Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- ECB WEIGHS WHETHER TO PUT NUMBER ON BOND-FIGHTING SCHEME (RTRS SOURCES)

- NORTH RHINE WESTPHALIA INFLATION MODERATES

- BOJ'S KURODA VOWS TO KEEP EASY POLICY AS JAPAN LESS AFFECTED BY GLOBAL INFLATION (RTRS)

- G7 DISCUSSIONS WITH CHINA, INDIA ON RUSSIAN OIL PRICE CAP POSITIVE (RTRS SOURCE)

- BOK LIKELY TO WEIGH MORE ON 'BIG-STEP' RATE HIKE SHOULD JUNE INFLATION HIT 6 PCT (YONHAP)

- CHINA’S ECONOMY DIDN’T BOUNCE BACK IN Q2, CHINA BEIGE BOOK SURVEY FINDS (CNBC)

- COUNTY IN CHINA’S ANHUI ANNOUNCES LOCKDOWN AFTER COVID OUTBREAK (BBG)

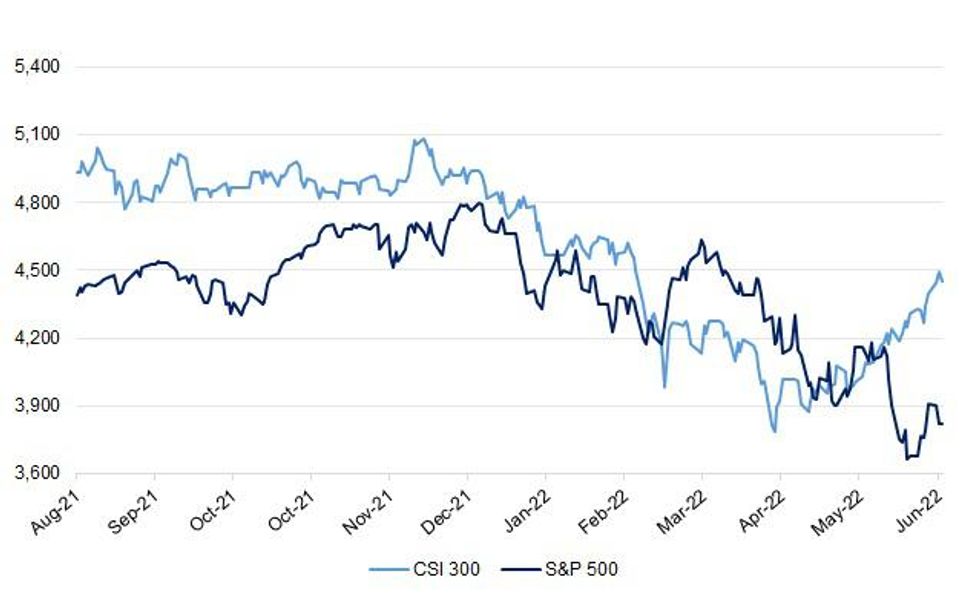

Fig. 1: CSI 300 Vs. S&P 500

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

UK

FISCAL: Rishi Sunak is resisting calls to scrap a scheduled rise in Corporation Tax in his autumn Budget despite pressure from Downing Street figures and Tory MPs. (Telegraph)

FISCAL: Boris Johnson is resisting public pressure from his own Defence Secretary and the head of the Army to increase military spending amid a Cabinet split over future funding. (Telegraph)

POLITICS: Staff at Conservative Party headquarters have war-gamed a snap election if Sir Keir Starmer is forced to quit as Labour leader, The Times has been told. Starmer is awaiting the outcome of an investigation by Durham police into whether he broke coronavirus rules when he drank beer and ate a meal in an MP’s office during the local election campaign in April last year. (The Times)

SCOTLAND: Scotland will seek the legal backing for a referendum on independence next year, escalating a standoff with the government in London that risks throwing the UK into constitutional turmoil. First Minister Nicola Sturgeon is accelerating the process of getting the necessary legislation for a vote tested in court before it heads to the Scottish Parliament. The referendum bill, which envisages a vote on Oct. 19 next year, was referred to the UK Supreme Court by Scotland’s chief legal officer, Sturgeon told lawmakers in Edinburgh on Tuesday. (BBG)

EUROPE

ECB: European Central Bank policymakers are weighing up whether or not they should announce the size and duration of their upcoming bond-buying scheme, designed to curb financing costs for Italy and other debt-laden countries, sources told Reuters. The ECB is set to announce the new tool on July 21, along with its first interest rate hike in more than a decade, in response to a surge in bond yields that has hit the most indebted countries hardest. ECB staff is preparing different options for policymakers, including how many of its details, such as firepower and duration, should be made public, according to conversations with half a dozen policymakers at the ECB's annual forum in Sintra, Portugal. (RTRS)

FRANCE: France's government cut its growth outlook sharply on Tuesday but kept its budget deficit forecast steady despite billions of extra spending on anti-inflation measures thanks to stronger than expected tax revenues. The finance ministry said that growth was now expected to be 2.5% this year, down from a previous estimate of 4% due to the impact from the Omicron COVID wave at the start of the year and Russia's invasion of Ukraine. (RTRS)

U.S.

FED: In an essay published Tuesday, St. Louis Fed President James Bullard pointed to two past examples, in 1983 and 1994, when the Fed raised rates but did not trigger a recession, and said the central bank should aim to follow that example. The Fed's "forward guidance that additional policy rate increases are likely in coming months is a deliberate step to help the FOMC more quickly move policy as necessary to bring inflation back in line with the Fed’s 2% target," Bullard wrote. (RTRS)

FED: San Francisco Federal Reserve Bank President Mary Daly on Tuesday said she believes the U.S. economy will slow to below 2% annual growth as the Fed raises interest rates, but there’s enough momentum that it won’t stop growing. “I do expect the unemployment rate to rise slightly, but nothing (like)…. what people would think of as a recession,” Daly said in an interview on LinkedIn. (RTRS)

OTHER

U.S./CHINA: The Biden administration will take a “balanced approach” on China tariffs and will issue a response soon, Deputy Commerce Secretary Don Gravessays in an interview on Bloomberg Television. “I expect that in the coming weeks we’re gonna have a very clear response,” he says. (BBG)

U.S./CHINA/TAIWAN: The G-7 should stop “interfering” in China’s internal affairs, Ma Xiaoguang, spokesman for the Taiwan Affairs Office in Beijing, said at a regular press briefing after the G-7 earlier underscored the importance of stability in the strait. The G-7 is ignoring the DPP’s provocation but wrongfully accusing China, which amounts to distortion of facts, Ma said. Separately, Ma said a bridge linking Xiamen and Kinmen would benefit people across the Taiwan Strait. (BBG)

GEOPOLITICS: Turkish President Recep Tayyip Erdoğan agreed Tuesday to lift his objection to Sweden and Finland joining NATO, paving the way for the two Nordic nations to begin the accession process. (Axios)

BOJ: The Bank of Japan will maintain its ultra-loose monetary policy as the economy has not been affected much by the global inflationary trend, Governor Haruhiko Kuroda said, stressing the country's 15-year experience with deflation is keeping wage growth subdued. "Unlike other economies, the Japanese economy has not been much affected by the global inflationary trend, so monetary policy will continue to be accommodative," he said, according to the recording released by the Bank for International Settlements (BIS). (RTRS)

RBA: With another interest rate hike from the Reserve Bank of Australia at next week’s meeting widely expected, MNI understands an increase of either 25 or 50 basis points is more likely than a larger 75 basis point hike even with inflation a growing worry. (MNI)

BOK: Demand for an unprecedented "big-step" rate hike among policymakers of the Bank of Korea (BOK) will likely intensify ahead of an upcoming rate-setting meeting should the country's consumer prices in June rise 6 percent or higher, a high-ranking central bank official has said. (Yonhap)

BRAZIL: Brazil's federal public debt rose 2.01% in May from the month before to 5.702 trillion reais ($1.08 trillion), the Treasury said on Tuesday. In April, the federal public debt had increased 0.45% over the previous month. The data had not yet been published due to a Treasury employees protest for higher salaries. (RTRS)

RUSSIA: Germany and the Netherlands will deliver six additional howitzers to Ukraine, the defence ministers of both countries said on the sidelines of a NATO summit in Madrid on Tuesday. (RTRS)

RUSSIA: Investors caught in the web of international sanctions that pushed Russia into default on bond payments are faced with the choice of seeking recompense now, or biding their time. Sanctions aimed at punishing Russia for its invasion of Ukraine shut it out of the world’s financial system, blocking its ability to transfer funds to creditors. It missed payments in late May, and a final deadline to remedy the situation expired on Sunday, creating what the bond documents call an “event of default.” Holders of at least 25% of the outstanding notes can come together to declare the debt fully and immediately repayable, “without any further formality” -- a process known as accelerating the debt -- according to the documents governing the relevant bond contracts. (BBG)

RUSSIA: Japan’s Government Pension Investment Fund reduced the value of its Russian stock and bond holdings to nearly zero at the end of fiscal 2021 compared with ~220b yen a year earlier, Nikkei reports without attribution. Doesn’t plan to make new investment into Russia assets and plans to sell off current holdings when trading activity, which has been disrupted by Western sanctions, resumes. Expected to log a gain when it reports earnings on Fri. (BBG)

METALS: Mines in Peru are operating normally amid protests, including a strike by truck drivers over fuel costs, said Raul Jacob, head of Peru’s mining society and CFO of Southern Copper. The strike hasn’t included any roadblocks, Jacob said in an emailed response to questions. (BBG)

METALS: JPMorgan Chase & Co. no longer has any exposure to the nickel bet that rocked global metals markets earlier this year, after a drop in prices on the London Metal Exchange allowed the tycoon at the center of the squeeze to exit his positions with the bank. (BBG)

OIL: OPEC+ is more than half a billion barrels behind on its pledge to supply world markets with oil, exacerbating concerns about the group’s ability to balance the global market. In May 2020, the Organization of Petroleum Exporting Countries and allies joined forces to coordinate production cuts aimed at re-balancing the global oil market. (BBG)

OIL: Group of Seven democracies have had positive and productive discussions with China and India about a plan to cap the price of Russian oil, a source familiar with the G7 discussions said on Tuesday, adding the two major oil consumers would have incentives to comply. The source, speaking on condition of anonymity, said the price-per-barrel cap level had not yet been determined, but it would have to be high enough to give Russia an incentive to keep producing oil. (RTRS)

OIL: Libya's state-owned NOC has informed some customers of force majeure restrictions at the eastern Ras Lanuf crude export terminal, according to a trade and a shipping source. One of the sources said the measure, which covers NOC for an inability to supply customers for circumstances outside its control, came into effect at the port today. An official force majeure notice has yet to be circulated to all clients, traders said. (Argus Media)

OIL: Ecuador's oil production has fallen by 1.8 million barrels during 15 days of anti-government protests and blockades, the energy ministry said on Tuesday. State-run oil company Petroecuador has borne the burnt, the ministry said in a statement, registering a reduction of 1.47 million barrels, while private producers have lost over 385,000 barrels. (RTRS)

CHINA

ECONOMY: The Chinese economy may grow around 4.8% in 2022, and could reach 5%-5.5% if supported by strong policies such as the issuance of special treasury bonds in H2, Yicai.com reported citing a report by Zhixin Investment Research Institute. If issuing CNY1.5 trillion special treasury bonds, the infrastructure investment growth in 2022 could increase by 24.8%, otherwise the figure may rise by 13.7%, the report said. The central bank is expected to cut the reserve requirement ratio in H2 to ease banks’ pressure on capital costs, the report said. (MNI)

ECONOMY: Chinese businesses ranging from services to manufacturing reported a slowdown in the second quarter from the first, reflecting the prolonged impact of Covid controls. That’s according to the U.S.-based China Beige Book, which claims to have conducted more than 4,300 interviews in China in late April and the month ended June 15. (CNBC)

CORONAVIRUS: The Sixian county in eastern Chinese province of Anhui locks down all residential communities and villages from Wednesday after Covid outbreak, according to a local government statement. Anhui province reports a total of 15 local cases for Tuesday, including 13 in Sixian. (BBG)

BANKS: Many banks in China including China Construction Bank, and China Merchants Bank see time deposit interest rates inverted and yields on large-denomination certificates of deposit continue to decline, Yicai.com reported. Banks are facing pressure on the net interest margin brought about by lower loan interest rates, coupled with sufficient liquidity and the lack of effective credit demand, their motivation to absorb deposits, especially medium- and long-term high-cost deposits, has been greatly weakened, the newspaper said citing analysts. Such pressure may ease in H2 as banks further balance the cost of its asset side and liability side, with recovering credit demand, the newspaper said citing analysts. (MNI)

CHINA MARKETS

PBOC INJECTS NET CNY90 BILLION VIA OMOS WEDNESDAY

The People's Bank of China (PBOC) injected CNY100 billion via 7-day reverse repos with the rate unchanged at 2.1% on Wednesday. This led to a net injection of CNY90 billion after offsetting the maturing CNY10 billion reverse repos today, according to Wind Information.

- The operation aims to keep liquidity stable at the end of mid-year, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.9707% at 9:33 am local time from the close of 1.9698% on Tuesday.

- The CFETS-NEX money-market sentiment index closed at 45 on Tuesday vs 49 on Monday.

PBOC SETS YUAN CENTRAL PARITY AT 6.7035 WEDS VS 6.6930

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 6.7035 on Wednesday, compared with 6.6930 set on Tuesday.

OVERNIGHT DATA

GERMANY JUN NRW CPI +7.5% Y/Y; MAY +8.1%

GERMANY JUN NRW CPI -0.1% M/M; MAY +0.9%

JAPAN MAY RETAIL SALES +3.6% Y/Y; MEDIAN +4.0%; APR +3.1%

JAPAN MAY RETAIL SALES +0.6% M/M; MEDIAN +1.0%; APR +1.0%

JAPAN MAY DEPT STORE, SUPERMARKET SALES +8.5% Y/Y; MEDIAN +4.9%; APR +4.0%

JAPAN JUN CONSUMER CONFIDENCE INDEX 32.1; MEDIAN 34.8; MAY 34.1

AUSTRALIA MAY RETAIL SALES +0.9% M/M; MEDIAN +0.4%; APR +0.9%

SOUTH KOREA JUN CONSUMER CONFIDENCE 96.4; MAY 102.6

UK JUN BRC SHOP PRICE INDEX +3.1% Y/Y; MAY +2.8%

MARKETS

SNPASHOT: NRW Inflation Off Peak

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 down 318.76 points at 26729.60

- ASX 200 down 51.34 points at 6712.30

- Shanghai Comp. down 26.16 points at 3383.05

- JGB 10-Yr future down 8 ticks at 148.42, yield down 1.1bp at 0.230%

- Aussie 10-Yr future up 1 tick at 96.205, yield down 1.2bp at 3.727%

- U.S. 10-Yr future +0-18 at 117-08+, yield down 4.69bp at 3.125%

- WTI crude down $0.53 at $111.23, Gold up $2.24 at $1822.25

- USD/JPY down 13 pips at Y136.01

- ECB WEIGHS WHETHER TO PUT NUMBER ON BOND-FIGHTING SCHEME (RTRS SOURCES)

- NORTH RHINE WESTPHALIA INFLATION MODERATES

- BOJ'S KURODA VOWS TO KEEP EASY POLICY AS JAPAN LESS AFFECTED BY GLOBAL INFLATION (RTRS)

- G7 DISCUSSIONS WITH CHINA, INDIA ON RUSSIAN OIL PRICE CAP POSITIVE (RTRS SOURCE)

- BOK LIKELY TO WEIGH MORE ON 'BIG-STEP' RATE HIKE SHOULD JUNE INFLATION HIT 6 PCT (YONHAP)

- CHINA’S ECONOMY DIDN’T BOUNCE BACK IN Q2, CHINA BEIGE BOOK SURVEY FINDS (CNBC)

- COUNTY IN CHINA’S ANHUI ANNOUNCES LOCKDOWN AFTER COVID OUTBREAK (BBG)

US TSYS: Bid Into Europe As Chinese Lockdown & German State CPI Data Support

Tsys have firmed ahead of European hours, on the back of the most populous region in Germany (NRW) experiencing a slight moderation in inflation during the month of June. Note that the state has the largest weighting in the national German CPI reading, with the remainder of the regional releases and flash national reading set to filter out through the day.

- Earlier in the session we saw a pullback in oil prices and some weight for the regional equity indices, stemming from news that a county in the Chinese province of Anhui had gone into a COVID-related lockdown, provide some light support for the space.

- TYU2 trades 0-03 off of best levels at typing, +0-18+ at 117-09, operating in a 0-17 range, on volume of ~110K.

- Wednesday’s NY session will see the final Q1 GDP print, weekly MBA mortgage apps data and Fedspeak from Powell, Mester & Bullard. The aforementioned round of German CPI readings will clearly also provide interest, given the market reaction and dynamic observed in the NRW print.

JGBS: Firmer & Flatter On Cross Market Impetus

The wider impetus surrounding core global fixed income markets in the wake of the previously outlined NRW CPI release out of Germany means that JGB futures are +3 ahead of the close of Tokyo trade, with the contract trading a little shy of best levels. The aforementioned bid in the wider core global FI space has resulted in some bull flattening of the JGB curve, with the major benchmarks running 1-3bp richer at typing. There wasn’t much in the way of idiosyncratic news flow to shape trade in the space, with the latest round of BoJ Rinban operations failing to provide anything in the way of meaningful market impact. Note that today’s rally leaves 10-Year JGB yields at 0.23%, 2bp off the upper limit of the BoJ’s permitted trading band. Tomorrow’s local docket is headlined by preliminary industrial production data and the release of the BoJ’s Rinban plan.

AUSSIE BONDS: Reversing Earlier Cheaps On German NRW CPI Beat

Aussie bonds reversed losses observed after the release of firmer than expected Australian retail sales data, with core FI markets catching a bid on the release of German NRW CPI data, pointing to easing inflation in Germany’s most populous state (details on data release fleshed out earlier).

- YM and XM are +4.5 and +1.0 respectively, operating around session highs and a little below Tuesday’s best levels, while bills run 1-2 ticks firmer through the reds. Cash ACGBs have bull steepened, running 1.0bp to 5.0bp richer across the curve, with the release of NRW CPI data unwinding the bear steepening seen just prior, with yields running flat to 5.0bp higher then.

- STIR markets are continuing to price in ~45bp of tightening for the RBA’s July meeting, little changed on the week, with a cumulative ~244bp priced in for calendar ‘22 (up from ~240bp at the beginning of the week).

- The local data docket sees May job vacancies and private sector credit due (0230 BST) on Thursday, with A$1.0bn of the 9 Sep ‘21 and A$1.5bn of the 7 Oct ‘22 Treasury Notes on tap.

EQUITIES: Lower In Asia; Chinese Real Estate Catches Bid On Vanke Comments

Asia-Pac equity indices are mostly lower at typing, with the MSCI Asia Pacific Index on track to break a four-day streak of gains. Tech equities region-wide have borne the brunt of the session’s downward pressure, tracking a similar performance from the tech-heavy NASDAQ in Tuesday’s NY session.

- The CSI300 sits 0.8% lower at typing, with losses in consumer staples dragging the index lower. Chinese property stocks bucked broader losses with the CSI300 Real Estate Index dealing 5.6% firmer at typing, catching a bid after The Paper reported comments by China Vanke Chairman Yu Liang at Vanke’s AGM on Tuesday that “in the short-term, the market has bottomed out”.

- The Hang Seng leads losses amongst regional peers, trading 1.8% lower, with >80% of the index’s constituents in the red at typing. China-based tech underperformed, seeing the Hang Seng Tech Index deal 3.0% worse off, neutralising minor gains seen in the real estate sub-index (+0.3%).

- The Nikkei 225 sits a little above session lows, dealing 1.1% weaker at typing. Utilities lead gains on gains in Tokyo Electric Power Co, with residents in Tokyo asked to restrict electricity usage for a third day amidst an ongoing heatwave. Large-cap and tech-related stocks contributed the most to losses, with a sub-gauge of information technology equities sitting 2.1% worse off at writing.

- The ASX200 sits 1.1% worse off at typing, with limited gains in energy and financials countered by broader weakness across virtually every other sector. Tech names lead losses here as well, with the S&P/ASX All Technology Index dealing 3.7% weaker at writing.

- U.S. e-mini equity index futures deal 0.2% firmer apiece, operating well within the bottom end of their respective ranges made on Tuesday at typing.

OIL: Weaker In Asia; EIA’s Delayed Inventory Release Eyed

WTI is -~$0.60 and Brent is -~$0.90, with both benchmarks operating comfortably within Tuesday’s range at typing after backing away from two-week highs made earlier in the session.

- To recap, WTI and Brent closed $2-3 higher apiece on Tuesday, with worry surrounding tightness in global crude supplies taking focus.

- To elaborate, major crude benchmarks built on an initial bid following the release of API inventory estimates late on Tuesday, with reports pointing to a larger-than-expected fall in U.S. crude inventories, paring a large build in the previous week. On the other hand, there was a reported build in gasoline and distillate stockpiles, while Cushing hub stocks declined.

- Turning to OPEC+, the group has reported a 562mn bbl shortfall re: group production targets since May ‘20, keeping in mind that collective daily output fell further to ~2.7mn bpd short of target in May.

- BBG source reports have pointed to Libya’s state oil company declaring force majeure at the port of Las Ranuf (~200K bpd loading capacity), with participants watching for further force majeure declarations at the remaining three oil ports around the Gulf of Sirte (around ~430K bpd capacity).

- Looking ahead, the EIA is due to release last week’s delayed Petroleum Status report (week ended Jun 17) later today, followed by this week’s release (week ended Jun 24) scheduled for 1530 BST.

GOLD: Little Changed In Asia

Gold sits $2/oz firmer, printing $1,822/oz at typing. The precious metal operates within a tight ~$5/oz range after briefly showing below Tuesday’s worst levels earlier in the session, with a limited downtick in the USD (DXY) providing some support for the space.

- To recap, bullion closed $2/oz lower on Tuesday amidst an uptick in U.S. real yields and the DXY. Gold has established a fairly limited $60 range in June, tracking meandering in U.S. real yields and the DXY, with focus coalescing around Fed hawkishness and expectations from some quarters re: the potential for a Fed-led economic slowdown.

- July FOMC dated OIS now price in ~66bp of rate hikes for that meeting, down from Tuesday’s intraday high (~73bp), while a cumulative ~181bp of tightening is now priced in for calendar ‘22.

- Up next, Fedspeak from Fed Chair Powell, (1400 BST), Cleveland Fed Pres Mester (1630 BST, ‘22 voter) and St. Louis Fed Pres Bullard (1805 BST, ‘22 voter) is due, with the latter noted to have written an essay on Tuesday re: the merits of keeping the Fed policy rate ahead of the inflation rate.

- From a technical perspective, gold has continued to move lower over the past two weeks, approaching initial support at $1,805.2/oz (Jun 14 low), a break of which would expose further support at $1,787.0/oz (May 16 low and bear trigger).

FOREX: EUR Drops On CPI Data From Germany’s Most Populous State

The Eurozone’s shared currency dipped upon the release of June CPI report out of North Rhine Westphalia, with headline inflation slowing to +7.5% Y/Y from +8.1% prior. Monthly inflation printed at -0.1% M/M after a 0.9% increase in May. Owing to NRW being Germany’s most populous state, its CPI is the largest contributor (21.7%) to the nationwide index, which will hit the wires later in the day.

- Reaction to NRW CPI resulted in modest recovery in gauges of greenback strength, with EUR being the largest contributor to these indices.

- Most G10 FX crosses meandered through the Asia-Pac session, as overnight headline flow failed to offer any notable catalysts.

- The Antipodeans diverged, as the Aussie landed near the bottom of the G10 pile, while the kiwi outperformed at the margin. A beat in Australian retail sales did little to rescue the Australian dollar.

- Apart from German CPI, European hours will see the release final EZ consumer confidence. After that, focus turns to the third reading of U.S. GDP & PCE.

- In addition, comments are due from Fed's Powell, Mester & Bullard, ECB's Lagarde, de Guindos & Schnabel as well as BoE's Bailey & Dhingra (many of them will speak during the ECB's Forum on Central Banking 2022).

FOREX OPTIONS: Expiries for Jun29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0550(E898mln), $1.0620-25(E1.1bln), $1.0665-75(E714mln)

- GBP/USD: $1.2750(Gbp1.5bln)

- USD/JPY: Y135.00($505mln), Y136.20($715mln), Y137.50($780mln)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/06/2022 | 0600/0800 | ** |  | SE | Economic Tendency Indicator |

| 29/06/2022 | 0600/1400 | ** |  | CN | MNI China Liquidity Suvey |

| 29/06/2022 | 0700/0900 | *** |  | ES | HICP (p) |

| 29/06/2022 | 0700/0900 | | ES | Spain Retail sales | |

| 29/06/2022 | 0745/0945 |  | EU | ECB de Guindos on Real Estate Cycles at ECB Forum | |

| 29/06/2022 | 0800/1000 | *** |  | DE | Bavaria CPI |

| 29/06/2022 | 0800/1000 | ** | | EU | M3 |

| 29/06/2022 | 0845/1045 | | EU | ECB de Guindos on Global Value Chains & Trade at ECB Forum | |

| 29/06/2022 | 0900/1100 | *** | | DE | Saxony CPI |

| 29/06/2022 | 0900/1100 | ** | | EU | Economic Sentiment Indicator |

| 29/06/2022 | 0900/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 29/06/2022 | 0900/1100 | * | | EU | Business Climate Indicator |

| 29/06/2022 | 1015/1215 | | EU | ECB Schnabel on Inflation Expectations at ECB Forum | |

| 29/06/2022 | 1030/0630 |  | US | Cleveland Fed's Loretta Mester speaking at ECB forum | |

| 29/06/2022 | 1100/0700 | ** | | US | MBA Weekly Applications Index |

| 29/06/2022 | 1200/1400 | *** | | DE | HICP (p) |

| 29/06/2022 | 1230/0830 | *** | | US | GDP (3rd) |

| 29/06/2022 | 1300/0900 | | US | Fed Chair Jerome Powell speaking at ECB forum | |

| 29/06/2022 | 1300/1500 | | EU | ECB Lagarde pm Monetary Policy Challenges | |

| 29/06/2022 | 1300/1400 |  | UK | BOE Bailey Panels ECB Forum | |

| 29/06/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 29/06/2022 | 1500/1700 | | EU | ECB Lagarde Closing Remarks at ECB Forum | |

| 29/06/2022 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 29/06/2022 | 1705/1305 | | US | St. Louis Fed's James Bullard |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.