Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- JPY remains weak despite BoJ concern over import costs

- JPMorgan kick off earnings season with a beat on expectations

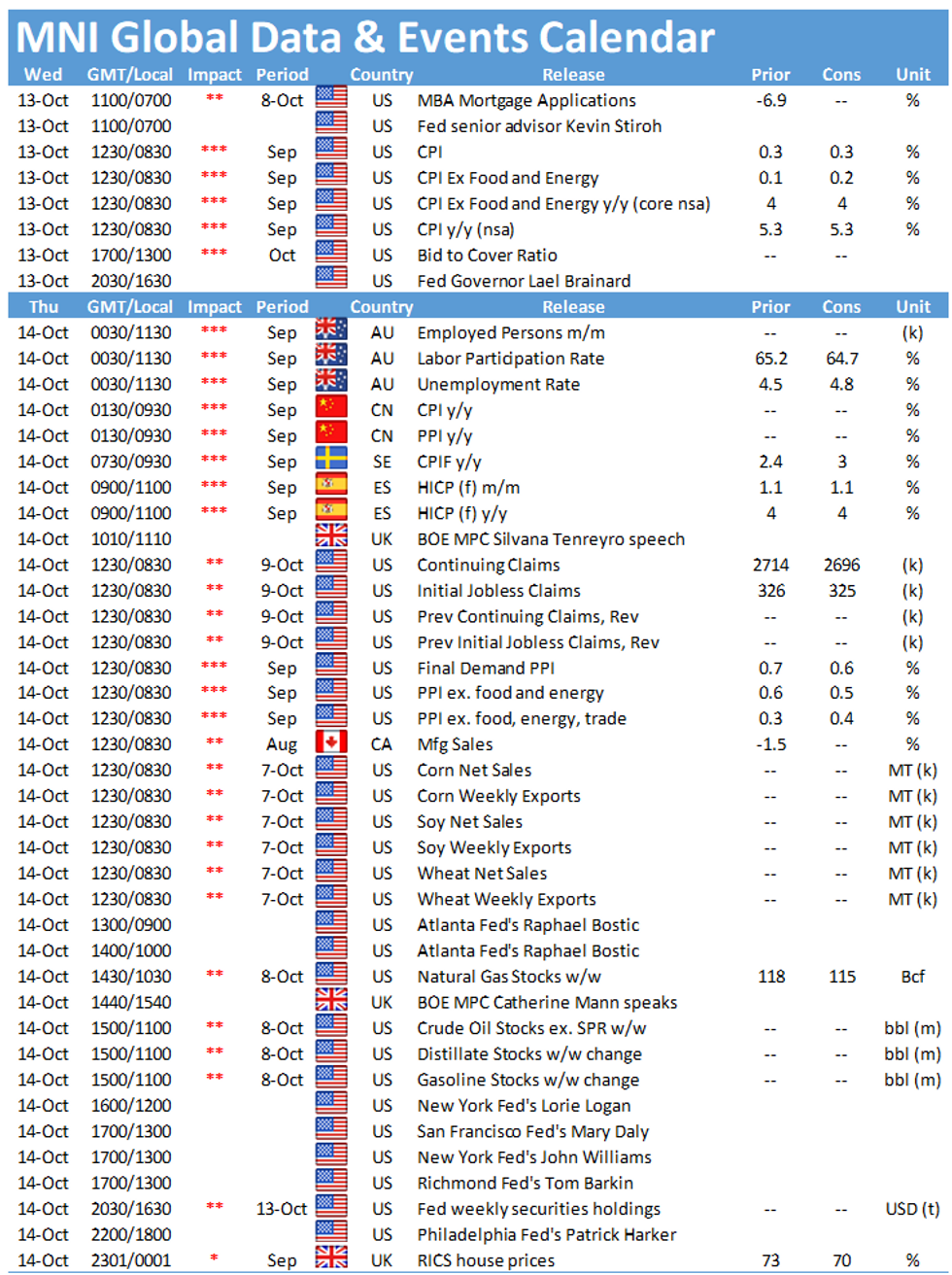

- CPI, FOMC minutes and 30y supply take focus

US TSYS SUMMARY: Busy Session Features CPI, 30Y Supply, And FOMC Minutes

Treasuries are a little stronger in overnight Wednesday trading, ahead of what promises to be an active session with data, supply, and Fed communications all in focus.

- Long end continues to strengthen ahead of 30Y supply today : 2-Yr yield is up 1bps at 0.348%, 5-Yr is down 0.2bps at 1.0695%, 10-Yr is down 1.4bps at 1.5629%, and 30-Yr is down 2.8bps at 2.0676%.

- Stocks are higher (financial stock qtly earnings eyed) and the dollar weaker.

- At 0830ET we get the September CPI report; headline M/M seen steady at 0.3%, core ticking up to 0.2% from 0.1%.

- Supply includes $35B 119-day bills at 1130ET, with the main event being $24B 30Y Bond re-open at 1300ET.

- Later, we get FOMC September minutes (1400ET) with any potential info on taper options keenly eyed, with Govs Brainard (1630ET) and Bowman (2000ET) also appearing.

- NY Fed buys ~$6.025B of 4.5-7Y Tsys.

EGB/GILT SUMMARY: Pushing Higher

European government bonds have rallied and curves have bull flattened alongside a mixed performance for equities.

- Gilts have outperformed, particularly at the long end where yields are 8bp lower on the day.

- Bunds have posted decent gains with yields 1-6bp lower across the curve.

- The OAT curve has similarly bull flattened with the 2s30s spread narrowing 5bp.

- UK monthly GDP came in marginally below expectations at 2.9% 3m/3m (3.0% consensus).

- Following of period of intensifying tensions between the UK and the EU over the Northern Ireland protocol, Brussels is reported to be considering proposals aimed at reducing bureacracy around checks on goods crossing the border. However, the role of the ECJ - a key sticking point for Westminster - appears to remain off the table in discussions.

- Supply this morning came from the UK (Gilt, GBP500mn), Germany (Bund, EUR816mn allotted) and Italy (BTPs, EUR6.5bn).

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXX1 169.50 put, sold at 85 and 84 in 10k (ref 168.86)

ERU3 100.00/99.75ps, sold at 4 in 5k (likely taking profit)

2RH2 100.50c, bought for half in 3.25k

UK:

3LZ1 99.00/98.50ps 1x1.5 sold at 16 in 5k

US:

TYZ1 130/127.5ps 1x2, bought for 16 in 1k

FOREX: JPY Remains Weaker Despite BoJ Concern

- For a third consecutive session, JPY is the poorest performing currency in G10, with USD/JPY securing a break above the multi-decade downtrendline drawn off the December 1975 high. Moves come alongside the Bank of Japan issuing caution over the weaker currency, with the central bank concerned that high energy import costs could crimp corporate profits and household spending.

- Elsewhere, GBP trades more favourably, with markets shrugging off a lower-than-expected monthly GDP reading in favour of strong industrial and manufacturing data for August. GBP/USD trades around 60 pips off the week's lowest levels, and now needs to top 1.3674 to secure any further progress.

- Equity futures trade in minor positive territory, with the e-mini S&P higher by 5-10 points ahead of the unofficial beginning of the earnings cycle. JPMorgan and BlackRock are the key reports Wednesday, with more financials names following on Thursday.

- US CPI takes focus going forward, with markets expecting CPI to hold at an above-target 5.3%. Core is also seen inline with the prior at 4.0%.

- Fed minutes cross later in the session, with markets focusing on the prospects for a November taper announcement. Central bank speakers due Wednesday also include BoE's Cunliffe and Fed's Brainard.

FX OPTIONS: Expiries for Oct13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500-15(E574mln), $1.1550-60(E703mln)

- EUR/GBP: Gbp0.8510-25(E1.2bln)

- USD/JPY: Y113.00($555mln)

- USD/CAD: C$1.2660-70($778mln)

- USD/CNY: Cny6.4200($1bln), Cny6.4500($1bln), Cny6.4800($1.3bln)

Price Signal Summary: Bond Gains Considered Corrective

- In the equity space, S&P E-minis remain below recent lows. The contract has failed to confirm a clear break of the 50-day EMA and instead price has pulled away from recent highs. This highlights a bearish risk and attention is on the key support and bear trigger at 4260.00, Oct 1 low. A clear break of the 50-day EMA - at 4387.11 today - is required to signal scope for a stronger bounce. EUROSTOXX 50 futures are also trading below recent highs with the 50-day EMA, as resistance, at 4090.50 still intact. Key support to watch is unchanged at 3949.50, the Oct 6 low.

- In FX, EURUSD is consolidating and recent price action appears to be a bear flag. The outlook remains bearish and the focus is on 1.1493 next, 50.0% of the Mar '20 - Jan '21 bull phase. The pair remains within a broad bear channel. GBPUSD continues to trade closer to recent highs and remains in a range. Until a short-term reversal is confirmed, the near-term path of least resistance remains up. A resumption of strength would open the 50-day EMA at 1.3711. USDJPY remains firm following the recent strong impulsive rally. The pair has breached 113.41, a multi-year trendline drawn from the Dec 1975 high. This reinforces bullish conditions and opens vol band resistance at 114.13.

- On the commodity front, Gold continues to consolidate. A short-term pivot support has been defined at $1746.0, Oct 6 low. There is scope for short-term gains while this level remains intact. A break though would be bearish. WTI trend conditions remain bullish. The focus is on $82.89, 1.764 projection of the Aug 23 - Sep 2 - Sep 9 price swing.

- In the FI space, the primary trend is unchanged and remains down. Gains are considered corrective. Recent Bund weakness has exposed 167.98, 2.382 projection of the Sep 9 - 17 - 21 price swing

- Gilt futures remain heavy too and the current recovery is likely a correction. The focus is on 123.27, 2.00 projection of the Aug 31 - Sep 17 - 21 price swing. Resistance is at 125.19, Oct 7 high.

EQUITIES: Stocks Higher to Kick Off Earnings Season

- Equity markets are higher ahead of the Wednesday cash open, with the e-mini S&P around 30 points off the Tuesday lows to narrow the gap with the near-term top at 4421.50.

- Across Europe, the tech sector is leading gains, with consumer discretionary and real estate firms following. Energy and financials are the laggards, but the downtick has been insufficient to counter strength in headline indices.

- Financials unofficially kick off the quarterly earnings cycle this week, with JPMorgan and Blackrock due Wednesday, with Bank of America, Wells Fargo, Morgan Stanley and Citigroup following on Thursday.

- Full schedule with timings and expectations found here: MNI US EARNINGS SCHEDULE - Banks Kick Off Quarterly Reporting Cycle - Bonds & Currency News | Market News

COMMODITIES: WTI, Brent Off Highs, But Remain Bullish

- WTI and Brent crude futures trade in minor negative territory, with both contracts rolling just off the week's cycle highs, in a move reminiscent of consolidation rather than any sentiment shift.

- This keeps the outlook bullish for oil markets in light of recent gains. Monday's gains confirmed an extension of the current bullish price sequence of higher highs and higher lows, reinforcing the uptrend. Note that the $80.00 psychological hurdle has also been cleared. The focus is on $82.89, a Fibonacci projection.

- Metals markets trade more positively, with gold and silver both in minor positive territory. Silver has made gains through the Monday/Tuesday highs to touch $22.87, with the next upside levels sitting at the October high of $23.19 and the 50-dma at $23.32.

MNI London Bureau | +44 203-865-3809 | edward.hardy@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok