Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

- USD Index remains in medium-term uptrend

- GBP underperforms as market pulls BoE-implied pricing lower

- Weekly jobless claims, slew of Fed speakers take focus ahead

US TSYS: Light Bull Steepening Ahead Of NY Trade

Tsys have ticked away from session cheaps alongside EGBs, leaving the major benchmarks flat to 3bp richer as the curve bull steepens a little (after yesterday’s post-services ISM flattening).

- TYZ3 last prints +0-06+, ticking away from yesterday’s base.

- A downtick for crude oil futures and pre-market moves lower for tech giant Apple will have aided the light bid in Tsys.

- News of a benchmark $ mandate from Slovenia has done little for the space in recent trade.

- FOMC-dated OIS still shows a terminal policy rate of ~5.45%. A little over 36bp of cuts is then priced through June ’24, as that contract consolidates a little below yesterday’s high.

- Easing priced into the strip remains comfortably shy of recent extremes after the Nov ‘23/Jun ’24 spread printed below -80bp in July.

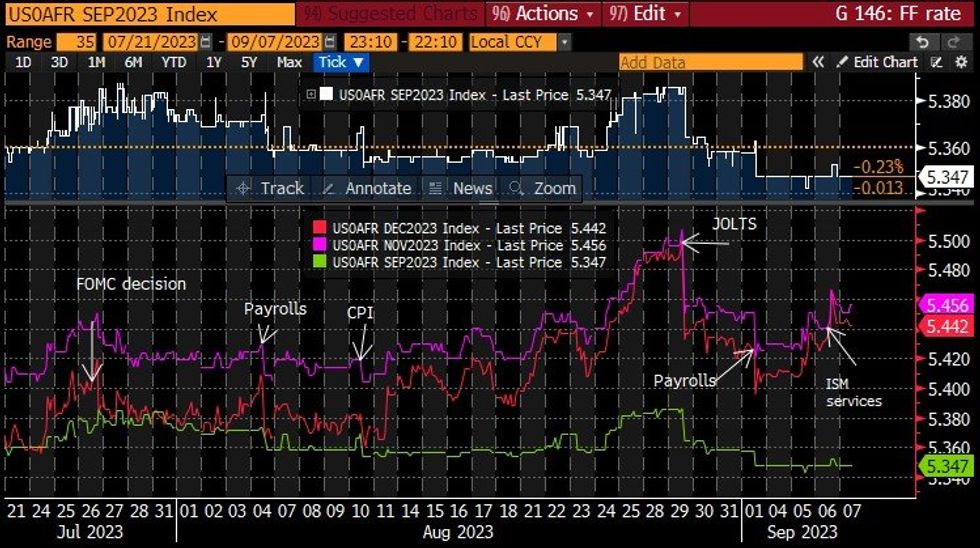

STIR FUTURES: Fed Implied Rates Nudge Lower, Chicago Fed On Lags From Tightening

- Fed Funds implied terminal pricing has consolidated yesterday’s pullback off highs and they continue to moderate a little further in 2024, but the surprise strength in ISM Services continues to hold sway.

- Cumulative hikes from 5.33% effective: +1.5bp Sep (unch), +12.5bp Nov (unch) to terminal 5.46%.

- Cuts from Nov terminal: 1.5bp to Dec’23, 38bp to Jun’24 (from 38bp) and 104bp to Dec’24 (from 101bp for new recent lows).

- There’s a stacked Fedspeak schedule, mostly tilted later in the session with Harker (’23), Goolsbee (’23), Williams (voter), Bostic (’24) and Bowman (voter) all lined up.

- This month’s Chicago Fed Letter wrote that “although the majority of the effects on output and inflation have already occurred, the policy tightening that has already been implemented will exert further restraint in the quarters ahead […] sufficient to bring inflation back near the Fed’s target by the middle of 2024 while avoiding a recession.” More here. https://www.chicagofed.org/publications/chicago-fed-letter/2023/483

Source: Bloomberg

Source: Bloomberg

TSYS: Early SOFR/Treasury Option Roundup: Mixed, Underlying Firmer

Mixed SOFR and Treasury option trade reported on modest volumes overnight. Underlying futures firmer but still well off Wed's pre-ISM Services data highs. Rate hike projections through year end running steady: Sep 20 FOMC is 6.8% w/ implied rate change of +1.7bp to 5.347%. November cumulative of +12.5bp at 5.456, December cumulative of 11.8bp at 5.449%. Fed terminal at 5.455% in Nov'23.

- SOFR Options:

- 2,000 SFRZ3 95.25/96.25 call spds vs. 2QZ3 97.5/98.5 call spd

- 2,000 SFRX3 94.62 calls ref 94.55

- 2,000 0QV3 94.87/95.25/95.50 broken put flys vs. 0QV3 96.25 calls

- 2,000 0QV3 95.25 puts ref 95.63

- 1,500 SFRV3 94.68 calls, 3.0 ref 94.55

- Treasury Options:

- 3,000 TYV3 111 calls, 15 ref 109-28

- 1,400 TYV3 108.25/109.25 2x1 put spds, 8 ref 109-21.5

EUROPE ISSUANCE UPDATE:

Spain auction results

Decent Spanish auction with the bid-to-cover picking up for both the 10-year and off-the-run 30-year Oblis (a little lower for the off-the-run 3-year but that is compared to its last reopening a year ago). The stop price for the nominals was all either in line (for the 3-year) or in excess of the pre-auction mid-price while Spain issued at the top of the target range at E6.445bln.

However, in line with other EGBs, we moved off the highs of the day in price terms which were seen immediately after the auction cut-off.

- E1.944bln of the 1.30% Oct-26 Obli. Avg yield 3.304% (bid-to-cover 1.78x)

- E2.598bln of the 3.55% Oct-33 Obli. Avg yield 3.663% (bid-to-cover 1.73x)

- E1.902bln of the 1.90% Oct-52 Obli. Avg yield 4.187% (bid-to-cover 1.95x)

- E483mln of the 1.00% Nov-30 Obli-Ei. Avg yield 1.025% (bid-to-cover 1.92x).

France auction results

It was an average French LT OAT auction. The stop price was above the pre-auction mid-price for all OATs sold but at less of a premium than the previous auction for each issue. Bid-to-covers were also lower for the 10/15-year OATs although for the latter that was largely due to the larger auction size today. The overarching decrease in general EGB pricing dominated any auction impact with prices of all OATs sold today trading below their stop price post-auction.

- E5.785bln of the 3.00% May-33 OAT. Avg yield 3.15% (bid-to-cover 1.72x)

- E2.336bln of the 1.25% May-38 OAT. Avg yield 3.42% (bid-to-cover 1.83x)

- E1.901bln of the 3.00% May-54 OAT. Avg yield 3.61% (bid-to-cover 2.17x).

EGBs: Off Lows, BTPs Tighten & GGBs Widen

A bounce in the Euro STOXX competes with the average to decent passage of French & Spanish supply in recent EGB trade, but those inputs generally nullify each other, leaving Bund futures around session bests, after recovering from a brief early look through yesterday’s low.

- A bid in Gilts, weaker than expected M/M domestic industrial production and a negative start for equities had provided support for Bunds earlier in the day.

- German cash benchmarks sit 2-3bp firmer with the 5- to 10-Year zone outperforming the wings.

- OAT futures have recovered from hedging/concession around the aforementioned auction process and trade just shy of session bests.

- Greek paper is a little wider in the long end, perhaps on some profit taking in compression trades ahead of tomorrow’s expected ratings update from DBRS Morningstar (although any upgrade to IG status for Greece won’t impact benchmark bond index GGB inclusion).

- Meanwhile, BTPs have unwound yesterday’s widening move, aided by the recovery in equities and some modest tightening in benchmark CDS indices. Also note that the Italian Treasury has announced that it will launch a new 5-Year retail-only BTP Valore with books open between 2-6 October (a reminder that the initial Valore offering saw strong demand).

GILTS: Early Richening Moves Extend On BoE DMP, 2 Further BoE Hikes No Longer Fully Priced

Initial BoE DMP reaction saw gilts extend their early rally and BoE-dated OIS soften further, although the moves have faded from extremes.

- The market reaction is best explained by noting the mixed releases within the DMP survey, as expected wage growth and expected price growth both fall - but realised wage growth picked up a little further. Overall this will probably be an encouraging report for the MPC, but in our view won't be enough to stop a September hike, and definitely keeps a November move on the table, too.

- Gilt futures have regained the 94 handle and operate through yesterday’s high, with initial resistance located at Tuesday’s high (94.55).

- Cash benchmarks sit 6-9bps richer as the curve bull steepens.

- SONIA futures flat to +13 through the blues, with the reds leading the bid.

- BoE-dated OIS prints 1-8bp softer on the session, with ~21bp of tightening showing for this month’s MPC, while terminal policy rate pricing moves below 5.75% i.e. 2x 25bp hikes from current policy rate levels are no longer fully priced.

FOREX: USD Index Remains Within Broad Uptrend

- Antipodean currencies outperform headed into the Thursday crossover, with AUD and NZD higher against most others. Despite the bounce off lows for AUD/USD, however, the bearish trend condition remains intact, with yesterday's 0.6357 low still within range and marking the bear trigger to open levels last seen in November.

- The USD Index remains in the medium-term uptrend drawn off the mid-July lows, with the index holding just below yesterday's multi-month high of 105.024. The JPY outperforms modestly, with markets clearly still heeding the verbal intervention from both Matsuno and Kanda earlier in the week.

- GBP is the poorest performer, resulting in fresh pullback lows for GBP/USD as the pair looks to the 200-dma at 1.2426 for support. BoE's Bailey appearing in front of lawmakers yesterday struck a somewhat dovish tone, stressing that the Bank of England are nearing the peak of their multi-year tightening cycle.

- US and Canadian data take focus going forward, with US weekly jobless claims data as well as Canadian Ivey PMI for August on the docket. The speaker slate is similarly busy, with ECB's Holzmann, Fed's Harker, Goolsbee, Williams, Bostic and Bowman making up the busy slate.

FX OPTIONS: Expiries for Sep07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0675-80(E588mln), $1.0700(E1.7bln), $1.0750-55(E839mln), $1.0780-90(E595mln), $1.0810-25(E983mln), $1.0840-50(E1.1bln), $1.0875-90(E1.5bln)

- USD/JPY: Y144.45-50($1.0bln), Y145.00-05($1.0bln)

- GBP/USD: $1.2550(Gbp821mln), $1.2700(Gbp1.3bln)

- AUD/USD: $0.6330(A$540mln), $0.6350-57(A$733mln), $0.6400-10(A$978mln)

- USD/CAD: C$1.3663($512mln)

- USD/CNY: Cny7.3000($525mln)

EQUITIES: NASDAQ 100 Mini Struggles, Apple Pressured Pre-Market

S&P 500 & NASDAQ 100 e-minis under some pressure early on with the negative lead out of China weighing.

- In terms of stock specific matters, pre-market headwinds have been noted for Apple (last indicated the best part of 3% weaker) on the back of a BBG source report suggesting that “China plans to expand a ban on the use of iPhones in sensitive departments to government-backed agencies and state companies, a sign of growing challenges for Apple Inc. in its biggest foreign market and global production base.”

- The major e-mini futures are flat to 0.6% lower, with the DJIA contract outperforming and the NASDAQ 100 leading the losses.

- Technically, the e-mini S&P 500 contract traded lower yesterday. Key resistance has been defined at 4,547.75, Sep 1 high. A break is required to reinstate the recent bullish theme. Note that recent gains in the contract stalled at the area of resistance around the former bull channel base - drawn from the Mar 13 low. The line intersects at 4,542.44. This is a bearish development and a continuation lower would expose key support at 4,350.00, the Aug 18 low.

EQUITIES: EuroStoxx50 Continues to Fade From Recent Highs

- The E-mini S&P contract traded lower yesterday. Key resistance has been defined at 4547.75, Sep 1 high. A break is required to reinstate the recent bullish theme. Note that recent gains in the contract stalled at the area of resistance around the former bull channel base.

- Eurostoxx 50 futures continue to pull back from the recent high. Attention is on support at 4225.00, the Aug 24 low. Clearance of this level would signal scope for a test of the key support at 4187.00.

Gold Narrows Gap With Key Support

- Gold traded lower again yesterday. Key support to watch lies at $1903.9, the Aug 25 low. A break of this level would be viewed as a bearish development and highlight the fact that the recovery between Aug 21 - Sep 1 has been a correction.

- The uptrend in WTI futures remains intact. The recent break of resistance at $84.16, the Aug 10 high, confirmed a resumption of the uptrend and this maintains the bullish price sequence of higher highs and higher lows. Note that moving average studies are in a bull mode position.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/09/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 07/09/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 07/09/2023 | 1230/0830 | * |  | CA | Building Permits |

| 07/09/2023 | 1230/0830 | ** | | US | Non-Farm Productivity (f) |

| 07/09/2023 | 1400/1000 | * | | CA | Ivey PMI |

| 07/09/2023 | 1400/1000 | * | | US | Services Revenues |

| 07/09/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 07/09/2023 | 1500/1100 | ** | | US | DOE Weekly Crude Oil Stocks |

| 07/09/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 07/09/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 07/09/2023 | 1755/1355 | | CA | BOC Governor Macklem gives "Economic Progress Report" speech in Calgary | |

| 07/09/2023 | 1930/1530 | | US | New York Fed's John Williams | |

| 07/09/2023 | 1945/1545 | | US | Atlanta Fed's Raphael Bostic | |

| 07/09/2023 | 2055/1655 | | US | Fed Governor Michelle Bowman | |

| 07/09/2023 | 2300/1900 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.