Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

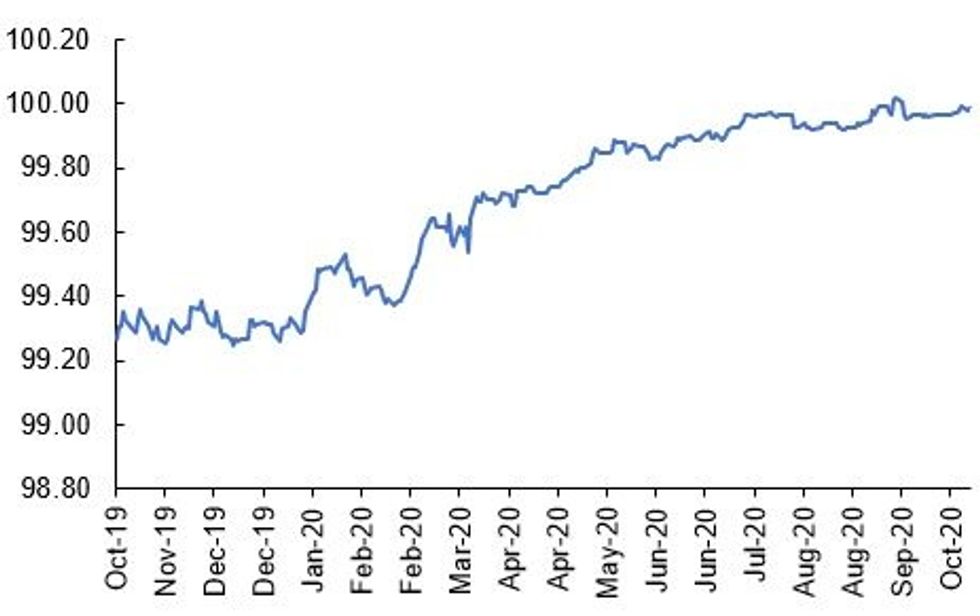

Fig 1. Mar-21 Short Sterling Futures Contract

Source: MNI/Bloomberg

US TSYS SUMMARY: Last Call For Pre-Election Stimulus

Treasuries are retesting Monday's lows as progress on fiscal stimulus remains in the balance.

- Dec 10-Yr futures (TY) down 5.5/32 at 138-24 (= today's and Monday's low), with the curve a bit steeper: 2-Yr yield is unchanged at 0.1451%, 5-Yr is up 0.5bps at 0.3393%, 10-Yr is up 1.3bps at 0.7824%, and 30-Yr is up 1.6bps at 1.5752%.

- Today marks Speaker Pelosi's "deadline" for seeing whether a stimulus deal is possible before election day (in 2 weeks). She and Treas Sec Mnuchin spoke Monday and both sides saw progress made, but as Politico reports this morning, the appropriations staff "found themselves immediately deadlocked" on some issues Monday aft., and Senate passage will be difficult.

- This subject may come up w Pres Trump on Fox and Friends at 0800ET.

- A heavy Fed speaker slate, but judging from yesterday's non-reaction to the likes of Powell and Clarida, doesn't figure to be market-moving today. VC Quarles at 1050ET, Chicago's Evans at 1300ET, NY Fed VP Singh at 1330ET, Gov Brainard at 1500ET, and Atlanta's Bostic at 1700ET.

- Data: 0830ET sees Sep Housing starts/building permits and Oct Philly Fed non-manuf.

- $60B of 42-/119-day bill auction at 1130ET; NY Fed buys ~$6.025B if 4.5-7Y Tsys.

BOND SUMMARY: Vlieghe Hints At Further Easing

European govies trade weaker this morning with price action relatively contained in core markets and the EGB periphery underperforming.

- Gilts have lacked convincing direction this morning with yields holding within 1bp of yesterday's close.

- It is a similar story for bunds. Last yields: 2-year -0.788%, 5-year -0.8084%, 10-year -0.617%, 30-year -0.2041%.

- BTPs have sold off with the curve bear steepening. Cash yields are 2-5bp higher on the day with the 2s30s spread 3bp wider.

- Supply this morning came from the UK (Gilt linker, GBP600mn) Germany (Schatz, EUR3.665bn) and the ESM (bills, EUR2bn).

- Speaking earlier today, the BoE's Vlieghe indicated that the risks are skewed in the direction of further monetary stimulus and that the risks of negative rates being counterproductive is low.

- The ECB's Hernandez de Cos will be speaking in Madrid at 1250BST.

- It has been another quiet day for the data calendar with no tier one releases.

DEBT SUPPLY

GILT AUCTION RESULTS: DMO sells GBP600mln nominal of the 1.25% Nov-32 linker

- Avg real yield -2.976% (-2.853%), bid-to-cover 3.16x (2.51x), price 162.030 (161.160)

- Pre-auction mid-price 161.528

- An additional GBP150mln nominal will be available through the PAOF to successful bidders until 13:00BST.

GERMAN AUCTION RESULTS: Germany Allots E3.3665bn of the 0% Sep-22 Schatz

- Average yield -0.80% (-0.73%), Buba cover 2.0x (1.65x), bid-to-cover 1.71x (1.33x)

ESM AUCTION RESULTS: The ESM Sells E2bn of 6-Month Bills

- Average yield -0.629%, bid-to-cover 5.55x

OPTIONS

SHORT STERLING OPTIONS: Call Calendar

0LZ0/3LZ0 100c calendar, sold the 1yr at 4 and 3.75 in 1.5k

TECHS

US 5YR FUTURE TECHS: (Z0) Under Pressure

- RES 4: 125-316 High Oct 5

- RES 3: 125-30+ 61.8% retracement of the Sep 30 - Oct 7 sell-off

- RES 2: 125-31 High Oct 15

- RES 1: 125-26 High Oct 19

- PRICE: 125-23 @ 11:36 BST Oct 20

- SUP 1: 125-21 Low Oct 9

- SUP 2: 125-202 Low Oct 7 and the bear trigger

- SUP 3: 125-18 Low Aug 28 (cont)

- SUP 4: 125-16+ 1.00 proj of Aug 4 - 13 sell-off from Sep 3 high

5yr futures maintain a softer tone. The move below 125-23+ yesterday, Oct 13 low exposes the key support at 125-202, Oct 7 low. A break of this level would negate recent bullish developments and instead confirm a resumption of the downtrend that has been in place since early August. This would pave the way for weakness towards 125-16+, a Fibonacci projection. Key short-term resistance is at 125-31.

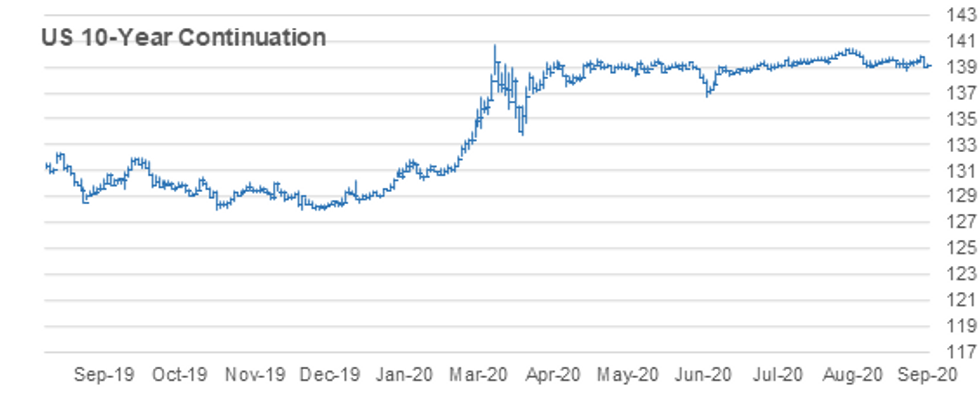

US 10YR FUTURE TECHS: (Z0) Attention Turns To Support

- RES 4: 139-25 High Oct 2

- RES 3: 139-17 76.4% retracement of the Sep 29 - Oct 7 sell-off

- RES 2: 139-14 High Oct 15

- RES 1: 139-01+ High Oct 20

- PRICE: 138-24+ @ 11:43 BST Oct 20

- SUP 1: 138-20+ Low Oct 7 and the bull trigger

- SUP 2: 138-18+ Low Aug 28 and the bear trigger

- SUP 3: 138-16+ Low Jun 23 (cont)

- SUP 4: 138-12 61.8% retracement of the Jun - Aug rally (cont)

Treasuries have reversed last week's positive tone and remain weaker. Yesterday's move lower marks an extension of the pullback from 139-14, Oct 15 high. The move through support at 138-28+, Oct 13 low exposes 138-20+, Oct 7 low and 138-18+, Aug 28 low. The latter is the bear trigger where a break would signal a resumption of the reversal that occurred on Aug 4. This would open 138-04+, a Fibonacci projection. Firm resistance is at 139-14.

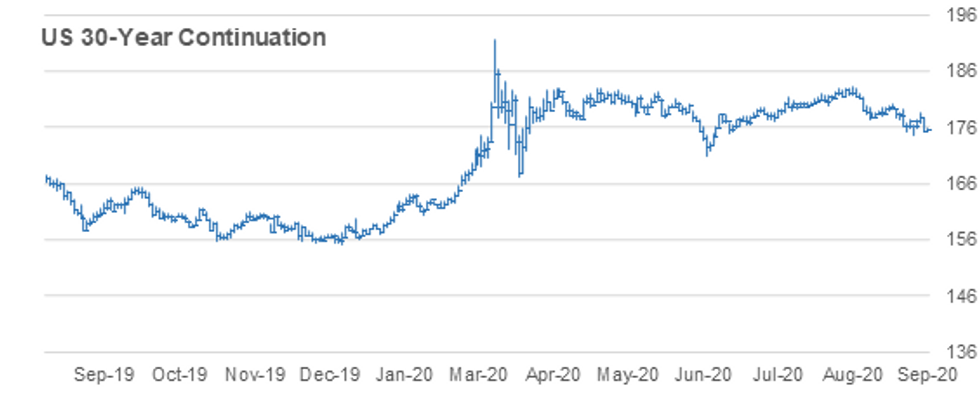

US 30YR FUTURE TECHS: (Z0) Approaching The Bear Trigger

- RES 4: 177-14 High Sep 17 and a bull trigger

- RES 3: 177-00 High Oct 2

- RES 2: 176-10 High Oct 15

- RES 1: 174-27 High Oct 19

- PRICE: 173-30 @ 11:50 BST Oct 20

- SUP 1: 173-10 Low Oct 7 and the bear trigger

- SUP 2: 172-17 Low Jun 5 (cont)

- SUP 3: 172-13 0.764 proj of Aug 6 - 28 downleg from Sep 3 high

- SUP 4: 172-00 Round number support

30yr futures are trading lower having started the week on a softer note. Price has breached 174-08, Oct 13 low, exposing the key level at 173-10, Oct 7 low. A break of 173-10 would negate recent bullish developments and instead confirm a resumption of the downtrend that has been in place since the Aug 6 reversal. This would open 172-17, Jun 5 low (cont) and 172-13, a Fibonacci projection. Key resistance has been defined at 176-10, Oct 15 high.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.