Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- BTPs surge as former ECB President Draghi heads to the Presidential Palace

- EUR/USD circling 1.20, eyes turn to ISM, ADP data

- Heavy Fed slate, with 5 speakers scheduled

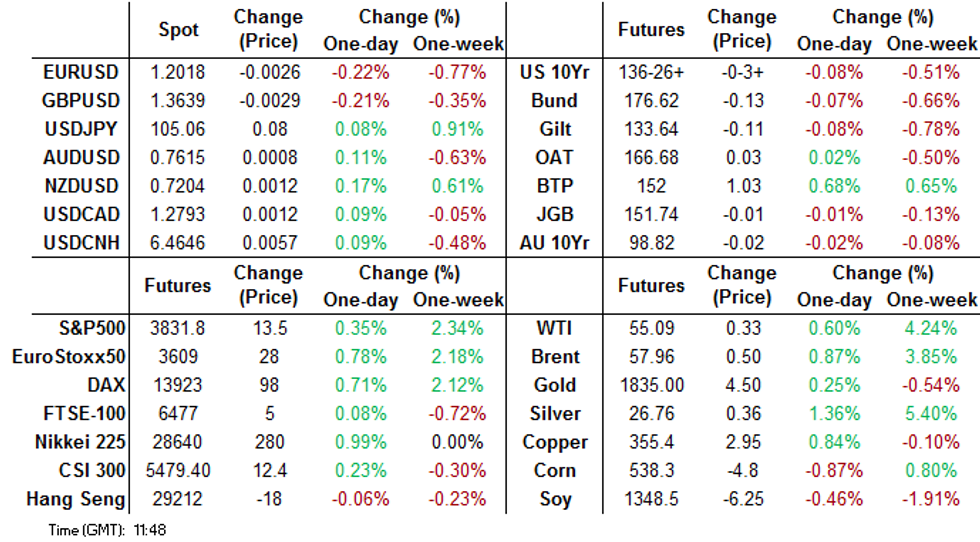

US TSYS SUMMARY: Grind Lower Ahead Of Data, Refunding

Treasuries have edged lower in overnight trade with continued bear steepening pressure in the curve. ADP and ISM Svcs data eyed along with Treasury's quarterly refunding announcement and a decent Fed speaker slate.

- Mar 10-Yr futures (TY) down 3.5/32 at 136-26.5 (L: 136-26 - the Jan 22 low / H: 137-00.5)

- The 2-Yr yield is up 0.4bps at 0.1171%, 5-Yr is up 1.1bps at 0.4511%, 10-Yr is up 2.1bps at 1.1169%, and 30-Yr is up 2.4bps at 1.8936%.

- Stock futures in the green (despite a stronger dollar on the margin), but off European morning highs.

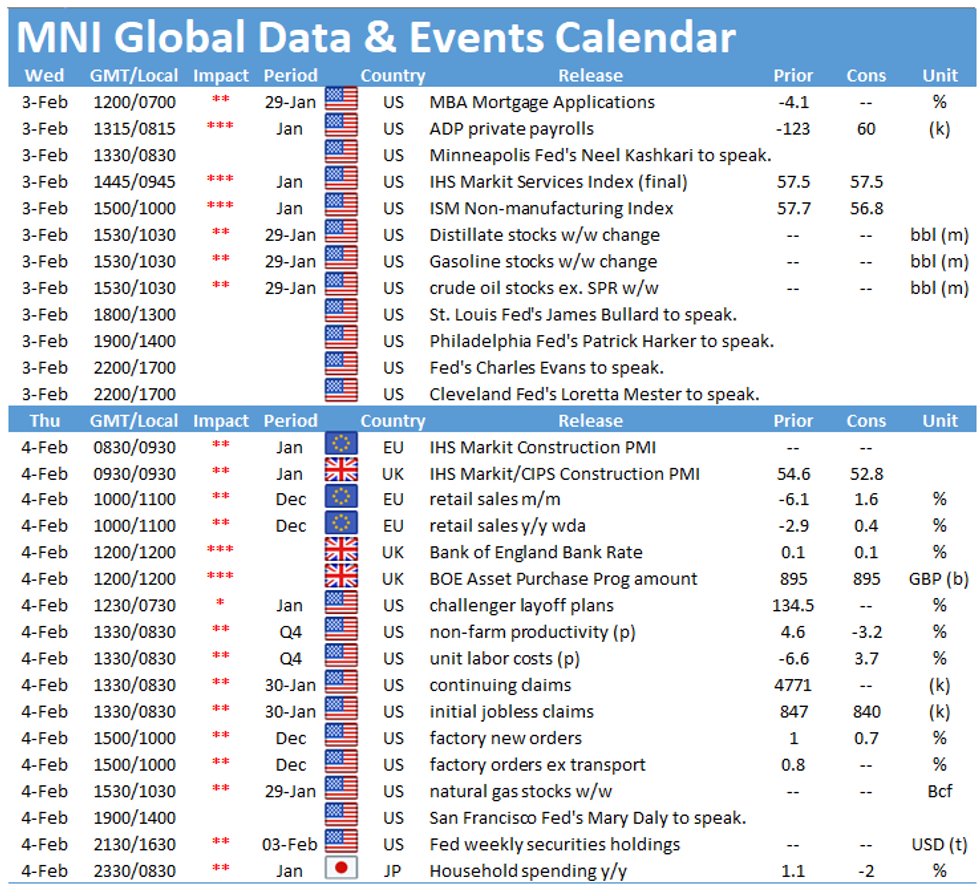

- Jan ADP Employment at 0815ET. Final Jan PMIs at 0945ET, but more attention on ISM Services shortly thereafter at 1000ET.

- Main supply event is Treasury qtly refunding estimate at 0830ET; our preview went out yesterday (link here). 1130ET sees $55B of 105-/154-day bill sale. NY Fed buys ~$6.025B of 4.5-7Y Tsys.

- Plenty of Fed Speakers: Minn's Kashkari (0830ET), StL's Bullard (1300ET), Philly's Harker (1400ET), and Cleveland's Mester and Chicago's Evans (both 1700ET).

EGBs-GILT SUMMARY: BTPs Fly On Draghi News

Italian BTPs are the star of the European FI show Weds morning, with yields and spreads collapsing as ex-ECB Draghi meets Pres Mattarella to form a technocratic gov't. Core FI a little weaker.

- In supply, PGB 30-Yr syndication for E3bn well-received (books >E40bn); UK sold GBP2.75bn of Jul-31 Gilt.

- Mixed PMIs this morning (Spain -ve, Italy +ve) and high inflation readings (EZ core +1.4% Y/Y vs 0.9% exp) provided some food for thought on the data front but apart from knee-jerk moves haven't really had a lasting impact.

- Now awaiting US Data/speakers, and further Draghi news. Our BOE meeting (Thurs) preview has just gone out (click here for link).

Latest levels:

- Mar Bund futures (RX) down 16 ticks at 176.59 (L: 176.38 / H: 176.7)

- Mar Gilt futures (G) down 12 ticks at 133.63 (L: 133.46 / H: 133.69)

- Mar BTP futures (IK) up 114 ticks at 152.11 (L: 151.58 / H: 152.29)

- Italy / German 10-Yr spread 10.7bps tighter at 103.3bps

EUROPE OPTIONS FLOW SUMMARY

Eurozone:

RXH1 178c, bought for 13.5 and 14 in 18k (short cover)

RXH1 175.50p, bought for 25-26 in 2k

DUH1 112.20p, sold at 1.25 in 4k

UK:

3LK1 99.50/99.25ps 1x1.5, bought for 2.5 in 3.5k

2LM1 99.62/99.37ps vs 2LH1 99.75/99.50ps, bought for 1 in 10k

ISSUANCE

Portugal new 30y Apr-52 OT - Launched/final terms

- Deal size set at E3bln (we had expected a E1.5-3.0bln transaction size, with risks of as large as E4.0bln).

- Books closed in excess of E40bln (including E3.25bn JLM interest)

- That is close to the record E41bln seen in July 2020 for the launch of the15-year 0.90% Oct-35 OT.

- Maturity: 12-April-2052* Spread: MS + 85 bps

- Timing: Launched. Allocs to follow.

UK:

- DMO sells GBP2.75bln nominal of 0.25% Jul-31 gilt

- Avg yld 0.441% (0.332%)

- Bid-to-cover 2.95x (2.87x)

- Tail 0.1bps (0.2bps)

- Price 98.045 (99.150)

FOREX: EUR Circling Key 1.20 Support

The single currency remains weaker, with EUR/USD inching below the Monday low to narrow the gap with key psychological support at the 1.20 handle. The moves come despite Eurozone CPI estimates for January beating to the upside, with Core CPI rising at the fastest rate in five years.

It's clear there remains caution over further EUR losses, with options markets hedging more materially against further EUR downside. Today, 1m risk reversals for EUR/USD hit their lowest level since June of last year.

EUR's losses are working in favour of the greenback, with the USD index again challenging the best levels of 2021. Scandi currencies are softening along with the EUR, with SEK, NOK among the poorest performers. AUD, NZD trade well, rising against most others so far Wednesday.

US ADP Employment Change and ISM Services are the data highlights later Wednesday, with markets watching for any further clues on this Friday's payrolls release. There are numerous Fed speakers due today, with Kashkari, Bullard, Harker, Mester and Evans all on the docket.

FX OPTIONS: Expiries for Feb03 NY cut 1000ET (Source DTCC)

EUR/USD: $1.1990-1.2000(E747mln), $1.2070-80(E1.2bln-EUR puts), $1.2100-15(E1.0bln)

USD/JPY: Y103.75-80($610mln)

EUR/GBP: Gbp0.8800-15(E488mln)

AUD/NZD: N$1.0660(A$980mln)

USD/MXN: Mxn19.50($774mln), Mxn19.70($500mln)

Tech Focus: EURUSD Approaches 1.2000

- In equities, E-mini S&P futures continue to extend this week's recovery. Attention is on this year's high of 3862.25 from Jan 26. A break would confirm a resumption of the uptrend.

- In the FX space, USDJPY is holding onto recent gains. The focus is on 105.68 next, Nov 11 high.

- EURUSD is softer following yesterday's break of support at 1.2054, Jan 18 low. The break confirms a resumption of the corrective downtrend and opens the 1.2000 handle. A break of 1.2000 would expose 1.1976, 50.0% of the Nov 4 - Jan 6 rally.

- EURGBP is pressuring 0.8800. Scope is for weakness towards 0.8759, the May 12, 2020 low.

- On the commodity front, Gold directional triggers are the resistance at $1875.2, Jan 21 high and the support at $1831.5, Jan 27 low. The yellow metal has probed $1831.5, a clear break would open $1804.7, Jan 18 low and key support. Silver remains vulnerable following yesterday's sharp sell-off. Further weakness would open $25.483, 76.4% retracement of the Jan 18 - Feb 1 rally. Oil contracts are firm. Brent (J1) has this week cleared resistance at $57.31, Jan 13 high to confirm a resumption of the broader uptrend. This opens $58.59, 76.4% of the Jan - Apr 2020 sell-off (cont). WTI (H1) has also resumed its underlying uptrend and has probed $55.00. Attention is on $56.52 next, 1.236 projection of Apr - Aug rally from the Nov 2 low

- In the FI space, Bunds (H1) Key support and the bear trigger lies at 176.34, Jan 12 low. Gilts (H1) have cleared support at 133.55, Jan 12 low. This opens 133.22 next, 1.382 projection of Dec 11 - 24 sell-off from Jan 4. BTPs (H1) gapped higher at the open. Importantly, the contract has cleared trendline resistance drawn off the Jan 8 high. The break opens 152.14, Jan 20 high.

EQUITIES: Stocks Solid, Italy Outperforms as Draghi Heads For PM

Stocks are once again solid, with continental stock markets higher by 0.3% for the FTSE-100, CAC-40 and as much as 2.5% for Italy. Reports that former ECB President Draghi is headed for the PM position in Italy has been greeted positively, with Italy's FTSE-MIB approaching the cycle highs printed in early January.

US futures trade higher once more, with the e-mini S&P higher by close to 15 points to again narrow the gap with alltime highs at 3862.25 printed on Jan26.

Earnings again remain a focus, with Amazon and Alphabet shares both higher pre-market after their respective releases yesterday. AbbVie, Biogen, Qualcomm and PayPal are among the key reports Wednesday.

COMMODITIES: Oil Remains Firm, Silver Stabilises

WTI and Brent crude futures continue to trade solidly, with both contracts higher by 0.6% or more. Contracts sit just below the week's best levels and the cycle high, but if today's gains are maintained, these key resistance levels could easily give way. First targets to the upside for WTI and Brent sit at $55.26 and $58.13 respectively.

Spot silver looks to have fully stabilised after the acute volatility earlier in the week. This keeps silver within the week's range to retain $26.287 as the first support. Spot gold trades in a similar fashion, with Tuesday's lows still first support.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.