Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- COLLINS SAYS LESS FED EASING MAY BE WARRANTED - MNI

- MNI ECB WATCH : ON COURSE FOR JUNE CUT- STILL DATA-DEPENDENT

- IRAN AIMS TO CONTAIN FALLOUT IN ISRAEL RESPONSE, WILL NOT BE HASTY, SOURCES SAY - RTRS

- JAPAN REPEATS WARNING AGAINST EXCESSIVE WEAK YEN - RTRS

- BOK HOLDS POLICY RATE AT 3.50% - PRESS - MNI BRIEF

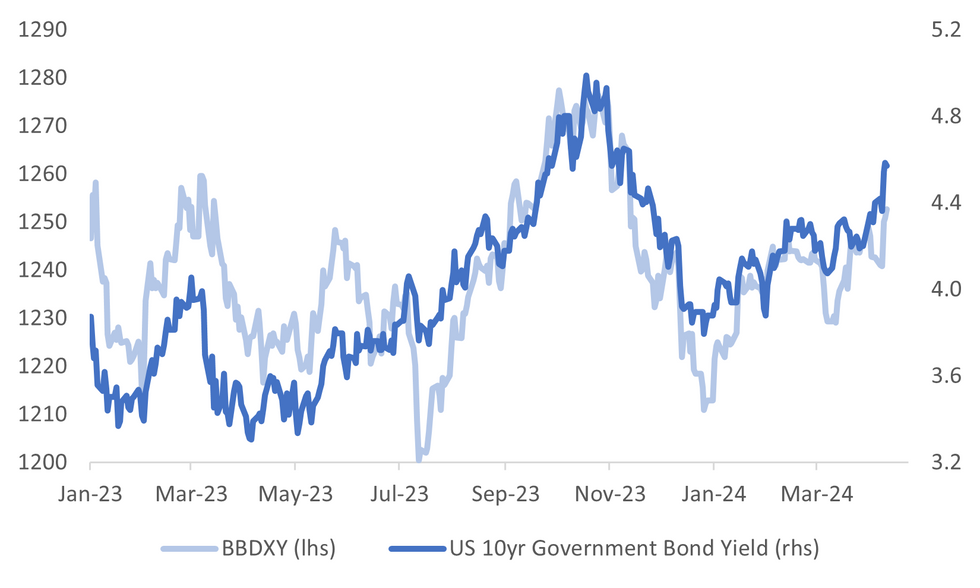

Fig. 1: USD BBDXY Index & Nominal 10yr Tsy Yield

Source: MNI - Market News/Bloomberg

EUROPE

ECB (MNI ECB WATCH): The European Central Bank pointed to a possible rate cut in June in its post-meeting statement on Thursday, but said it would keep a data-dependent approach and not commit to a pre-determined easing path.

BORROWING (MNI BRIEF): Eurogroup Chair Paschal Donohoe said Thursday he's "very confident" France and all EU member states will reduce public borrowing next year, following news France's deficit would be 5.1% of GDP this year, well above the 3% of GDP EU limit on net borrowing.

FRANCE (BBG): The French economy probably notched up slightly faster growth in the first quarter after half a year of barely expanding, according to a survey by the country’s central bank.

UKRAINE (BBG): Russia’s missile attacks on Ukraine’s energy system, the bombardment of its second-largest city and advances along the front are stoking worries that Kyiv’s military effort is nearing breaking point.

U.S.

FED (MNI): U.S. interest rates may have to stay higher for longer after recent data showing strong jobs growth and higher core inflation compared to last year, Boston Fed President Susan Collins said Thursday, adding she continues to expect to lower rates some time this year.

FED (MNI BRIEF): Richmond Fed President Tom Barkin on Thursday said the central bank should take its time to assess whether recent hot inflation is a real shift or a bump along the way, while the labor market remains strong.

CORP (BBG): Apple Inc., aiming to boost sluggish computer sales, is preparing to overhaul its entire Mac line with a new family of in-house processors designed to highlight artificial intelligence.

ISRAEL (NYT): The visit of Gen. Michael E. Kurilla, the U.S. military commander in the Middle East, came as diplomats sought to avert a wider war. The United States dispatched its top military commander for the Middle East to Israel on Thursday, after President Biden stated that, despite recent friction, American support for Israel “is ironclad” in the event of an attack by Iran.

US/CHINA (BBG): President Joe Biden has added more Chinese companies and individuals to an export blacklist than any US administration, as growing frictions between the world’s biggest economies continue to complicate global trade.

OTHER

ASIA PAC (BBG): President Joe Biden said he was committed to “deepening maritime and security ties” with Japan and the Philippines as he sought to assure allies worried about increasingly assertive Chinese actions in disputed waters.

IRAN (RTRS): Iran has signalled to Washington that it will respond to Israel's attack on its Syrian embassy in a way that aims to avoid major escalation and it will not act hastily, as Tehran presses demands including a Gaza truce, Iranian sources said.

ISRAEL (WSJ): Israel is preparing for a direct attack from Iran on southern or northern Israel as soon as the next 24 to 48 hours, according to a person familiar with the matter. A person briefed by the Iranian leadership, however, said that while plans to attack are being discussed, no final decision has been made.

JAPAN (RTRS): Japanese Finance Minister Shunichi Suzuki said authorities were analysing not just recent yen declines but factors that are driving the moves, and repeated that Tokyo stood ready to respond to any excessive currency swings.

OIL (BBG): US officials met secretly this week with members of Venezuelan President Nicolás Maduro’s administration to keep him engaged in negotiations over democratic reforms as a deadline nears to reinstate sanctions against the nation’s oil industry.

SOUTH KOREA (MNI BRIEF): The Bank of Korea on Friday decided to keep its policy interest rate unchanged at 3.50% amid persistent concern over stubborn inflation, for the 10th straight meeting, Wowkorea reported.

SOUTH KOREA (BBG): Samsung Electronics Co. is preparing to take the wraps off a $44 billion investment in US chipmaking as soon as next week, a signature project in Washington’s broader effort to bring semiconductor production back to America.

NEW ZEALAND (BBG): New Zealand consumer spending was sluggish in the first three months of the year, indicating the economy remains weak. First-quarter retail purchases on credit and debit cards rose 0.1% from the fourth quarter, when they declined 0.9%, Statistics New Zealand said Friday in Wellington.

NEW ZEALAND (BBG): New Zealand’s manufacturing industry has contracted for a 13th consecutive month, the most sustained downturn since 2009. The Performance of Manufacturing Index fell to 47.1 in March from a revised 49.1 in February, Business New Zealand and Bank of New Zealand said Friday in Wellington. The index was last above 50, indicating expansion, in February 2023.

CHINA

CPI (21st CENTURY HERALD): China’s March CPI print of 0.1% y/y, down 0.6% from February, shows consumption remains in the post-epidemic recovery stage, according to Luo Zhiheng, chief economist of Guangdong Securities. Luo noted tourism increased by 10.1% y/y but communication tools and transportation decreased by -2.1% and -5.2%, showing current consumption of mobile phones, cars and other commodities remains weak.

HAINAN (21st CENTURY HERALD): Authorities in Hainan will break the province's economic reliance on real estate and construct a modern industrial system with high productivity, Liu Xiaoming, deputy secretary of the Hainan Provincial Party Committee told reporters at a recent press conference.

CHINA MARKETS

MNI: PBOC Injects Net CNY2 Bln Via OMO Fri; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY2 billion via 7-day reverse repo on Friday, with the rates unchanged at 1.80%. The operation has led to a net injection of CNY2 billion as no reverse repo matures today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8175% at 09:48 am local time from the close of 1.8239% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Thursday, compared with the close of 45 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0967 on Friday, compared with 7.0968 set on Thursday. The fixing was estimated at 7.2331 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND MAR BUSINESSNZ MANUFACTURING PMI 47.1; PRIOR 49.1

NEW ZEALAND MAR CARD SPENDING TOTAL M/M 0.1%; PRIOR -2.0%

NEW ZEALAND MAR CARD RETAIL TOTAL M/M -0.7%; PRIOR -2.0%

NEW ZEALAND MAR FOOD PRICES M/M -0.5%; PRIOR -0.6%

JAPAN FEB F IP M/M -0.6%; PRIOR -0.1%

JAPAN FEB F IP Y/Y -3.9%; PRIOR -3.4%

JAPAN FEB CAPACITY UTILIZATION M/M -0.5%; PRIOR -7.9%

SOUTH KOREA MAR UNEMPLOYMENT RATE 2.8%; MEDIAN 2.8%; PRIOR 2.6%

MARKETS

US TSYS: Treasury Futures Little Changed, Yields 1-2bps Lower, UofM Sentiment Later

- Jun'24 futures edged slightly higher in the morning session hitting highs of 108-07+, before paring most of those gains to trade up + 01 at 108-04+. 10Y futures have touched oversold territory, with the 14-day RSI now hovering at 30, levels we have not seen since Oct 2023 when the 10y yield hit 5%, while 5Y futures are now trading below the 30 mark.

- Looking at technical levels: Initial support lays at 108-00 (round number support), below here 107-26+ 2.382 (proj of Dec 27 - Jan 19 - Feb 1 price swing), while a break here would open a move to 107-07+ (76.4% of the Oct - Dec ‘23 bull leg). While to the upside resistance holds at 109-02/26+ (Apr 8 low / Apr 10 high), a break back above here would open up 110-06 (Apr 4 high)

- Cash Treasury curve is slightly steeper today with yields 1-3bps lower, the 2Y yield is -2bps at 4.941%, 10Y -1.8bp to 4.569%, while the 2y10y is +0.104 at -37.542.

- (Bloomberg) Bonds Are Data Dependent Too as Yields March Higher (See link)

- Looking Ahead: Import Price Index, U. of Mich. Sentiment later tonight & Fed Speak

JGBS: Twist-Flattening, Light Domestic Calendar, Narrow Ranges

JGB futures are weaker, -6 compared to the settlement levels after dealing in a narrow range in today’s Tokyo session.

- Industrial Production was revised down to -0.6% in the final report. Capacity Utilisation fell 0.5% in February.

- (Bloomberg) Many Japanese companies are paying more to raise money from shorter-tenor notes as the Bank of Japan prepares to wind down corporate bond purchases as part of its historic move away from ultra-accommodative policy. (See link)

- Cash US tsys are dealing 1-2bps richer in today's Asia-Pac session after finishing Thursday with a slight twist-steepening.

- The cash JGB curve has twist-flattened, pivoting at the 5s, with yields 0.5bp higher to 4.0bps lower. The benchmark 10-year yield is 2.0bps lower at 0.851% versus the YTD high of 0.871% set yesterday.

- Swaps are richer, with rates 1-3bps lower across maturities. Swap spreads are tighter out to the 10-year and wider beyond.

- On Monday, the local calendar is light, with Core Machine Orders as the highlight.

AUSSIE BONDS: Cheaper, Narrow Ranges, Light Local Calendar, Jobs Report Next Thursday

ACGBs (YM -3.0 & XM -3.5) are holding cheaper after dealing in narrow ranges in today’s Sydney session. With the domestic data calendar light, local participants likely eyed US tsy dealings in today’s Asia-Pac session for directional guidance. Cash US tsys are 1-2bps richer, with a slight steepening bias.

- (AFR Joye) Equity and fixed-income investors were shocked during the week by the release of the official US inflation data, which confirmed a massive re-acceleration in services (rather than goods) inflation in March, with the annualised trend now running at an incredible 6.5 per cent (or 7.7 per cent if we exclude housing). (See link)

- Cash ACGBs are 3bps cheaper, with the AU-US 10-year yield differential 3bps lower at -28bps.

- Swap rates are 3.4bps higher, with the 3s/10s curve steeper.

- The bills strip has bear-steepened, with pricing -2 to -6.

- RBA-dated OIS pricing is 4-5bps firmer for 2025 meetings. A cumulative 17bps of easing is priced by year-end.

- The highlight of next week’s local calendar is the Employment Report for March on Thursday. The calendar is light until then.

- Next Wednesday, the AOFM plans to sell A$800mn of the 3.00% 21 November 2033 bond.

NZGBS: Closed At The Session’s Cheapest Levels, Q1 CPI Next Wednesday

NZGBs closed at the session’s cheapest levels, with benchmark yields 7-9bps higher. The NZGB 10-year underperformed its $-bloc counterparts, with the NZ-US and NZ-AU yield differentials 3bps wider at +27bps and +53bps respectively.

- Softer domestic data (Manufacturing PMI, Retail Card Spending and Food Prices) failed to support the market during the session.

- Cash US tsys are dealing 1-2bps richer in today's Asia-Pac session after finishing Thursday with a slight twist-steepening.

- Swap rates closed 8bps higher.

- For meetings beyond July, RBNZ dated OIS pricing is 2-8bps firmer today and 10-22bps firmer compared to levels before the RBNZ Decision on Wednesday.

- While the RBNZ maintained its tightening bias, the primary impetus behind this shift was a substantial reduction in market expectations for easing by the US Federal Reserve. This adjustment followed the release of stronger-than-expected US CPI data earlier in the week.

- Next week, the local calendar sees the Performance Services Index and Net Migration data on Monday ahead of REINZ House Sales, Non-Resident Bond Holdings and Q1 CPI data on Wednesday.

FOREX: USD Supported On Dips, Consolidating Strong Gains For The Week

The BBDXY has gravitated higher as the Friday Asia Pac session has unfolded. The Index was last near 1252.70, still sub intra-session highs from Thursday (~1253.7), but consolidating strong gains for the week (+0.80% at this stage).

- US cash Tsy yields sit 1-2bps lower across the benchmarks. News flow has been light but 10yr futures may be seeing some support around the 108 region, particularly in light of this week's sharp sell-off. US equity futures are close to flat, while regional equities are mixed.

- USD/JPY is close to flat, with lower US yields helping curb gains at the margin. The pair was last near 153.25, so still very close to recent highs (153.32). In the early part of trade we had further FX jawboning from FinMin Suzuki. The comments didn't shift yen sentiment though, with dips sub 153.00 supported.

- NZD/USD is around 0.6000, slightly outperforming most other pairs in the G10 space. We had softer PMI and card spending updates from earlier, suggesting a still challenged economic backdrop.

- AUD/USD is near 0.6530, down slightly for the session. Post US CPI lows just under 0.6500 remain intact. This week's sharp rise in US yields has offset a generally more favorable commodity price backdrop. Iron ore is back towards $109/ton.

- Looking ahead, UK growth data headlines the calendar on Friday, before UMich consumer sentiment and inflation expectations will be the US focus.

OIL: Nudging Higher, Middle East Tensions Remain In Focus

Brent crude is firmer in the first part of Friday trade, up around 0.60%, largely reversing losses from Thursday's session. We track near $90.25/bbl in recent dealings, which leaves us comfortably within recent ranges, although down on end levels from last week. The active WTI contract was last around $85.65/bbl.

- No military strikes from Iran or proxies yesterday helped take some of the risk premium out of oil. Reuters also reported that Iran will contain the fallout in its response to Israel (i.e. avoid a major escalation) and that its response will not be hasty (see this link).

- Still, other new outlets (WSJ) have stated Israel is preparing for a near term attack from Iran and/or it proxies. Market sentiment may be skewed towards not wanting to be short crude as we move towards the weekend, hence today's modest uptick.

- Elsewhere, OPEC maintained its oil demand growth forecast for 2024 and for 2025 steady, while slightly lowering the non-OPEC supply forecast for this year according to the latest OPEC Monthly Oil Market Report.

- US officials reportedly met with Venezuelan officials this week, with democratic reforms discussed ahead of deadline around US sanctions on the country's oil industry (see this BBG link). Later on, we hear from the IEA around the global oil balance backdrop.

- The technical settings for WTI remain unchanged, a bull theme remains intact.

GOLD: Yet Another All-Time High

Gold is 0.5% higher in the Asia-Pac session, after finishing 1.6% higher at $2372.52, a new closing high, on Thursday.

- Bullion showed resilience throughout the greenback rally on Wednesday while Thursday’s softer details in the US PPI report boosted the yellow metal.

- US tsys finished Thursday’s NY session with a slight twist-steepening of the curve after a volatile start following the ECB's steady rate announcement and the largely in-line US PPI data. PPI inflation missed at 0.15% m/m (0.3% est) in March, but core measures were in line.

- Initial Jobless Claims fell 11k last week to 211k, just below expectations, but with seasonal factors around the timing of Easter still likely playing a role.

- The US 2-year finished 1bp richer, with the 10-year yield 4bps cheaper at 4.59%.

- Fed Collins and Fed Williams said it may take more time to gain the confidence to begin easing policy. Williams: “There’s no clear need to adjust monetary policy in the very near term”.

- According to MNI’s technicals team, the latest climb maintains the bullish price sequence of higher highs and higher lows and note that moving average studies are in a bull-mode condition, reflecting positive market sentiment. The $2300.0 handle has been cleared. The next objective is $2376.5, a Fibonacci projection.

ASIA STOCKS: Hong Kong & China Equities Lower, HSI Below 17,000, Property Falls

Hong Kong and China equity markets are lower today with tech names leading the decline, while Asian EV makers dip after Ford’s move to slash prices on its electric pickup truck sparked a selloff in shares of US startups, Chinese property developers extend declines, led by Shimao Group and China Vanke, as prolonged weakness in home sales, cash crunch and a lack of progress in restructuring sour investors’ sentiment, while the surge in Gold recently has helped Chinese Gold producers.

- Hong Kong equities are lower today, the HSTech Index has been range bound recently trading between 3,400 and 3,600 the index is down 1.08% for the day, the Mainland Property Index is down 3.05% while the wider HSI is down 1.73% and is now on track to close the week below 17,000 which would send a negative signal across local stocks. In China, equity markets are faring slightly better with the CSI300 off 0.28%, the CSI1000 is down 0.33% and the ChiNext is down 0.67%.

- China Northbound saw 2b of inflows on Thursday, with the 5-day average at -1.27billion, while the 20-day average sits at 1.12billion yuan.

- In the property space, many Chinese cities have recently implemented targeted easing measures in their housing markets, with 15 cities removing the lower limit for mortgage rates on first-home purchases, including Guangzhou, and four cities relaxing housing provident fund policies.

- (Bloomberg) Chinese Developers Fall as Liquidity Concerns Weigh Sentiment (See link)

- China is reducing its copper smelting output due to declining margins amidst a surge in global prices, with treatment and refining charges collapsing to near zero levels. Approximately 8.5% of the country's smelters were inactive in the first quarter, up from 4.1% a year earlier, as ore supply shortages and increased domestic capacity intensify competition. The situation poses production challenges for smelters aiming to protect their margins amid insufficient ore supplies caused by output reductions at major global producers like First Quantum Minerals Ltd. and Anglo American Plc.

- Apple is gearing up to revamp its entire Mac lineup with a new family of in-house processors, the M4 chips, designed to showcase artificial intelligence capabilities. The company aims to address sluggish computer sales by integrating AI features into its products, with plans to release updated computers starting late this year. This shift to in-house chips continues Apple's long-running initiative, known as Apple Silicon, aimed at unifying hardware and software while reducing reliance on processors made by Intel. The move is likely to impact Intel, as Apple shifts away from its processors, potentially affecting the broader semiconductor industry landscape.

- Looking ahead, China Trade Balance data is expected at 5pm AEST

ASIA PAC STOCKS: Asian Equities Mixed, Japan Equities Outperform As Yen Weakens

Regional Asian equities mixed on Friday, US equities markets rallied on mixed PPI overnight, as tech outperformed after Apple announced it is preparing to overhaul its Mac line with new in-house processors highlighting AI, while earnings will kick off later today with JPM and Citigroup reporting. Japan is the top performing market in the region, Feb Industrial Production fell to -3.9% from -3.4% y/y, South Korea's unemployment rate rose in March and BOK has kept rates on hold, New Zealand saw PMI decline in March, while card spending and Food prices ticked higher in March.

- Japan equities are higher today and now heading for a weekly rebound as tech shares followed their overseas peers higher amid optimism a solid US economy will fuel a rise in profit growth for S&P 500 companies. The yen has began to slip to lows again, Investors will continue to closely watch the currency once more as Japanese authorities warned that it will consider all options to combat weakness. Most sectors are higher this morning with Banks the exception the Topix Bank Index down 0.51%, while the wider Topix Index is up 0.42% and the Tech heavy Nikkei 225 is up 0.34%

- South Korean equities are lower today, the unemployment rate rose in March to 2.8% from 2.6% in Feb, while the BOK has kept rates on hold at 3.50%. Equity flow momentum remains strong and is by far seeing the most inflow from foreign investors in the region, with 1.35b of inflows over the past 5 trading days. The Kospi is down 0.87%.

- Taiwan equities are slightly higher today, equity flow momentum is negative in the short-term with the 5-day average now -$173m, and the 20-day average now -$210m. Taiwan has a quiet week ahead in terms of economic data released with the next released not until Apr 22 when the unemployment data is released. Focus will largely be on whether the recent rally continues and if government officials continue to warn local investors about chasing stretched valuations. The Taiex is up 0.28% today and 16% for the year with the majority of those gains coming from just three stocks with TSMC contributing about 60%, Hon Hai accounting for 8% and Quanta Computers 2.5%.

- Australian equities have opened lower today, with miners and energy shares weighing on the market, while Health care and Tech trade higher. The ASX200 is trading just on the 20-day EMA which could lend some support to the market. There is little in the way of economic data until employment data on Thursday. The ASX200 is down 0.34% at 7,785.

- Elsewhere in SEA, New Zealand equities are down 0.34% after earlier saw PMI fall to 47.1 from 49.3 in Feb, while Food prices rose to -0.5% in Mar from -0.6% m/m in Feb. Singapore equities are down 0.30% after GDP missed expectations coming in at 2.7% vs 3.0% y/y, while MAS kept policy rates unchanged. Philippines equities are up 0.30%, Malaysian equities are down 0.20% while India equities are down 0.50%.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/04/2024 | 0600/0700 | ** |  | UK | UK Monthly GDP |

| 12/04/2024 | 0600/0700 | ** | | UK | Trade Balance |

| 12/04/2024 | 0600/0700 | ** | | UK | Index of Services |

| 12/04/2024 | 0600/0700 | *** | | UK | Index of Production |

| 12/04/2024 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 12/04/2024 | 0600/0800 | *** |  | DE | HICP (f) |

| 12/04/2024 | 0600/0800 | *** |  | SE | Inflation Report |

| 12/04/2024 | 0600/0700 | | UK | BOE's Greene Panellist at Delphi Economic Forum on US vs Europe Growth | |

| 12/04/2024 | 0645/0845 | *** |  | FR | HICP (f) |

| 12/04/2024 | 0700/0900 | *** |  | ES | HICP (f) |

| 12/04/2024 | 1100/1200 | | UK | BOE's Bernanke Review of Forecasting for Monetary Policymaking | |

| 12/04/2024 | 1100/1300 |  | EU | ECB's Elderson Speaks At Delphi Economic Forum | |

| 12/04/2024 | - | *** |  | CN | Trade |

| 12/04/2024 | 1200/0800 |  | US | San Francisco Fed's Mary Daly | |

| 12/04/2024 | 1230/0830 | ** | | US | Import/Export Price Index |

| 12/04/2024 | 1300/0900 | * |  | CA | CREA Existing Home Sales |

| 12/04/2024 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 12/04/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 12/04/2024 | 1700/1300 | | US | Kansas City Fed's Jeff Schmid | |

| 12/04/2024 | 1830/1430 | | US | Atlanta Fed's Raphael Bostic | |

| 12/04/2024 | 1930/1530 | | US | San Francisco Fed's Mary Daly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.