Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- China was at the fore overnight, with liquidity management via PBoC OMOs, unch. LPR fixings, state media rhetoric re: market understanding of diminished odds of a PBoC RRR cut in Q4 and a slightly higher than expected USD/CNY mid-point fixing eyed.

- The JPY found itself at the bottom of the G10 FX table, while core fixed income was subjected to another busy round of overnight dealing.

- Inflation data from the UK, Eurozone & Canada will be supplemented by another busy day on the central bank speaker front.

BOND SUMMARY: Off Worst Levels, But Core FI Biased Lower In Asia

The earlier impetus from the combination of weakness in ACGBs, U.S. fiscal matters (President Biden become more optimistic on the resolution of a spending deal within the Democratic party) and the previously outlined Chinese state media headline flow surrounding the market's understanding of diminished odds of a RRR cut from the PBoC during the remainder of '21 has subsided a little, allowing the space to find a bit of a base. E-Minis have reversed their early, modest gains, and now trade little changed. TYZ1 last trades -0-03 at 130-15, while cash Tsys run little changed to 2.0bp cheaper across the curve, with a more traditional round of bear steepening coming the fore after the early, belly-led weakness. A 2,125 lot block buy of FV futures was seen. In the short end there was a covered 40K buyer of the EDH2 99.625/99.500 put spread. A raft of Fedspeak & 20-Year Tsy supply will headline in NY hours

- JGB futures -5 at typing after extending on their overnight weakness, off of morning lows, in line with the broader theme witnessed in the core global FI space. Bears have so far failed to force a test of the month-to-date low (151.18). Cash trade saw mixed performance across the curve, with modest firming for 2s and 30+Year paper while the remainder of the major benchmarks trade 0.5-1.0bp cheaper. Local headline flow remains strangely muted, outside of an eruption of the Mt. Aso volcano. The latest round of BoJ Rinban operations drew the following offer/cover ratios: 1- to 3-Years: 3.07x (prev. 2.77x), 3- to 5-Years: 2.80x (prev. 2.74x), 5- to 10-Years: 1.86x (prev. 2.18x), 25+-Years: 5.79x (prev. 5.40x).

- Yesterday's move from the RBA re: promoting the facilitation of its yield curve targeting mechanism by upping the costs of borrowing the relevant bonds for short selling purposes supported the short end of the curve in relative terms, although pressure spilled over from a technical break lower in XM at one point, before both recovered from worst levels as core FI found a bit of a base. YM trades +2.0 on the day, with XM -7.0.

FOREX: Positive Risk Tone Dents Yen, PBOC Signals Discomfort With Yuan Strength

Risk tone in G10 FX space remained positive after strong corporate earnings reports boosted benchmark stock indices on Wall Street, while U.S. Tsy yields extended gains in early Tokyo trade. Buoyant sentiment reduced demand for safe haven currencies and conspired with Gotobi day flows against the yen, making it the worst G10 performer.

- USD/JPY rallied through Oct 4, 2018 high of Y114.55 and topped out at Y114.70, its best level since Nov 6, 2017. The cross then went offered into the Tokyo fix, trimming gains as a result. The pair's RSI moved deeper into overbought territory.

- The yuan faltered as focus turned to PBOC action and domestic data. China's central bank boosted its daily liquidity injection to net CNY90bn and set its central USD/CNY mid-point 27 pips above sell-side estimate, signalling a sense of discomfort with the redback's sharp appreciation yesterday. Meanwhile, China's new home prices registered the first monthly contraction since 2015, fuelling concerns about the systemically important local property sector.

- The Antipodeans edged away from session highs as participants assessed developments in China, yet they remained atop the G10 pile. NZD and AUD showed at their best levels against the greenback in four and three months respectively.

- Inflation reports from the EZ, UK & Canada headline today's global data docket. Central bank speaker slate is tightly packed again and features a number of Fed, ECB, Norges Bank & Riksbank members.

FOREX OPTIONS: Expiries for Oct20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1595-00(E650mln), $1.1690-95(E533mln), $1.1765-75(E1.0bln)

- GBP/USD: $1.3550(Gbp605mln), $1.3575(Gbp583mln)

- USD/JPY: Y113.50-65($741mln)

- AUD/USD: $0.7250-65(A$911mln), $0.7300(A$503mln)

- AUD/NZD: N$1.0408(A$680mln), N$1.0518(A$934mln), N$1.0568(A$1.1bln)

- USD/CNY: Cny6.4300($531mln)

ASIA FX: China Draws Attention, Redback Loses Ground

The yuan retreated as participants assessed daily PBOC operations, the central bank's yuan fixing and its decision to leave the LPR unchanged, in line with expectations. The won led gains in Asia EM space as risk-on impetus from overnight provided support.

- CNH: The PBOC fix drew attention today, in the wake of Tuesday's sharp appreciation in the yuan. China's central bank set the central USD/CNY mid-point 27 pips above sell-side estimate, signalling a sense of discomfort with a stronger redback. In addition, the PBOC boosted their daily liquidity injection to net CNY90bn, citing tax season requirements and government bond issuance. On a different front, China's new home prices registered the first monthly contraction since 2015, fuelling existing concerns about China's real-estate sector.

- KRW: The won rallied after onshore markets reopened, playing catch up with overnight risk-on flows and yuan surge. FinMin Hong said that the government discussed temporarily cutting fuel tax and could make an announcement on the matter next week, as oil prices may remain elevated for some time.

- MYR: Firmer crude likely lent some support to the ringgit, as the currency crept higher. Improving domestic Covid-19 situation may have further bolstered the MYR. There may have been an element of catch up in today's price action, as local markets were shut yesterday.

- THB: In Thailand, the Bangkok Post reported that PM Prayuth asked relevant agencies to keep diesel price at THB30/litre for as long as possible, but pushed back against haulage operators' demand to set the cap at THB25/litre. The baht struggled for any topside impetus, even as Thailand's daily Covid-19 cases fell to a fresh three-month low.

- PHP: The peso went offered amid limited local headline flow. Spot USD/PHP topped out at PHP50.925, just shy of the psychological barrier/Sep 27 high at PHP51.000/51.036.

- SGD: USD/SGD extended losses but struggled to test yesterday's low. The city state logged its record daily count of Covid-19 infections on Tuesday, but regional participants were unfazed.

- IDR: Indonesian markets were closed in observance of a local holiday.

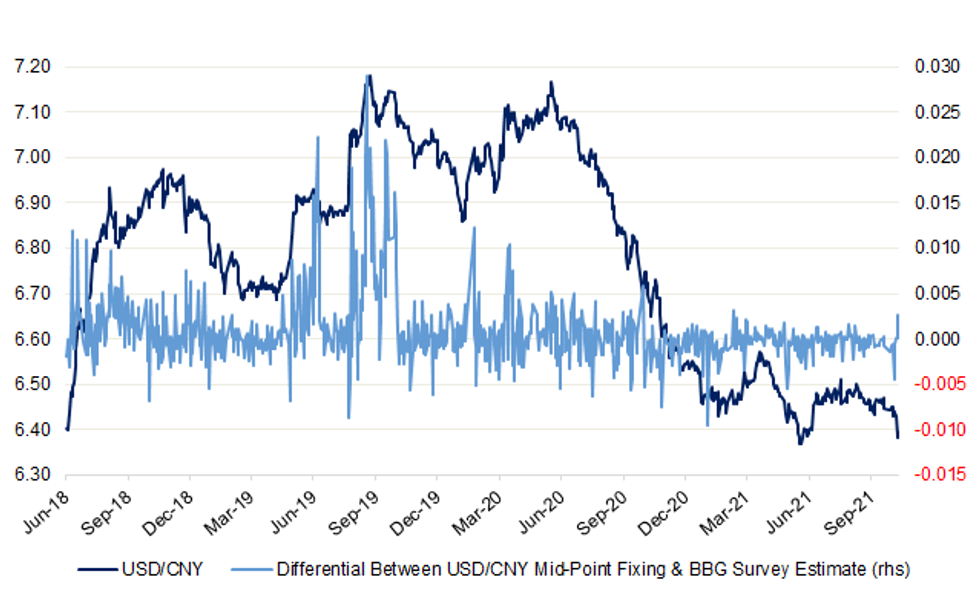

Initial Signs That The PBoC Does Not Want USD/CNY To Move Lower?

Today's USD/CNY mid-point fixing was not quite as low as the median estimate provided to BBG. Although the deviation wasn't large in historical terms, it perhaps provided an initial sign that the PBoC may not be willing to let USD/CNY trade too much lower.

Fig 1. USD/CNY Vs. Differential Between USD/CNY Mid-Point Fixing & BBG Survey Estimate

Source: MNI Market News/Bloomberg

Source: MNI Market News/Bloomberg

EQUITIES: Asia Stocks Generally Higher, Aided By U.S. Lead

The positive lead provided by Wall St. supported the majority of the major regional equity indices during Asia-Pac hours, with e-minis running little changed overnight.

- Hope re: the passing of the worst of the regulatory crackdown from Chinese policymakers allowed the Hang Seng's tech sector to rally, although the Chinese mainland indices lacked clear direction even as the PBoC stepped in with month-end/bond issuance related net OMO injections. Chinese state media also communicated the views of analysts pointing to diminished odds of a RRR cut from the PBoC in Q4, while the NBS pointed to known headwinds for the Chinese economy.

- The Hang Seng outperformed on the aforementioned strength for tech, adding over 1% on the day at typing.

GOLD: Gold Flat In Asia

Spot gold last deals little changed on the day, just above $1,770/oz. Gold pulled back from best levels during Tuesday trade, with the DXY recovering from its intraday lows alongside an uptick in our weighted U.S. real yield monitor. Still, bullion remains within the confines of the recently observed range, awaiting a catalyst for fresh impetus. Note that ETF holdings of bullion have moved to the lowest level witnessed since May '20.

OIL: Crude Lower In Asia, Headline API Crude Inventory Estimate Weighs

WTI & Brent sit ~$0.50 and ~$0.45 below their respective settlement levels, unwinding the bulk of Tuesday's gains (which were anything but one-way)

- The sharper than expected headline crude build in the weekly inventory estimates from API is applying pressure. The headline read was accompanied by a larger than expected drawdown in gasoline stocks, an in line with expected distillate drawdown and a drawdown in stocks at the Cushing hub.

- The weekly DoE inventory readings headline on Wednesday.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.