Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Stocks bounce, but recovery shallow so far

- AUD firmer as RBA double down on taper plan

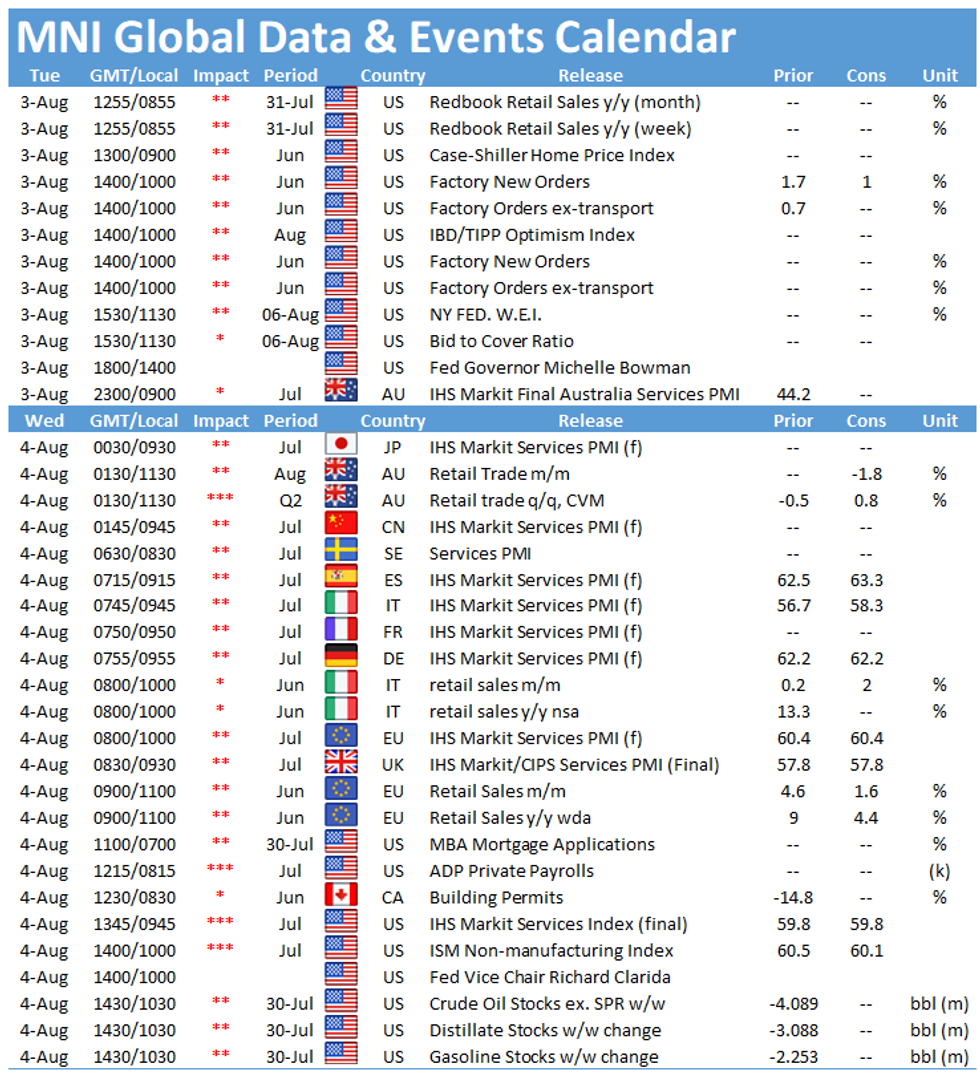

- Factory orders, final durable goods orders on deck

US TSYS SUMMARY: Edging Lower Ahead Of Factory Orders Data

Treasuries have slipped in the European morning and sit well off Monday's two-week highs, with modest bear steepening in the curve.

- The Tsy move has mirrored S&P eminis which have edged higher toward the 4,400 mark once again.

- Asia-Pac trade saw further concerns on China regulatory crackdown (auto chip sellers, internet gaming), while the RBA's steadfastness on tapering weighed on global FI.

- Sep 10-Yr futures (TY) down 5.5/32 at 134-26.5 (L: 134-25.5 / H: 135-01); avg volume (~275k). Still between support (133-26) and resistance (135-07, Jul 20 high and the bull trigger).

- 10Y underperforming: The 2-Yr yield is up 0.6bps at 0.1781%, 5-Yr is up 1.3bps at 0.6665%, 10-Yr is up 1.7bps at 1.1938%, and 30-Yr is up 1.5bps at 1.8645%.

- Factory orders and final durable goods orders feature at 1000ET.

- St Louis' Bullard said in a Reuters interview published 0600ET reiterating his call for the Fed to start and conclude tapering by early 2022.

- Fed Gov Bowman speaks at 1400ET.

- In supply, we get $20B 42-day bill auction at 1130ET. NY Fed buys ~$1.425B of 10-22.5Y Tsys.

EGB/GILT SUMMARY - Leaning steeper in early trading

EGBs are trading a touch in the red this morning, with curves flat/steeper on the margin.

- Bund is back towards flat on the session.

- German 2s/10s lean steeper, after we printed the flattest level since 15th February on the open.

- Support comes at 27.448, the 61.8% retracement of the Jan/May steepening bias (printed 27.974 low), now at 29.046.

- Peripherals are tighter, with Greece leading by 1.9bp.

- Gilts are mostly trading in line with EGBs, albeit better bid and up 6 ticks at the time of typing.

- UK 5/30s has traded in a limited range as investors sits on the sideline ahead of the BoE (Thursday), but more importantly the US NFP Friday.

- Range in the curve is 71.113/73.001, and short of yesterday's high at 73.685.

- Looking ahead, we have very little in terms of data, US Durable goods is Final, so more focus on Factory orders on the balance.

- Gilt futures are up 0.06 today at 130.10 with 10y yields up 1.6bp at 0.536% and 2y yields up 2.1bp at 0.048%.

- Bund futures are down -0.02 today at 176.80 with 10y Bund yields up 1.5bp at -0.473% and Schatz yields up 0.9bp at -0.770%.

- BTP futures are down -0.05 today at 154.79 with 10y yields up 1.1bp at 0.581% and 2y yields up 0.2bp at -0.483%.

- OAT futures are down -0.07 today at 162.33 with 10y yields up 1.4bp at -0.124% and 2y yields up 1.2bp at -0.709%.

EUROPE ISSUANCE UPDATE

UK DMO sells GBP 2.0bln 1.25% Jul-51 Gilt, Avg yield 0.972% (Prev. 1.274%), Bid-to-cover 2.41x (Prev. 2.24x), Tail 0.5bps (Prev. 0.2bps)

Austria sells:

- E700mln 0% Apr-25 RAGB, Avg yield -0.74% (Prev. -0.60%), Bid-to-cover 1.78x (Prev. 2.11x)

- E600mln 0% Feb-31 RAGB, Avg yield -0.27% (Prev. -0.06%), Bid-to-cover 1.81x (Prev. 1.86x)

EUROPE OPTION FLOW SUMMARY

Eurozone:

OEV1 135.5p, bought for 9 in 1.5k

DUU1 112.20/112.00ps, bought for half in 3k

UK:

0LZ1 vs 0LU1 99.75/99.87cs, bought the Dec for 1 in 2k

SFIM2 99.80/99.60ps 1x2, sold the 1 at half in 1k

US:

TYU1 136.5c, bought for '08 in 5,276

FOREX: AUD On The Up as RBA Double Down on Taper Plan

- AUD outperforms, with the currency seeing some support from the RBA rate decision, which ran against market expectations. The Bank chose to stick with its tapering plan, going against market consensus, pledging to continue to wind down purchases from A$5bln per week to A$4bln in early September. AUD/USD is just below the week's highs of 0.7408, with resistance seen at 0.7429, the high from Jul 19.

- The greenback is weaker inside a range, with the USD Index soft but still just above the Monday lows of 91.912 and last week's multi-month lows of 91.782.

- NOK is the strongest currency in G10, with the currency benefiting from a stabilisation in oil prices after Monday's downtick. USD/NOK eyes the formation of a golden cross in DMA space, with the 50-dma likely to top the 200-dma at some point this week.

- US factory orders and final durable goods orders numbers are the highlight on the data slate, with the speaker schedule also light. Fed's Bowman is due to give welcoming remarks at a Fed conference focused on low income and marginalized workers.

FX OPTIONS: Expiries for Aug03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1840-55($1.4bln), $1.1880-00(E1.0bln), $1.2000(E868mln)

- USD/JPY: Y110.00($775mln)

- USD/CAD: C$1.2480($1.2bln)

- USD/CNY: Cny6.4780($1bln), Cny6.5000($1.3bln)

Price Signal Summary - Bunds Extend Sequence of Higher Highs

- In the equity space, S&P E-minis outlook is bullish despite Friday's pullback. Recent gains confirmed a resumption of the uptrend and signal scope for a continuation near-term. Support to watch is at 4348.92, the 20-day EMA. EUROSTOXX 50 futures traded firmly from the Monday open, keeping the bullish short-term theme intact. This follows the recent print above a key near-term resistance at 4101.50, Jul 1 high. The breach of this level places on hold a recent bearish outlook and instead signals scope for a stronger recovery.

- In FX, the USD is weaker. EURUSD traded higher Thursday and Friday to clear a former resistance at 1.1851, Jul 15 high. The extension has exposed the 50-day EMA at 1.1916. GBPUSD traded higher again Friday before fading into the close. The pair has cleared the 50-day EMA. The move above this average strengthens the current corrective recovery, signalling scope for gains towards 1.3990 next, a Fibonacci retracement. USDJPY resumed the modest decline Monday, edging through the Friday lows to print down at 109.20. A bearish focus dominates. This follows the recent Jul 19 break of support at 109.48, Jul 29 low.

- On the commodity front, Gold has faded off last week's highs, but remains in recovery mode after printing 1790.0 in mid-July. The outlook is bullish and the recent pullback was considered corrective. Brent futures corrected Monday, slipping over $2.50 as markets gravitated back toward the 50-dma at $72.33.

- Within FI, Bund futures rallied through last week's highs with relatively little effort early Monday, keeping the ball in bulls' court. The current bullish sequence of higher highs and higher lows remains intact and this signals scope for a climb towards 177.19 next, a Fibonacci extension. BTPs remain bullish and are trading at recent highs. A positive outlook follows the recent resumption of the uptrend that started May 19 - gains on Jul 6 and 7 resulted in a breach of a former key resistance at 152.47.

EQUITIES: Stocks Stronger, But Bounce in US Futures Shallow

- European equities are uniformly higher, with outperformance in France's CAC-40 (+0.9%), with the recovery in stocks also evident across US futures. Nonetheless, the e-mini S&P bounce has been shallow so far, with the week's highs of 4419.75 still a way off at current levels.

- Europe's energy and healthcare sectors are driving the way higher Tuesday, with an alleviation of pressure on oil prices helping soothe sentiment.

- Earnings from Willis Towers Watson, ConocoPhillips and Eli Lilly cross Tuesday.

COMMODITIES: Copper Weaker As China Slowdown Fears Persist

- WTI Crude up $0.57 or +0.8% at $71.39

- Natural Gas up $0.04 or +0.97% at $3.978

- Gold spot down $3.33 or -0.18% at $1809.72

- Copper down $4.65 or -1.05% at $440.95

- Silver unchanged at $25.3183

- Platinum down $4.84 or -0.46% at $1054.93

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok