Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (Washington)

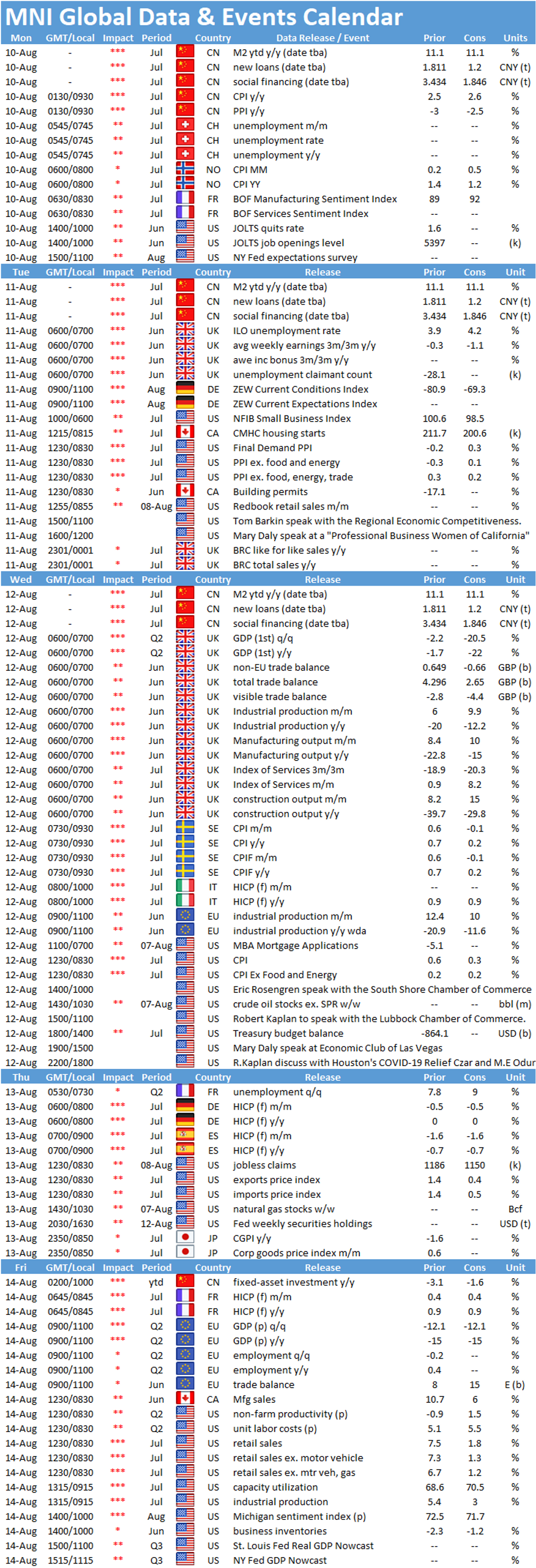

Key Things to Watch For:

- Wednesday, August 12 – UK GDP

- UK preliminary Q2 GDP data will be released Wed, offering the first official look at just how bad the damage to the economy was in the first three months of the lockdown and modest reopening of the economy.

- Monthly data for April suggested the economy fell almost 25% from its late February levels and there was only a modest bounceback recorded in the May monthly data.

- Analyst expectations suggest Q2 q/q GDP will contract around 20% -- by far the largest quarterly decline on record. GDP is seen lower by 22.5% y/y in Q2.

- One brighter spot will likely be the June monthly GDP reading, which is expected to improve around 8% m/m from May.

- Wednesday,

August 12 – U.S. CPI

- U.S. CPI should advance by 0.3% in July, mainly on strengthening gas prices and food prices as the Covid-19 pandemic continues to push consumers toward eating more meals at home.

- Excluding food and energy, CPI should increase 0.2%, bringing the y/y rate to 1.1%. Weakened demand is expected to hold down inflation in coming months.

- Friday,

August 14 – U.S. Retail Sales

- U.S. retail sales growth are set to slow in July, with markets expecting sales to add 1.8% following a 7.5% increase in June.

- Gasoline prices rose in July, but reduced travel likely put downward pressure on sales from gas stations.

- Excluding motor vehicle and gas station sales, sales should increase 1.2%. High frequency data show spending dropped off in July, suggesting consumers practiced caution through the month as the coronavirus outbreak in the U.S. worsened.

MNI Washington Bureau | +1 202-371-2121 | brooke.migdon@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok