Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

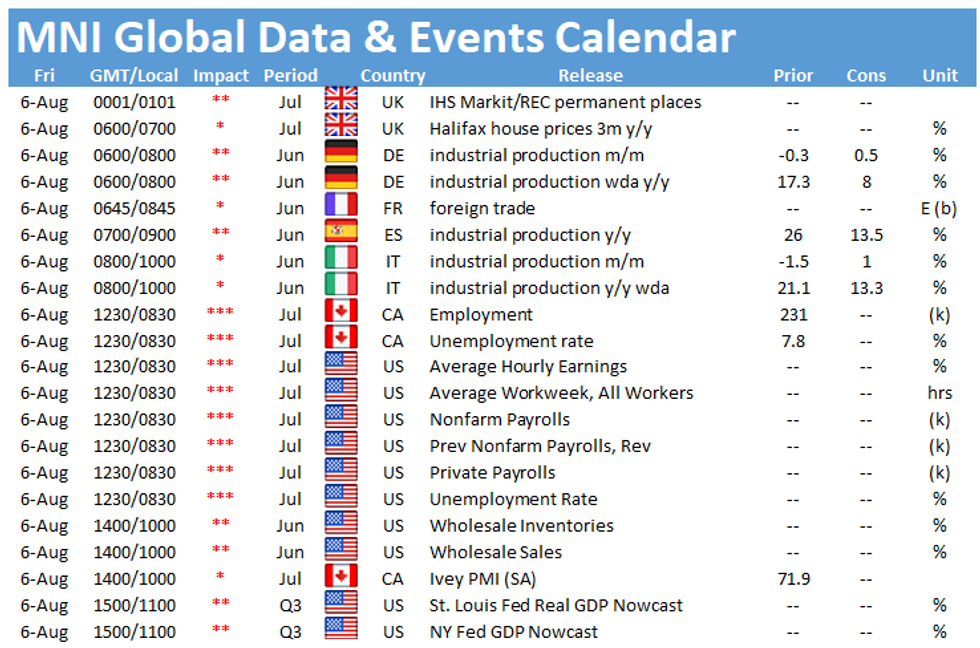

Friday once again is all about the U.S. employment data, although pan-European industrial production data early in the session will give an update as to how manufacturing is coping with global supply chain issues. The U.S. data is expected at 1330BST, with German, French and Italian data set for release through the morning.

German June IP seen recovering from May weakness.

German industrial production is expected to recover in June from the m/m decline seen in May, with analysts expecting a pick up to +0.5% from the -0.3% fall seen last month. On an annual basis, production should rise 7.9%, slowing from the base-effect boosted 17.3% gain seen in May. However, after the better than expected factory orders data released Thursday, there is an outside chance of an upward surprise.

Source: Bloomberg

U.S. Seen adding jobs again in July

U.S. job growth likely spiked again in July, with employers adding up to 870,000 jobs, according to Bloomberg estimates, after adding 850,000 in June. Higher wages and more aggressive recruiting could have sped up job growth in the service sector, analysts say, and OpenTable data through the month signaled a recovery in restaurant reservations. XXXX, as highlighted in MNI's latest Reality Check

Private payrolls should increase 808,000 after a smaller 662,000 gain in June, according to Bloomberg, although there is a downside risk following the weaker-than-expected ADP number on Wednesday. The unemployment rate is expected to sink to 5.7% from 5.9%.

US nonfarm payrolls have snapped back from April 2020 lowpoint

Source: Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.