Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FED MIGHT NOT CUT AT ALL IN ‘24- EX-FED ECONOMIST - MNI INTERVEIW

- US IN NEW STRIKES AGAINST HOUTHI TARGETS IN YEMEN - RTRS

- PAKISTAN CONDUCTS STRIKES AGAINST MILITANT GROUPS INSIDE IRAN: INTELLIGENCE OFFICIAL - AFP

- JAPAN NOV MACHINE ORDERS INCREASE CAPEX CONCERN - MNI BRIEF

- AUSSIE UNEMPLOYMENT STEADY, DESPITE 65,000 JOBS LOST - MNI BRIEF

- US AND CHINESE FINANCIAL OFFICIALS TO MEET IN BEIJING FOR TALKS - BBG

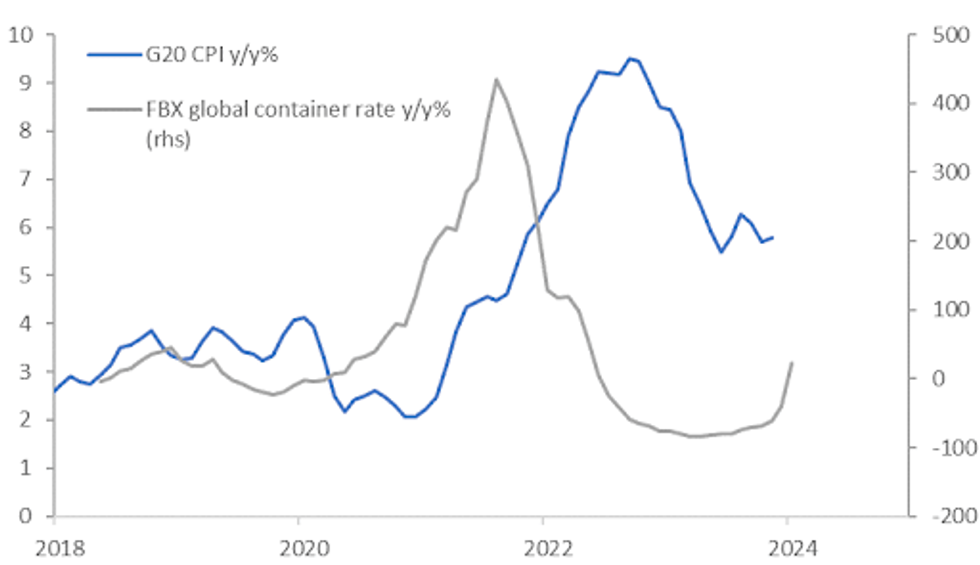

Fig. 1: G20 CPI Inflation Vs Container Rates Y/Y%

Source: MNI - Market News/Bloomberg

U.K.

POLITICS (BBG): Rishi Sunak’s signature plan to deport asylum-seekers survived a key vote in Parliament, but not before the British prime minister suffered a series of blows to his authority that damaged his hopes of avoiding defeat at a general election later this year.

HOUSING (BBG): UK estate agents are more upbeat about sales than at any time since before the pandemic amid easing mortgage costs and hopes that the Bank of England will cut interest rates, a survey found. The Royal Institution of Chartered Surveyors said its gauge of 12-month sales expectations jumped 10 percentage points in December to 34, the highest level since February 2020.

EUROPE

FISCAL (MNI INTERVIEW): The European Parliament will try to water down proposals for member states to limit fiscal deficits to 1.5% of gross domestic product over the medium term, the legislature’s representative in “trilogue” talks on the bloc’s new fiscal rules with the European Commission and the European Union’s Belgian presidency told MNI.

GERMANY (BBG): Thousands of Germans have joined nationwide protests against the far-right Alternative for Germany party (AfD) after the revelation of a meeting in which senior party members discussed a deportation scheme that echoed Nazi policies of the 1930s.

GERMANY (POLITICO): German lawmakers on Wednesday voted against a proposal from the center-right opposition Christian Democrats that included language on delivering Taurus long-range cruise missiles to Ukraine.

FRANCE (BBG): French President Emmanuel Macron backed the issuance of joint European debt to pay for priorities including defense and technology in order to ensure Europe remains sovereign amid increasing competition with China and the US.

FRANCE (POLITICO): Emmanuel Macron might be tacking right on social issues; on economics he's going back to his liberal DNA. Days after a government reshuffle, the French president announced a set of reforms to further liberalize the country's labor market and cut bureaucracy for businesses in what sounded like a resurrection of his years-old flagship measures.

RUSSIA (BBC): Russian riot police fired tear gas and hit protesters with batons in Bashkortostan on Wednesday after a rights activist was sentenced to four years in a penal colony.

CORPORATE (BBG): Bayer AG laid out plans for sweeping changes including significant job cuts in its managerial ranks, as new Chief Executive Officer Bill Anderson seeks to revive the crisis-rattled company.

U.S.

FED (MNI INTERVIEW): Stubborn price pressures could prevent the Federal Reserve from lowering interest rates this year as the economy remains strong and officials worry about easing prematurely, ex-Philadelphia Fed economist Dean Croushore told MNI.

FED (MNI BRIEF): The Fed's Beige Book Wednesday reported "little or no change in economic activity" in January's reading of anecdotal reports from business contacts, with slowing price increases and little to no net change in overall employment.

MIDEAST (RTRS): The U.S. military said on Wednesday its forces conducted strikes on 14 Houthi missiles that were loaded to be fired from Yemen, in the fourth day of U.S. strikes in less than a week. In a statement on social media platform X, U.S. Central Command said the Houthi missiles presented an imminent threat to merchant vessels and U.S. Navy ships in the region.

US/CHINA (BBG): US and Chinese officials will meet in Beijing this week for financial talks, the latest sign of the improvement in ties between the world’s two largest economies. Officials from the US Treasury will meet Chinese counterparts in Beijing Thursday and Friday, according to a Treasury official who asked not to be named. The discussions are the latest round of “financial working group” talks established last year and will include issues including financial stability, capital markets, narcotics and terrorism funding, the official said.

FISCAL (BBG): Congressional leaders said they were cautiously optimistic about reaching a deal on stricter border security that would unlock funding for Ukraine, following a White House meeting with President Joe Biden.

OTHER

PAKISTAN (AFP): The Pakistan military carried out overnight strikes in Iran, an intelligence official said Thursday, after Tehran attacked positions inside Pakistan that Islamabad said killed two children.

JAPAN (MNI BRIEF): Japan's core machinery orders, which exclude volatile items for power generation equipment and ships, fell 4.9% m/m in November for the first drop in three months, increasing concerns over the capital investment outlook, data released by the Cabinet Office showed on Wednesday.

AUSTRALIA (MNI BRIEF): Australia’s unemployment rate held steady at 3.9% in December, however, those employed dropped by 65,100 – stronger than the expected 15,000 fall. "The fall in employment in December followed larger than usual employment growth in October and November, a combined increase of 117,000 people, with the employment-to-population ratio and participation rate both at record highs in November," said David Taylor, head of labour statistics at the ABS. "While the December employment fall was large, the number of employed people was still 52,000 higher than September."

BRAZIL (MNI POLICY): Brazilian central bank officials are divided over whether there has been an increase in the country’s potential growth rate that could allow deeper cuts in the benchmark Selic rate toward the end of its monetary easing cycle, MNI understands.

CHINA

HOUSING (21st Century Business Herald): The housing market is expected to see a seasonal sales boom in Q1, though the intensity will be much weaker than the same period last year, with houses prices likely to hover at a low level, said Li Yujia, chief research fellow at the Guangdong Urban & Rural Planning and Design Institute.

FISCAL POLICY (YICAI): Policymakers should balance active fiscal policy between investment and consumption to maximise effectiveness this year, according to Luo Zhiheng, director at the China Chief Economist Forum. Luo called for wealth transfers to groups such as those below the poverty line and college students facing employment pressure.

POLICY (BBG): Chinese Premier Li Qiang gave his clearest signal yet that Beijing won’t resort to huge stimulus to revive growth amid the worst bout of deflation in decades. Another batch of troubling data is testing the patience of investors who worry Beijing is behind the curve.

CHINA MARKETS

MNI: PBOC Injects Net CNY73 Bln Via OMO Thurs; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY100 billion via 7-day reverse repo on Thursday, with the rates unchanged at 1.80%. The reverse repo operation has led to a net injection of CNY73 billion reverse repos after offsetting CNY27 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8043% at 09:56 am local time from the close of 1.9840% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 46 on Wednesday, compared with 60 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

PBOC Yuan Parity Higher At 7.1174 Thursday vs 7.1168 Wednesday

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1174 on Thursday, compared with 7.1168 set on Wednesday. The fixing was estimated at 7.1961 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND DEC REINZ HOUSE SALES Y/Y 14.1%; PRIOR 12.2%

NEW ZEALAND DEC FOOD PRICES M/M -0.1%; PRIOR -0.2%

NEW ZEALAND DEC NON-RESIDENT BOND HOLDINGS 61.3%; PRIOR 60.5%

JAPAN NOV CORE MACHINE ORDERS M/M -4.9%; MEDIAN -0.8%; PRIOR 0.7%

JAPAN NOV CORE MACHINE ORDERS Y/Y -5.0%; MEDIAN -0.1%; PRIOR -2.2%

JAPAN NOV F IP M/M -0.9%; PRIOR -0.9%

JAPAN NOV F IP Y/Y -1.4%; PRIOR -1.4%

JAPAN NOV CAPACITY UTILIZATION M/M 0.3%; PRIOR 1.5%

AUSTRALIA JAN CONSUMER INFLATION EXPECTATION 4.5%; PRIOR 4.5%

AUSTRALIA DEC EMPLOYMENT CHANGE -65.1k; MEDIAN 15k; PRIOR 72.6k

AUSTRALIA DEC FULL TIME EMPLOYMENT CHANGE -106.6k; PRIOR 57k

AUSTRALIA DEC PART TIME EMPLOYMENT CHANGE 41.4k; PRIOR 15.7k

AUSTRALIA DEC UNEMPLOYMENT RATE 3.9%; MEDIAN 3.9%; PRIOR 3.9%

AUSTRALIA DEC PARTICIPATION RATE 66.8%; MEDIAN 67.1%; PRIOR 67.3%

UK DEC RICS HOUSE PRICE BALANCE -30%; MEDIAN -36%; PRIOR -41%

CHINA DEC SWIFT GLOBAL PAYMENTS CNY 4.14%; PRIOR 4.61%

MARKETS

US TSYS: Cash Bonds Unwind Some Of Wednesday’s Bear-Flattening

TYH4 is trading at 111-16+, 0-02+ from NY closing levels.

- Cash bonds are dealing 1-3bps richer in today’s Asia-Pac session.

- There has been little meaningful newsflow in today's session, apart from the continuation of China's equity market weakness. At this stage, it is largely isolated to onshore markets with limited spillover to other regional equities, or other asset classes.

- Later today will see US Housing Starts, Building Permits, Philadelphia Fed Business Outlook and Weekly Initial Jobless Claims data.

- ECB's Lagarde speaks at the WEF panel in Davos and Fed's Bostic Speaks on the Economic Outlook.

JGBS: Bear-Steepening Strengthens In Post-20Y Auction Trading, National CPI Tomorrow

JGB futures remain in negative territory, -37 compared to the settlement levels, but slightly above the session’s worst levels.

- In addition to the morning’s Core Machinery Orders and Weekly Investment Flows data, Industrial Production (F) data for November printed in line at -0.9% m/m (-1.4% y/y). Capacity Utilization for November showed 0.3% versus 1.5% prior.

- The domestic driver for today’s session however has been the poor 20-year JGB auction. The 20-year yield is 2bps cheaper in post-auction trading after the auction low price failed to meet dealer expectations. On a positive note, the cover ratio did increase and the auction tail shortened materially. Today’s auction followed on the heels of suboptimal results at January’s 5-, 10- and 30-year JGB supply.

- The bear-steepening in the cash JGB curve has intensified in post-auction dealings, with yields flat to 9bps higher. The benchmark 10-year yield is 2.2bps higher at 0.640% versus the Nov-Dec rally low of 0.555%.

- The swaps curve has also bear-steepened, with swap spreads mixed.

- Tomorrow, the local calendar sees National CPI data and the Tertiary Industry Index.

AUSSIE BONDS: Cheaper, Post-Jobs Data Richening Largely Unwound

ACGBs (YM -7.0 & XM -5.5) sit cheaper and are situated in the middle of the Sydney session range. This follows a reversal of the post-employment data richening. Currently, futures are trading 1bp higher compared to pre-data levels.

- December new jobs came in well below expectations at -65.1k after an upwardly revised 72.6k but the unemployment rate was stable at 3.9%.

- The unwinding of post-data strength most likely reflected the understanding that a single month's data doesn't establish a definitive trend. The ABS has highlighted a shift in the timing of employment growth. Consequently, when observing trends over several months, the labour market is still characterised as tight, albeit gradually showing signs of easing.

- Apart from employment data, local participants have likely eyed the 1-3bps richening in US tsys in today’s Asia-Pac session.

- Cash ACGBs are 5-6bps cheaper on the day, with the AU-US 10-year yield differential 2bps wider at +18bps.

- Swap rates are 5bps higher on the day, with EFPs slightly tighter.

- The bills strip has maintained its bear-steepening, with pricing -1 to -8.

- RBA-dated OIS pricing is 1-5bps firmer for meetings beyond March. A cumulative 37bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty.

NZGBS: Heavy Session, US Tsys Richen In Asia-Pac Dealings

NZGBs closed at the session’s worst levels, 8-10bps cheaper, with the 2/10 curve flatter. Today’s data drop (REINZ Home Sales and Food prices) failed to provide much of a directional catalyst for the local session.

- NZGBs held by international investors jumped to 61.3% in December from 60.5% in November.

- After the negative lead-in from a heavy NY session for US tsys, the local market then moved away from morning cheaps in line with the 1-3bp richening by US tsys in today’s Asia-Pac session. However, the improvement in NZGBs proved short-lived, with cash bonds finishing at their cheaps.

- Swap rates closed 3-6bps higher, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed 1-8bps firmer across meetings, with November leading. A cumulative 91bps of easing is priced by year-end.

- Bloomberg reported that ANZ expects the RBNZ to deliver a steady sequence of 25bp rate cuts starting in August, which will take the Official Cash Rate to 3.5% over 12 months. (See link)

- Tomorrow, the local calendar sees BusinessNZ Manufacturing PMI and Net Migration data.

EQUITIES: China Indices Hit Fresh Multi Year Lows Before Stabilizing Somewhat

Regional equities are mixed in Asia Pac markets for Thursday trade. China onshore markets sit down at the break, after hitting fresh multi-year lows in earlier trade. US equity futures sit modestly lower after cash losses in Wednesday trade. Eminis were last near 4766, off a little over 0.1%, Nasdaq futures are down by a similar amount.

- China onshore equity weakness continues. The Shanghai Composite off more than 2% at one stage, but now at -1.59% at the break. This put the index at fresh lows back to early 2020 and through 2800.

- The move lower looks more flow/technically driven than any fresh fundamental catalyst. Still, there is disappointment over lack of fresh stimulus with the MLF held steady earlier in the week and recent comments by Premier Li in Davos that growth targets can be achieved without massive stimulus.

- The CSI 300 is off 0.63% at the break, also up from session lows. We are still back at 2019 levels from an index standpoint though.

- Sentiment elsewhere is more mixed. Japan stocks are modestly higher, the Nikkei 225 last +0.40%. The Taiex is up 0.40%, after officials called for calm in light of recent falls. The Kospi is also up around 0.30% at this stage.

- Indian shares have opened weaker. The Nifty off 1%, weighed by the banking sector post HDFC results.

- In SEA, trends are mixed. Malaysia and Philippines are down, but positive trends are evident elsewhere.

FOREX: Dollar Softens On Lower Yields, A$ Shrugs Off Jobs Miss

The USD has been slightly offered in the first part of Thursday trade. The BBDXY sits close to 0.10% weaker, but is up from session lows, last near 1237.40 (session lows at 1236.64).

- AUD/USD dipped close to Wednesday session lows of 0.6526, post a sharp fall in Dec jobs, which was much weaker than expected. We climbed from there though, last near 0.6560, just off session highs (0.6567).

- The ABS noted that there has been a shift in the timing of employment growth, which may have impacted today's figures, while the unemployment rate was steady at 3.9% as well. A further sharp fall in China equities hasn't impacted sentiment for the AUD.

- NZD/USD has drifted a little higher, last near 0.6120/25 within recent ranges. Food prices fell 0.1% m/m in Dec. House sales improved for Dec, but from a low base.

- USD/JPY has been supported on dips sub 148.00. Core machine orders for Nov were weaker than expected, down 4.9% m/m, placing question marks over the Capex outlook. Still, with little expected from the BoJ next week, yen has traced familiar ranges.

- Some moderation in US Tsy yields, albeit unwinding only a fraction of Wednesday's gains has likely helped at the margin. US equity futures are lower but only modestly.

- Looking ahead, focus will turn to US jobless claims and Philly fed manufacturing data. Wires will continue to be monitored for any significant headlines emanating from officials at the World Economic Forum in Davos.

OIL: Crude Higher As Red Sea Conflict Shows No Signs Of Abating

Oil is moderately higher during APAC trading today helped by another round of US strikes on Houthi positions, a lower greenback (USD index -0.1%) and more mixed risk sentiment. WTI is off its intraday low of $72.65 to be approaching $73 and is up 0.5% to $72.93/bbl. Brent is 0.2% higher at $78.08 after a low of $77.77. Prices are up moderately so far this year driven by Middle East Tensions.

- The US struck Houthi missile launchers in Yemen after another merchant vessel was hit on Wednesday. Tensions in the Red Sea are not abating and more vessels are avoiding the waterway including oil and gas carriers with shipping costs rising sharply as a result. The UK has appealed to Iran to stop arming the group.

- Iran has sent missiles into other countries this week, including Iraq and Pakistan. Pakistan is reported to have now struck Iran in retaliation, adding significantly to the potential for conflict to spread in the region.

- Bloomberg reported a US crude inventory build of 483k barrels in the latest week, according to people familiar with the API data. Gasoline rose 4.86mn and distillate +5.21mn. The official EIA data is out later today.

- Later the Fed’s Bostic speaks twice on the economic outlook at 1230 and 1705 GMT, there will be Q&A at the second appearance. He will be a FOMC member in 2024. On the data front, there are US housing starts/permits, jobless claims and Philly Fed. The ECB December meeting accounts are published and President Lagarde appears.

GOLD: Another Significant Drop As USD & Yields Move Higher

Gold is little changed in the Asia-Pac session, after closing 1.1% lower at $2006.25 on Wednesday. Bullion is close to testing the $2,000 an-ounce level, after holding above that threshold since mid-December.

- Wednesday’s move can be attributed to USD strength and higher US Treasury yields. The US Treasury curve bear-flattened, with yields 2-14bps higher, after US Retail Sales printed stronger than expected in December. The control group, which feeds into GDP, was the clear standout, jumping 0.76% m/m (cons 0.2%) after a slightly upward revised 0.47% (initial 0.40%).

- Industrial Production also fared slightly better than expected in December, rising 0.05% m/m (cons -0.1%) but the beat was offset by a downward revised 0.0% m/m (initial 0.2%) in November.

- From a technical standpoint, the precious metal pushed through supports at $2017.3/2013.4 (50-day EMA/Jan 11 low), opening a key support at $1973.2 (Dec 13 low).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/01/2024 | 0900/1000 | ** |  | EU | EZ Current Account |

| 18/01/2024 | 1000/1100 | ** | | EU | Construction Production |

| 18/01/2024 | 1230/0730 |  | US | Atlanta Fed's Raphael Bostic | |

| 18/01/2024 | 1330/0830 | *** | | US | Jobless Claims |

| 18/01/2024 | 1330/0830 | *** | | US | Housing Starts |

| 18/01/2024 | 1330/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 18/01/2024 | 1445/0945 | *** | | US | MNI Chicago Business Barometer Seasonal Adjustment |

| 18/01/2024 | 1515/1615 | | EU | ECB's Lagarde participates in Stakeholder Dialogue at WEF | |

| 18/01/2024 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 18/01/2024 | 1600/1100 | ** | | US | DOE Weekly Crude Oil Stocks |

| 18/01/2024 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 18/01/2024 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 18/01/2024 | 1705/1205 | | US | Atlanta Fed's Raphael Bostic | |

| 18/01/2024 | 1800/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

| 19/01/2024 | 2330/0830 | *** |  | JP | CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.