Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

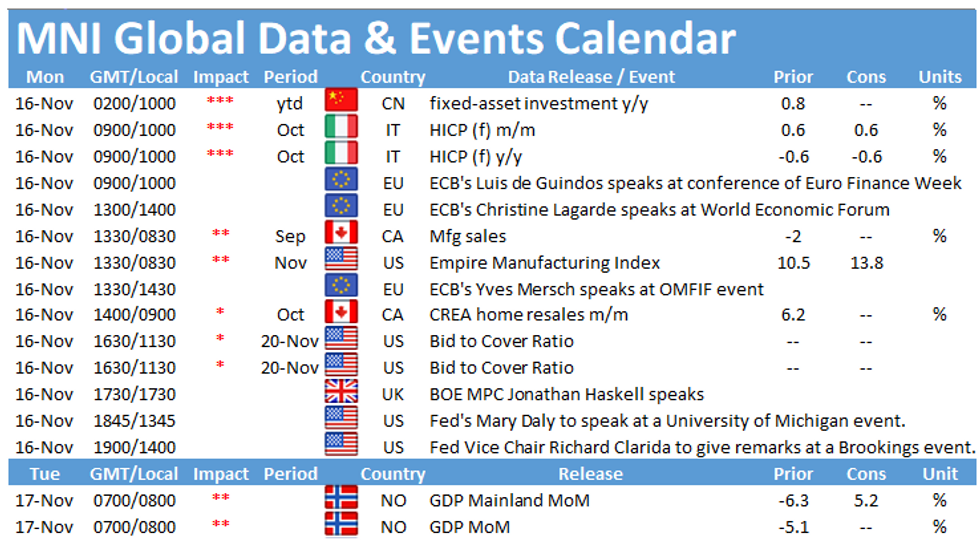

The week gets off to a quiet start in terms of data releases. The publication of the final print of Italian inflation at 0900GMT is worth noting in Europe, while in the North Americas the release of the Empire State Manufacturing survey and the Canadian survey of manufacturing, both at 1330GMT, are the highlights of the day.

Italian inflation remains negative

The annual HICP improved to -0.6% in October according to the flash estimate. The index deteriorated to -1.0% in September, down 0.5pp compared to August. Monthly inflation registered at +0.6% in October. Markets are looking for unchanged reading for the final print of inflation. The national CPI rate registered at -0.3% on an annual basis. October's uptick was driven by higher prices for unprocessed food and a smaller decline of energy prices. Istat noted that the difference between the HICP and the national rate mainly stems from end of summer sales which are not taken into account in the national rate.

Empire State manufacturing index seen rising

The headline general business index of the Empire State Manufacturing survey fell 7 points to 10.5 in October, indicating slower activity growth. The report noted that new orders and shipments increased further but unfilled orders continued to decrease. Companies remained optimistic that conditions would improve over the next six months. In November the index is forecast to rise with markets pencilling in an uptick to 13.0. The recent positive news regarding a vaccine are likely to bode well with firm's optimism regarding the outlook.

Canadian manufacturing sales eased in August

Canadian manufacturing sales dropped 2.0% in August following three consecutive months of growth. However, total sales were still 6.6% lower than in February. The biggest drops were seen in transportation equipment as well as the plastics and rubber sector. Excluding transportation equipment, sales ticked up 1.1% in August. The manufacturing PMI edged slightly lower in October but remains in expansion territory and signalled another improvement in business conditions which bodes well with manufacturing sales.

Monday's events calendar holds several interesting speakers in the cards including ECB's Luis de Guindos, Christine Lagarde and Yves Mersch as well as BOE's Jonathan Haskell and Fed's Mary Daly and Richard Clarida.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.