically balanced and it won't have big gap or large fluctuations in the coming months

- SGD: Singapore dollar is flat, USD/SGD holding gains from the previous day, authorities remain on high alert after there were 328 locally transmitted cases in the past 24 hours.

- TWD: Taiwan dollar is weaker, USD/TWD moving away from cycle lows with continued chatter of state bank USD buying.

- KRW: Won is weaker, the worst performer in Asia. Late yesterday there were some comments from FinMin Hong, he said that it is likely there will be more BoK interest rate hikes ahead, while coronavirus cases jumped back above 2,000.

- MYR: Ringgit is weaker, PM Ismail Sabri announced that the entertainment sector will be allowed to reopen tomorrow to fully vaccinated Malaysians, with capacity limits in place. BNM will release their monetary policy decision tomorrow.

- IDR: Rupiah declined, Danareksa Consumer Confidence rebounded to 71.2 in August from 62.1 recorded in July while Bank Indonesia's consumer sentiment gauge slipped to 77.3 from 80.2

- PHP: Peso is lower, authorities have postponed easing restrictions in the National Capital Region. Metro Manila will remain under Modified Enhanced Community Quarantine (MECQ) through Sep 15.

- THB: Baht fell, A source from the ruling PPRP told the Bangkok Post that the party's SecGen Thamanat will keep his post, PM Prayuth "might not trust him as much as he used to," following accusations that Thamanat was behind a plot to oust Prayuth.

ASIA RATES: Yields Creep Higher

- INDIA: Yields higher in early trade. Yields rose and the rupee fell yesterday as dollar demand triggered outflows, the move was blamed on outflows of nearly $1 billion across corporates and exacerbated by backlogs due to the closure of US markets on Monday. Indian state governments sold INR 144.8b of bonds, less than the INR 147.3b planned. Indian assets could come under further pressure today thanks to a move higher in US yields. Participants look ahead to an INR 170bn bill sale today. Looking further ahead the RBI will conduct a bond auction tomorrow, while the highlights of the economic docket next week include industrial production, CPI and trade data.

- SOUTH KOREA: Futures in South Korea are lower, tracking a move in US tsys. In the cash space the curve twist steepened, 10-Year yield rose 0.9bps to 1.993%. Late yesterday there were some comments from FinMin Hong, he said that it is likely there will be more BoK interest rate hikes ahead, while coronavirus cases jumped back above 2,000. The BoK sold KRW 1.1tn of 1-Year MSB's, the sale was soft with cover of 1.04 and an average yield of 1.08%. Elsewhere data showed bank lending to households rose to KRW 1,046.3tn from KRW 1,040.2tn in July.

- CHINA: The PBOC matched maturities with injections today, repo rates rose with the overnight rate 18.9bps higher at 2.189% after dropping into yesterday's close while the 7-day repo rate is above the PBOC's prevailing level at 2.2016%, 5.16bps higher. Futures are slightly lower, but have come off worst levels seen slightly after the open, recovering as stocks come under pressure. As a reminder head of the PBOC's monetary policy department said yesterday China's market liquidity will remain basically balanced and it won't have big gap or large fluctuations in the coming months, while PBOC Deputy Governor Pan said China will stick to prudent monetary policy, won't impose flood-style stimulus measures and there's ample room for policy makers.

- INDONESIA: Yields higher, curve bear flattens. Danareksa Consumer Confidence rebounded to 71.2 in August from 62.1 recorded in July while Bank Indonesia's consumer sentiment gauge slipped to 77.3 from 80.2. Finance Ministry sold IDR 10t rupiah of Islamic bonds and T-bills on Tuesday, meeting its target, bid/cover came in at 5.6. Elsewhere there were reports that the government issued emergency use approval for vaccines made by CanSino Biologics and Johnson & Johnson.

EQUITIES: Japan Rally Continues

A quiet session in the Asia-Pac time zone saw most equity markets sustain minor losses, Japan was the exception where bourses rallied for an eight day. In Japan the LDP leadership race remains in the spotlight, albeit the latest headline flow surrounding the matter included little in the way of market moving updates. In China markets are slightly lower, Evergrande weighed on indices after dropping below its 2009 IPO price after its ratings were cut further. Most EM bourses are in minor negative territory after taking a negative lead from the US and as the greenback held the previous day's gains. In the US futures just about in the green after a lacklustre day on Wall Street, tech gains nudged the Nasdaq marginally higher to another record, while the benchmark S&P 500 and Dow Jones slipped.

GOLD: Looking Back Above $1,800/oz Breifly

Tuesday's uptick in the USD & U.S. real yields kept the pressure on bullion, with a sharp run lower seen on a break below the 100- & 200-DMAs and the recent intraday lows, ultimately resulting in a push below $1,800/oz. Bullion has regained some poise during Asia-Pac hours, trading a handful of dollars higher, after a brief look back above $1,800/oz overnight.

OIL: Steadies After Hitting Weekly Lows

Crude futures hovered around neutral levels in Asia after receding the previous day. WTI and Brent crude futures traded lower into the Tuesday close, pressing the oil complex to fresh weekly lows. Price action worked in favour of the WTI-Brent spread, which widened by around $0.50/bbl. USD strength was the primary catalyst behind lower commodities, exposing first support in WTI at $67.12/bbl and $70.42/bbl for Brent crude.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.