Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

We've just published our round-up of 33 sell-side analysts' previews of the March 2024 FOMC meeting - PDF here:

MNIFOMCAnalystPreview-March2024.pdf

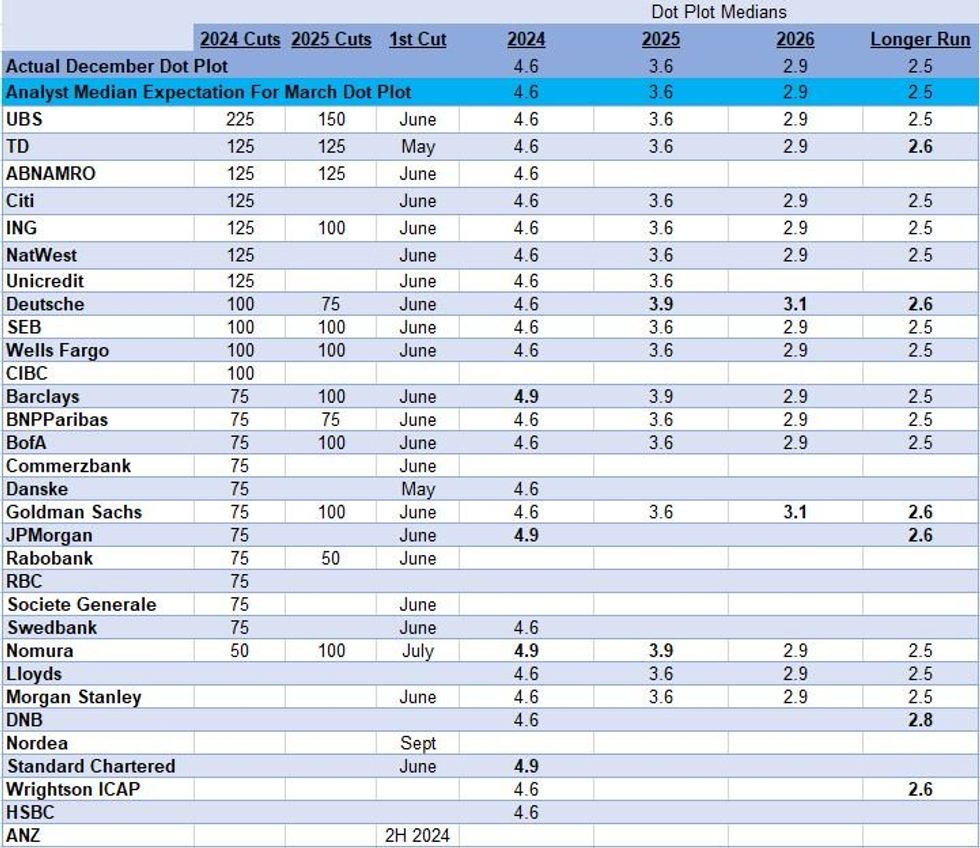

- Going into the March FOMC meeting, analyst expectations for 2024 Fed rate cuts have converged firmly on June as the starting point, but there remains a wide range of expectations otherwise.

- The “median” analyst whose previews we read for this report saw 75bp of Fed funds rate cuts in 2024 compared with 125bp pre-January meeting. There is no firm consensus though, with a wide range of expectations running from 50bp to 225bp (had been 75bp to 275bp pre-January FOMC).

- The most aggressive rate cut path we have seen is from UBS, whose analysts expect 225bp of cuts in 2024 starting in June, with 150bp more in Q1 2025.

- TD and Danske see cuts starting in May; Nomura sees July while Nordea sees September.

- For the updated Dot Plot, there is firm consensus that there will be no change to the FOMC medians for rates (20 of 24 analysts see 3 cuts, or 4.6%, remaining the base case for 2024).

- Barclays, JPMorgan, Nomura, and Standard Chartered see a rise to a 4.9% 2024 median, while Deutsche, Goldman Sachs, and Nomura see increases further out (2025-26).

- Of 18 analysts who expressed an opinion on the longer-run dot, 6 see an increase from 2.5% in the December Dot Plot.

- Several analysts expect the GDP and inflation forecasts for 2024 to be revised upward slightly. No analyst expects significant changes to the Statement.

- On tapering QT, the general expectation remains that the Fed will cap Treasury runoff at $30B (vs $60B currently) around mid-year, with an announcement in May / June.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok