Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Gilts outperform globally and GBP struggles vs. G10 FX peers after softer than expected CPI data allows BoE pricing to show below even odds of a rate hike re: tomorrow's meeting.

- Wider macro headline flow has been subdued ahead of the raft of impending central bank decisions.

- The FOMC decision (no move in rates expected, with focus on rhetoric & SEP) dominates the global risk docket today.

MNI Fed Preview - Sep 2023: The Last Mile

EXECUTIVE SUMMARY:

Sell-side analysts are unanimously agreed that the FOMC will leave rates on hold at the September meeting, but there are divergences in views on the Dot Plot to be submitted this week, and on the Fed’s actual rate path.

- Four analysts (of the 30 previews MNI read) see one further hike in this cycle: Barclays, BofA, Citi, Nordea.

- All analysts expect cuts in 2024, with most seeing them starting in 1Q 2024.

- The median of analysts’ expectations for the Fed’s September Dot Plot rates suggest that the central expectation is for no changes from June’s projections: 5.6% for 2023, 4.6% for 2024, 3.4% for 2025, with the new entry for 2026 at 2.6%, and the Longer-Run rate at 2.5%.

- FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK: FedPrevSep2023-ANALYSTS.pdf

MNI SNB Preview: September 2023: 25bps Hike Could Be The Last

EXECUTIVE SUMMARY:

- A 25bps rate hike to 2.00% could be the last in the cycle

- Short-term price pressures are clearly alleviating, however medium-term inflation still an issue.

- The Bank is unlikely to drop the message that more tightening may be required ahead

- Our full preview including a summary of sell-side views can be found here: MNI SNB Preview Sep 23.pdf

MNI Riksbank Preview - Sep 2023: 25bp Hike Against A Weak Backdrop

EXECUTIVE SUMMARY:

- The Riksbank are expected to hike 25bps on Thursday, with their signalling for the policy path going forwards the key question this meeting.

- Headline and underlying inflation have fallen over the summer, though the August CPIF ex-energy reading still came in above the Riksbank forecast and remains far above the 2% target.

- The continued depreciation of the SEK is of significant concern to the Executive Board. While direct intervention is not expected, there is potential for the Riksbank to announce the hedging of its FX reserves this meeting.

- The economic backdrop in Sweden has continued to show signs of weakness and we expect the Riksbank to acknowledge this fact, while keeping the door open for a November hike to keep the SEK supported.

- Our full preview including a summary of sell-side views can be found here.

MNI Norges Bank Preview: September 2023: Another 25bp Expected

EXECUTIVE SUMMARY:

- A 25bps hike could be the last of the cycle, putting peak rates at 4.25%

- Softer food prices should give board more confidence that inflation peak has passed

- While off the August highs, I-44 exchange rate is less problematic for rate path ahead

- Our full preview including a summary of sell-side views can be found here: MNI Norges Bank Preview Sep 23.pdf

US TSYS: Extending Post UK CPI Bid On FOMC Day

- Tsys have extended firmer momentum after initially limited impulse from notably softer than expected UK CPI (core 6.2% Y/Y vs cons 6.8), translating to 2Y yields back near levels prior to yesterday’s stronger CAD CPI.

- Cash Tsys trade 1-3bps richer, led by the front end to belly ahead of today’s FOMC decision.

- TYZ3 sits at session highs of 109-10, off yesterday’s late low of 109-03 which tested but didn’t breach the bear trigger at the same level from the Sep 13 low. It remains firmly in yesterday’s range albeit on relatively subdued volumes of 230k.

- Pertinent futures flow from London trade includes a 7k FV block buyer at 104-24.75 (DV01 $306k) and a 2.7k UXY block seller at 113-20+ (DV01 $245k).

- The FOMC decision is clearly in focus ahead. Our full preview can be found here: https://roar-assets-auto.rbl.ms/files/55779/FedPrevSep2023-ANALYSTS.pdf.

- Elsewhere on the docket, weekly MBA mortgage data at 0700ET plus $50B of 17-week bills at 1130ET.

- The FOMC will hold rates at its September meeting, while maintaining its tightening bias.

- Despite recent progress on inflation, which will see core PCE forecasts revised down for the first time since 2020, we expect most of the FOMC's median expectations to be largely unchanged in the latest set of quarterly projections.

- That includes the median rate "dots" indicating one further hike by end-2023, as most participants will remain cautious of signalling that the hiking cycle is over, and 100bp of cuts in 2024.

- Both of these are a very close call though, with risks that the 2023-24 dots shift a notch lower.

- The interplay between the inflation forecasts and implied 2024 cuts in the Fed funds rate projections will be a key market focus of the new projections and of the press conference.

US TSY FUTURES: Short Setting Noted On Tuesday

The combination of yesterday’s cheapening and preliminary open interest data points to short setting being the dominant theme on the Tsy futures curve on Tuesday.

- TY futures appeared to be the only contract that saw long cover in net terms.

- The net DV01 addition across the curve sat at $3.9mn.

| 19-Sep-23 | 18-Sep-23 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 3,732,346 | 3,720,145 | +12,201 | +465,848 |

| FV | 5,510,842 | 5,494,278 | +16,564 | +702,283 |

| TY | 4,697,552 | 4,701,787 | -4,235 | -275,459 |

| UXY | 1,825,833 | 1,817,248 | +8,585 | +785,656 |

| US | 1,363,172 | 1,357,789 | +5,383 | +720,005 |

| WN | 1,541,196 | 1,533,780 | +7,416 | +1,519,387 |

| Total | +45,914 | +3,917,720 |

STIR: Fed Path Unwinds Latest Disinversion Push Ahead Of FOMC Decision

- Fed Funds implied rates have pulled back some of yesterday’s latest disinversion shift with spillover from softer than expected UK CPI. It still keep end-2024 rates near recent highs and consistent with the June dot plot ahead of today’s fresh forecasts.

- Cumulative hikes from 5.33% effective: 0bp for today's decision, +7.5bp for Nov, +10.5bp for Dec and +11bp for Jan to terminal 5.44% (having first shifted into January yesterday).

- Cuts from terminal: 26bp to Jun’24 (from 25bp) and 84bp to Dec’24 (from 81bp).

STIR: OI Points To Mix Of SOFR Positioning Swings On Tuesday

The combination of yesterday’s twist steepening of the SOFR strip and preliminary OI data points to the following:

- Short cover in SFRU3, long cover in SFRZ3 & SFRH4.

- A mix of short setting and long cover in the reds, with the long cover being the dominant force on a pack basis.

- Long cover in the greens.

- Short setting providing the dominant force in the blues.

| 19-Sep-23 | 18-Sep-23 | Daily OI Change | Daily OI Change In Packs | ||

| SFRM3 | 1,103,941 | 1,105,994 | -2,053 | Whites | -55,068 |

| SFRU3 | 1,070,783 | 1,079,924 | -9,141 | Reds | -25,479 |

| SFRZ3 | 1,307,301 | 1,340,179 | -32,878 | Greens | -4,245 |

| SFRH4 | 958,988 | 969,984 | -10,996 | Blues | +10,748 |

| SFRM4 | 907,306 | 928,707 | -21,401 | ||

| SFRU4 | 787,404 | 799,265 | -11,861 | ||

| SFRZ4 | 898,693 | 890,572 | +8,121 | ||

| SFRH5 | 529,954 | 530,292 | -338 | ||

| SFRM5 | 595,724 | 596,690 | -966 | ||

| SFRU5 | 480,806 | 481,023 | -217 | ||

| SFRZ5 | 443,055 | 444,256 | -1,201 | ||

| SFRH6 | 312,270 | 314,131 | -1,861 | ||

| SFRM6 | 245,417 | 250,949 | -5,532 | ||

| SFRU6 | 201,010 | 189,800 | +11,210 | ||

| SFRZ6 | 190,706 | 187,463 | +3,243 | ||

| SFRH7 | 129,462 | 127,635 | +1,827 |

BONDS: European Issuance Update

Greece auction result:

- E200mln of the 4.25% Jun-33 GGB. Avg yield 3.3% (bid-to-cover 5.08x).

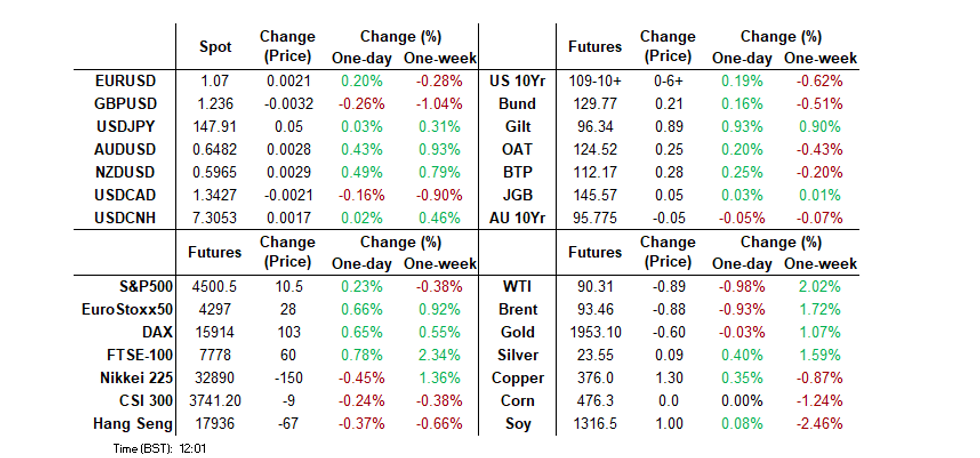

FOREX: GBP Struggles Post-UK CPI, USD/JPY Tags Fresh ’23 High

GBP finds itself at the foot of the G10 FX table after the softer than expected UK CPI data pushed markets to price less than even odds re: a BoE hike tomorrow.

- Terminal policy rate pricing has been trimmed to reflect less than 25bp of tightening i.e. one further hike is not quite fully priced.

- Meanwhile, most of the sell-side still leans towards a hike at tomorrow’s event, albeit with heavy caveats applied. Goldman Sachs were the exception, now looking for no move from the Bank.

- GBP has recovered from session lows.

- USD/JPY showed to a fresh YtD peak above Y148.00 in early London hours, dealing as high as Y148.17, before fading back below the figure.

- A quick reminder that top Japanese FX diplomat Kanda warned that the relevant Japanese authorities are watching FX markets with urgency, stressing that they will take appropriate steps if required.

- Pre-Kanda, we saw U.S. Tsy Secretary Yellen note that she understands the potential need to smooth out JPY volatility, in what was deemed a tacit approval of any required intervention on the part of the Japanese authorities.

- Higher beta FX (Scandis and Antipodeans) sit at the top of the G10 FX table, albeit within contained ranges, with global equity benchmarks on the front foot.

- The FOMC decision (no move in rates expected, with focus on rhetoric & SEP) dominates the global risk docket today.

EQUITIES: S&P E-Minis Bear Cycle Remains In Play

- A bear cycle in the E-mini S&P contract remains in play and yesterday’s break lower reinforces current conditions. The contract has breached 4483.25, the Sep 7 low. This confirms a resumption of the bear leg that started Sep 1. A continuation lower would expose 4397.75, the Aug 18 low. Initial key resistance has been defined at 4566.00, the Sep 15 high.

- A strong sell-off in EUROSTOXX 50 futures Monday highlighted a bearish start to this week’s session. A continuation lower would threaten the recent short-term bullish theme and refocus attention on key near-term support at 4210.00, the Sep 8 low. Clearance of this level would confirm a resumption of the downtrend that started late July. Key short-term resistance has been defined at 4359.00, the Sep 15 high.

COMMODITIES: Oil Futures Are Trading Lower

- Gold has recovered from last week’s $1901.1 low on Sep 14. A break of this level would strengthen a bearish theme and highlight the fact that the recovery between Aug 21 - Sep 1 has been a correction. This would expose $1884.9, the Aug 21 low. On the upside, the recent breach of the 50-day EMA does highlight a possible developing bullish threat. Key resistance is at $1953.0, the Sep 1 high where a break is required to confirm a bullish theme.

- In the oil space, the uptrend in WTI futures remains intact, however, the contract has entered a short-term bearish corrective cycle. The trend condition is overbought and a move lower would allow this to unwind. The first key support to watch lies at $86.53, the 20-day EMA and is a potential short-term objective. On the upside, clearance of yesterday’s $93.74 high would confirm a resumption of the uptrend and open $94.66,the 2.236 projection of the Jun 28 - Jul 13 - Jul 17 price swing.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/09/2023 | 0900/1100 |  | EU | ECB's Schnabel Speaks at Event | |

| 20/09/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 20/09/2023 | 1230/1430 | | EU | ECB's Elderson Speaks at Springtji Forum | |

| 20/09/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 20/09/2023 | 1730/1330 |  | CA | BOC minutes from last rate meeting | |

| 20/09/2023 | 1800/1400 | *** | | US | FOMC Statement |

| 21/09/2023 | 2245/0045 | | EU | ECB's Lane Speaks at NYU | |

| 21/09/2023 | 0600/0700 | *** |  | UK | Public Sector Finances |

| 21/09/2023 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 21/09/2023 | 0645/0845 | * | | FR | Retail Sales |

| 21/09/2023 | 0730/0930 | *** |  | CH | SNB PolicyRate |

| 21/09/2023 | 0730/0930 | ** |  | SE | Riksbank Interest Rate |

| 21/09/2023 | 0800/1000 | *** |  | NO | Norges Bank Rate Decision |

| 21/09/2023 | 1100/1200 | *** | | UK | Bank Of England Interest Rate |

| 21/09/2023 | 1100/0700 | * |  | TR | Turkey Benchmark Rate |

| 21/09/2023 | 1100/1200 | *** | | UK | Bank Of England Interest Rate |

| 21/09/2023 | 1230/0830 | *** | | US | Jobless Claims |

| 21/09/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 21/09/2023 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 21/09/2023 | 1230/0830 | * | | US | Current Account Balance |

| 21/09/2023 | 1400/1000 | *** | | US | NAR existing home sales |

| 21/09/2023 | 1400/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 21/09/2023 | 1400/1600 | | EU | ECB's Lagarde Lectures in Marseille | |

| 21/09/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 21/09/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 21/09/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 21/09/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

| 22/09/2023 | 2300/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.