Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

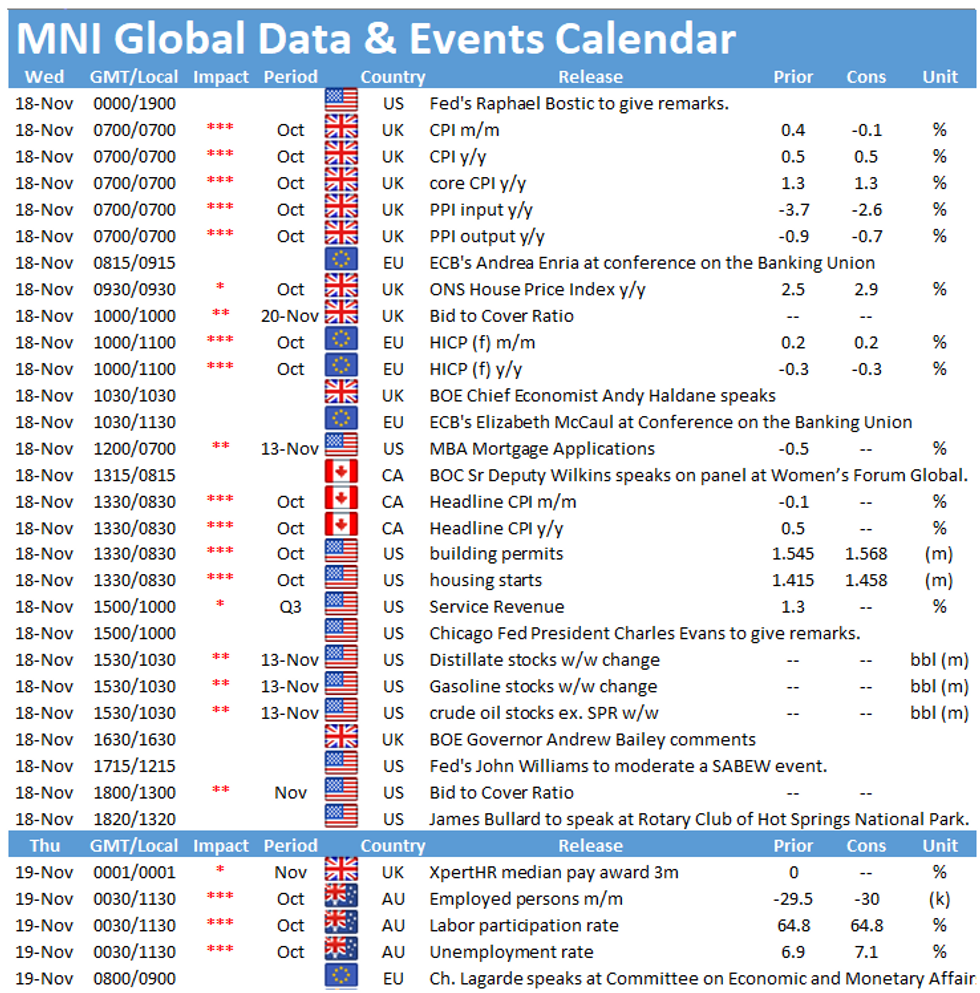

Consumer prices are the main data events to look out for Wednesday, including the publication of UK inflation figures at 0700GMT, followed by EZ inflation at 1000GMT and the Canadian consumer price index at 1330GMT.

UK inflation forecast to remain subdued

Expectations are for CPI to come in at 0.5% y/y in October, in line with the previous month, and m/m is expected to dip 0.1%. That's firmly below the Bank of England's 2% target. Core inflation is expected at 1.3% y/y, also unchanged from the previous month's reading. Input inflation is expected to improve from September's reading, with input prices seen down 2.6% y/y from -3.7%.

Survey evidence also suggests subdued prices. The BRC shop price survey noted that non-food prices showed the shallowest decline in October since the start of the pandemic. However, the BRC further stated that with stricter restrictions retailers are likely to continue discounting to attract consumers, leading lower prices. The services PMI showed the second consecutive fall in prices charged by service providers.

EZ final inflation seen at flash estimate

Final inflation in the Eurozone is expected to be in line with the flash result. Flash inflation remained negative in October at -0.3% which is the lowest level since January 2015. Energy prices continued to drag down inflation with annual energy inflation recording -8.4% in October. Core inflation remained unchanged in October at 0.2%. Inflation remains below 2% since October 2018 and is likely to remain weak over the coming months. The EZ services PMI noted another round of discounting among euro area service providers due to competitive pressures and weak demand.

Canadian inflation seen easing

The Canadian annual consumer price index ticked up to 0.5% in September, up from August's reading of 0.1%. In October markets are looking for a small dip to 0.4% for annual prices. Monthly prices are forecast to improve to 0.2% in October following an increase of 0.1% in September. September's increase was mainly driven by a smaller decline of transportation costs as prices did not follow the usual seasonal patterns.

Wednesday's event calendar holds several interesting speakers in the cards including ECB's Andrea Enria and Elizabeth McCaul as well as BOE's Andy Haldane and Andrew Bailey, Chicago Fed's Charles Evans and Fed's John Williams and James Bullard.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.