Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Equities stabilise after late-week sell-off

- RBA blink, acts to stem rise in short-end yields

- Fedspeak in focus ahead of pre-meeting blackout period

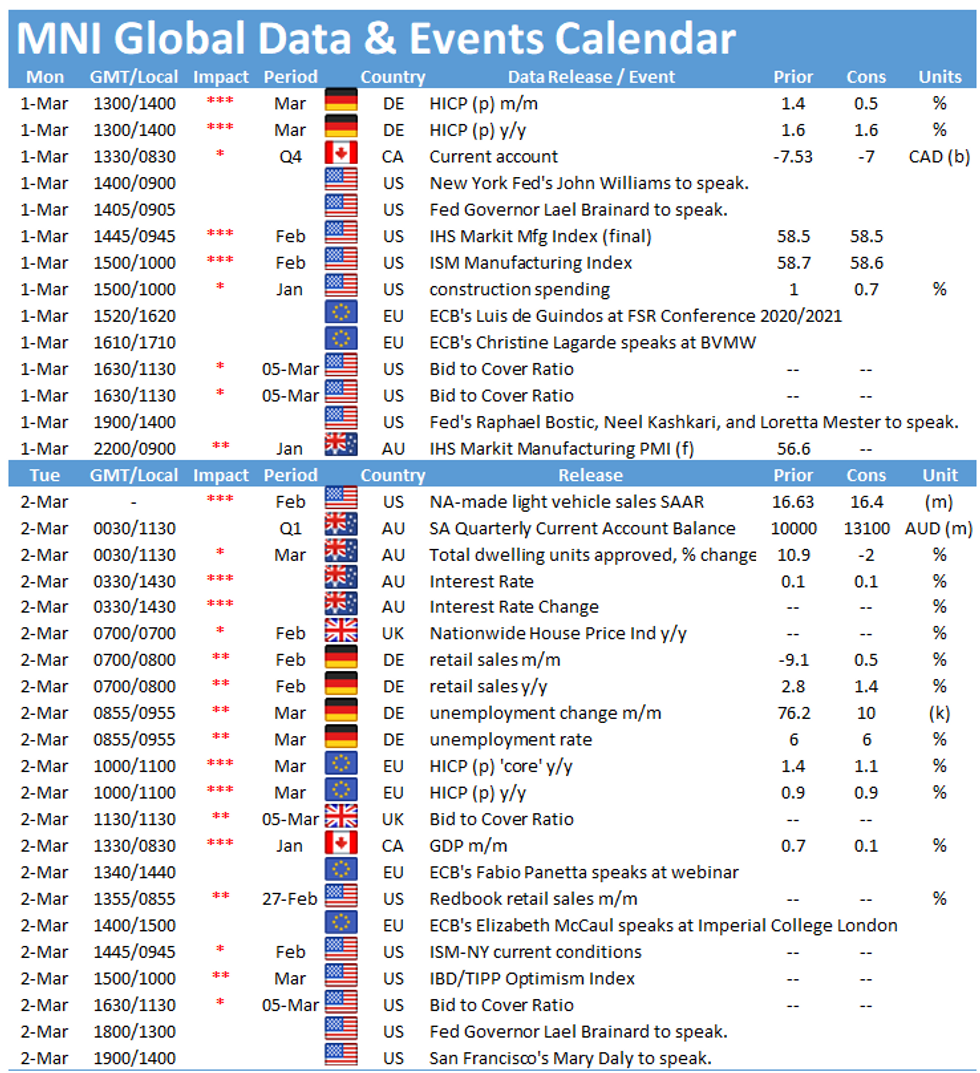

US TSYS SUMMARY: Long-End Yields Rebound

The Tsy curve has been bear steepening early Monday: 30s are underperforming with the short end/belly relatively anchored ahead of ISM data and Fed speakers.

- 30s are still well within Friday's ranges though (let alone the 29bps range beginning late Thursday thru end-week). The 2-Yr yield is up 0.2bps at 0.1289%, 5-Yr is down 1.6bps at 0.7153%, 10-Yr is up 3.6bps at 1.441%, and 30-Yr is up 6.9bps at 2.2198%.

- Jun 10-Yr futures (TY) up 12.5/32 at 133-3.5 (L: 133-02.5 / H: 133-16.5).

- Very much a risk-on session with a sea of green for commodities and equities overnight, with the dollar rebounding from early lows.

- Fed speakers get an opportunity to refine the FOMC's messaging post-Tsy selloff and pre-blackout period (which begins at week-end). NY Fed's Williams at 0900ET followed swiftly by Gov Brainard at 0905ET, with Bostic, Mester and Kashkari later at 1400ET.

- Final Feb PMI at 0945ET, followed by 1500ET's ISM manufacturing release alongside Jan construction spending.

- 1130ET sees 13-/26-week bill auctions for $105bn. NY Fed buys ~$2.425B of 1-7.5Y TIPS.

EGB/GILT SUMMARY: Broad Gains

European sovereign bonds have rallied this morning alongside gains for equities and commodities.

- Gilts opened higher and have gradually given up some of the early gains, while continuing to trade above Friday's closing levels. Cash yields are 1-3bp lower on the day, with the belly of the curve slightly outperforming. Focus this week will be on the budget this Wednesday with Chancellor of the Exchequer Rishi Sunak strongly hinting at the likelihood of tax rises - if not announced at this week, then at some point in this parliament.

- Bunds have rallied and the curve has bull flattened. Cash yields have edged down 1-4bp.

- OATs trade in line with bunds and the curve has similarly flattened. Last yields: 2-year -0.5970%, 5-year -0.5478%, 10-year -0.0589%, 30-year 0.6989%.

- BTPs have outperformed core EGBs with yields 4-6bp lower.

- Supply this morning came from Germany (Bubills, EUR5.08bn) and the Netherlands (DTCs, EUR2.15bn).

- Italian and Spanish manufacturing PMI data for February came in better than expected. German regional CPI data for February has broadly accelerated in Y/Y terms since January.

FOREX: Commodity-tied FX Stabilises After Last Week's U-Turn

Having traded among the poorest in G10 FX late last week, commodity-tied currencies are more stable, with AUD, NZD and CAD rebounding off recent lows.

- Markets continue to keep a close eye on volatility in government bond yields, with the RBA one of the first central banks to respond, having upped their bond purchase size to combat a recent rise in the front-end of the curve. Global stock markets are similarly more stable, with continental equities higher by close to 2% ahead of the NY crossover.

- Meanwhile, haven currencies are offered, with the CHF and JPY close to the bottom of the G10 pile. USD/CHF is now nearing the 200-dma after hitting new multi-month highs this morning.

- Focus turns to prelim German CPI data and February US ISM manufacturing numbers. Fedspeak should garner more interest, with speeches due from Fed's Brainard, Williams, Bostic, Mester and Kashkari. The ECB President Lagarde is also due, speaking in front of the German Association of SMEs.

CFTC: GBP's Bull Run Coincides With New 52w High in Positioning

- Friday's CFTC update showed the GBP net position among speculators was at a 52-week high, at 17.5% of open interest. Speculators added close to 9,000 contracts, pushing the 52-week Z-score to the highest of all currencies surveyed at 2.15.

- The uptick in GBP positioning coincided with a firm bull run for the currency, with the CFTC data collected on the same day that GBP/USD hit new multi-year highs of 1.4237.

- Markets also lifted CHF and, to a lesser extent, NZD and MXN.

- The JPY position worsened most notably, with a net 8,500 contracts sold, equivalent of 4.1% of open interest.

OPTIONS: Expiries for Mar 01 NY cut 1000ET (Source DTCC)

EUR/USD: $1.2000-05(E871mln), $1.2070-75(E667mln-EUR puts), $1.2200(E1.3bln), $1.2245-55(E1.6bln)

USD/JPY: Y104.95-00($517mln), Y105.40-45($785mln), Y105.55-57($2.0bln), Y106.20-25($1.8bln), Y106.45($1.65bln), Y106.50-55($720mln), Y106.75-85($766mln)AUD/USD: $0.7750(A$683mln-AUD puts), $0.7770(A$2.2bln), $0.7865-70(A$746mln)

AUD/NZD: $1.0730-35(A$567mln), N$1.0790-108.00(A$645mln)

NZD/USD: $0.6950(N$734mln), $0.7170-75(N$588mln), $0.7350(N$1.9bln-NZD puts)

USD/CAD: C$1.2500($1.25bln), C$1.2665-75($520mln)

USD/CNY: Cny6.40($520mln)USD/TRY: Try7.00($571mln)

TECHS: Price Signal Summary - USD Extends Gains

- Equity indices outlook is unchanged and the broader trend remains up with recent weakness considered a correction. E-mini S&P futures have managed so far to find support at the 50-day EMA.

- Key S/T support has been defined at 3785.00, Friday's low. A break would trigger a deeper sell-off.

- In the FX space, EURUSD is softer following a reversal from last week's 1.2243 high on Feb 25. A shooting star candle Thursday followed by a bearish engulfing candle Friday does not bode well for bulls. Watch key near-term support at 1.2023, Feb 17 low. USDJPY uptrend remains clearly intact with the focus on a climb towards 106.95, Aug 28, 2020 high.

- On the commodity front, Gold remains in a clear downtrend following last week's move through $1760.67, Feb 19 low. Gains are likely a correction. Resistance is at $1775.9, Feb 26 high. The focus is on $1700.0. Oil contracts remain firm although bulls have paused for breath. Brent (K1) targets the $70.00 psychological handle. WTI (J1) targets the round number resistance at $65.00.

- In the FI space, Bunds ended last week on a volatile note. The trend condition is oversold. Gains are considered corrective and firm resistance is seen at 175.12, the 20-day EMA. Gilts (M1) remains bearish. Scope is for a move towards the 127.00 handle. Resistance seen at 129.00, Feb 24 high and a key near-term resistance. The bear trigger in Treasuries is 131-31, Feb 25 low. The outlook remains bearish and targets 130-31, 76.4% of the Dec 2019 - Mar 2020 rally (cont).

EQUITIES: Stocks Stabilise, But No Sharp Recovery Yet

Continental stock markets are higher, with mainland indices up 1-1.5% a few hours after the European opening bell. Indices are primarily stabilising after the downside seen late last week, but the recovery is still well short of Thursday's best levels.

Across Europe, all sectors are in the green, with consumer discretionary and financials the best performers. Still higher, but at the bottom end of the table, are utilities and communication services.

The e-mini S&P continues to find support at the 50-dma of 3805.77. The index showed below there on Friday, but failed to close below - keeping the level intact for now.

COMMODITIES: Oil Partially Recoups Friday Losses

Both WTI and Brent crude futures trade higher ahead of the Monday session, but both are still well short of Friday's best levels and last week's cycle highs.

- Energy markets have received some support from middle-east tensions, after the Israeli Prime Minister traded barbs with Iran after an Israeli ship was damaged off the coast of Oman.

- Gold and silver are both in the green by around 0.5%. Price action is muted, however, with gold trading wholly inside the Friday range so far Monday.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.