Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- UK NOV GDP BEATS FORECASTS, EXCEEDS PRE-COVID LEVEL

- GERMAN ECONOMY SHRANK AS MUCH AS 1% IN Q4

- BOJ READY TO DEFEND YIELD CURVE ON ANY FED MOVES (MNI INSIGHT)

- CYBERATTACK HITS UKRAINE OFFICIAL SITES AMID RUSSIA TENSIONS

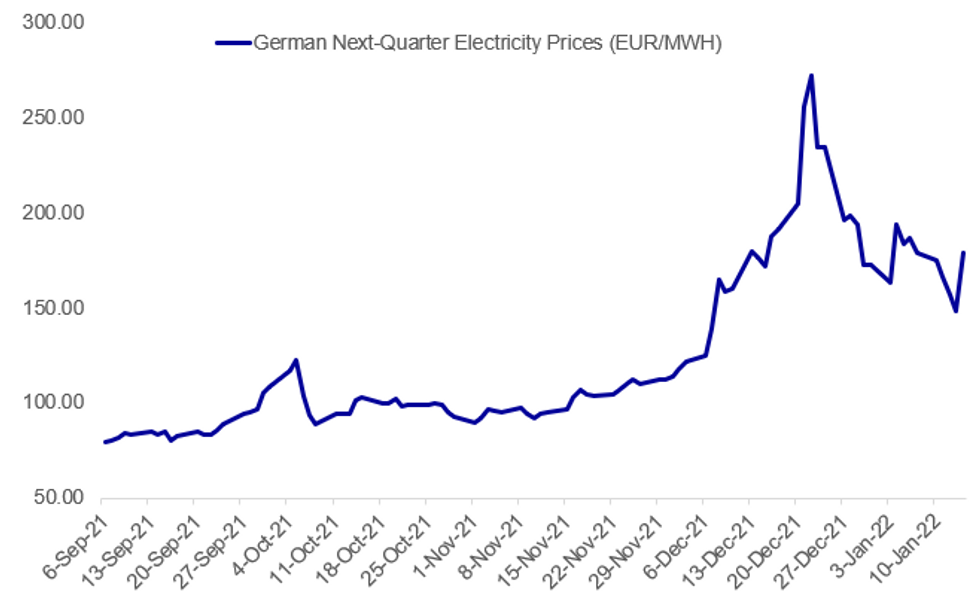

- EUROPEAN POWER PRICES JUMP AFTER EDF CUTS NUCLEAR FORECAST

Fig. 1: Europe Power Price Woes Continue

Source: BBG, MNI

Source: BBG, MNI

NEWS:

BOJ (MNI INSIGHT): Bank of Japan officials are ready to fight any surges in 10-year bond yields through fixed-rate purchase operations for consecutive days if the U.S. Fed tapering and expected rate hikes bring on financial market pressures this year, MNI understands. For full article contact sales@marketnews.com

GERMAN DATA (BBG): Germany’s economy contracted by as much as 1% in the final quarter of 2021 as the emergence of the coronavirus’s omicron strain added to drags on output from supply snarls and the fastest inflation in three decades.Gross domestic product shrank by between 0.5% and 1% in the three-month period, the Federal Statistics Office said Friday at a briefing. For the year as a whole, it advanced 2.7%, in line with expectations.

UKRAINE/RUSSIA (BBG): Ukraine said a cyberattack brought down the websites of several government agencies for hours. Authorities didn’t immediately comment on the source of the outage, which comes as tensions with Russia surge over its troop buildup near the border. “Some government websites, including the Foreign Ministry and Education Ministry, came under hacker attack overnight,” the State Security Service said Friday. Ukraine has previously accused Russia of mounting major cyberattacks against it as relations between the two neighbors have worsened since a 2014 conflict. In recent months, Ukraine and its allies in the U.S. and Europe have warned that Russia could be preparing to invade as it massed about 100,000 troops near the border. Moscow denies any such plans.

EUROPE ENERGY (BBG): French and German electricity prices jumped after Electricite de France SA revised down the production forecast for its nuclear fleet that’s vital to keep the lights on in Europe. The world’s biggest producer of nuclear power reduced its estimate by about 8% after finding defects at some reactors. It’s another blow to Europe which is already facing an historic energy crisis with natural gas stocks at their lowest in more than a decade for this time of year. The German February contract rose as much as 22% to 235.50 euros ($270.07) a megawatt-hour while the contract for the next quarterclimbed as much as 23% to 183 euros on European Energy Exchange AG. French contract for April to June delivery added as much as 24% to 191 euros.

UK POLITICS: Latest general election opinion polling from YouGov shows the main opposition Labour party with an 11% lead over Prime Minister Boris Johnson's Conservative party, the widest Labour lead over the Conservatives in a YouGov poll since December 2013.

- Westminster Voting Intention: LAB: 40% (+2), CON: 29% (+1), LDM: 11% (-2), GRN: 6% (-1), RFM: 6% (+2), SNP: 5% (=). Via @YouGov, 12-13 Jan. Changes w/ 11-12 Jan.

- The sustained revelations about rule-breaking parties at Downing St during COVID lockdowns in 2020 and 2021 continue to damage public support for the gov't, with the latest story alleging a party took place on the eve of the funeral of HRH Prince Phillip, the Duke of Edinburgh, consort to Queen Elizabeth II.

COVID (BBG): The omicron coronavirus variant causes less severe disease than the delta strain even in those who are unvaccinated or who haven’t had a prior Covid-19 infection, a study from South Africa’s Western Cape province showed. The research in the region where Cape Town is the capital compared 11,609 patients from the first three waves of infection, the most recent of which was caused by the delta variant, and 5,144 patients from the latest omicron-driven wave.

BANK OF KOREA (MNI STATE OF PLAY): The Bank of Korea on Friday raised its policy interest rate to the pre-pandemic level of 1.25% amid persistent concerns over inflation and financial imbalances as it keeps a close eye on the impact of the Omicron variant spread. "The Board will appropriately adjust the degree of monetary policy accommodation as the Korean economy is expected to continue its sound growth and inflation to run above the target level for a considerable time, despite underlying uncertainties over the virus," a statement released by the BOK said.

DATA:

SPAIN DEC HICP +1.1% M/M, +6.6% Y/Y; NOV +5.5% Y/Y

Spanish CPI Surges

SPAIN DEC HICP +1.1% M/M, +6.6% Y/Y; NOV +5.5% Y/Y

SPAIN DEC CPI +1.2% M/M, +6.5% Y/Y; NOV +5.5% Y/Y

- Spanish headline inflation surged to +6.5% y/y, +1.2% m/m.

- HICP was +6.6% y/y, +1.1% m/m

- This was weaker than flash estimates, which priced December inflation at +6.7% y/y for both HICP and CPI readings, and monthly growth 0.1pt higher

UK NOV GDP +0.9% M/M (MEDIAN +0.4%, OCT +0.21.0%,)

MNI BRIEF: UK Nov GDP Beats Forecasts, Exceeds Pre-Covid Level

UK GDP jumped by 0.9% in November, far outpacing forecasts of a 0.4% rise, taking output 0.7% above the pre-Covid-19 level seen in February 2020, the Office for National Statistics said Friday. Services rose by 0.7%, adding 1.05 percentage points to total output. Education and retail were particularly strong, but services were robust across the board, according to an ONS official.

Manufacturing rose by 1.1% in November, lifting total production by 1.0%, despite a 1.3% decline in mining and quarrying.

Construction jumped by 3.5%, as shortages of materials that contributed to a sharp fall in October “eased slightly,” according the official. Mild November weather also lifted the sector.

MNI BRIEF: UK Nov Trade Surplus Biggest Since August 2020

External trade was in surplus in November, to the tune of GBP626 million, up from GBP151 million in October, the biggest surplus since August 2020, the Office for National Statistics said Friday.

Exports rose by 4.6%, while imports increase by 3.8%. The deficit in goods trade narrowed slightly to GBP11.337 billion from 11.807 billion in October.

As has been the case since the UK left the transitional trading arrangement with the European Union at the tart of the year, non-EU imports exceeded incoming shipments from the EU, with the gap widening to GBP3.8 billion, the highest of any month in 2021. Fuel imports accounted for much of the increase.

FIXED INCOME: Partially retracing yday's rally

Core fixed income is off of yesterday's highs and futures have broadly retraced a bit over half of yesterday's moves higher. The Treasury and gilt curves have done this as part of a parallel shift while the German 2s10s curve has bear steepened.

- UK data this morning was better than expected and GDP is now above the pre-pandemic level, but its hard to see it having too much of a sway on the MPC who are much more focused on inflation and labour market data than pre-Omicron activity data.

- The main events of the day will be US data. Retail sales and industrial production for December will both be closely watched but perhaps even more important will be the inflation surveys within the Michigan confidence data.

- TY1 futures are down -0-9 today at 128-14 with 10y UST yields up 3.8bp at 1.744% and 2y yields up 3.8bp at 0.933%.

- Bund futures are down -0.37 today at 170.34 with 10y Bund yields up 2.2bp at -0.107% and Schatz yields up 1.3bp at -0.595%.

- Gilt futures are down -0.28 today at 123.37 with 10y yields up 3.6bp at 1.140% and 2y yields up 3.3bp at 0.788%.

FOREX: USD Downtrend Pauses on Wall Street Slide

- Currency markets are in consolidation mode early Friday, with the greenback holding its ground and pausing the recent downtrend. Nonetheless EUR/USD gains overnight managed to put the pair at a new cycle high of 1.1483, again narrowing the gap with the next key level at the 100-dma of 1.1507.

- The pause in the USD downtrend follows the resolutely negative close on Wall Street yesterday, with the tech-led NASDAQ closing lower by just over 2.5% on the day. As a result, JPY has seen some support so far today, while recent outperformers including the AUD and NZD are at the bottom of the pile.

- USD/CNH made another attempt on recent cycle lows early Friday, dropping to touch 6.3425 before bouncing on reports that China's SAFE regulator had tightened restrictions on 'underground banks' and their interactions with the forex market.

- December retail sales numbers take focus in the US session, with markets expecting sales to have dropped 0.1% across the month, with the prelim Uni of Michigan confidence release following shortly afterward. Central bank speakers of note include ECB's Lagarde and Fed's Williams.

EQUITIES: U.S. Futures Off Overnight Lows

- Asian markets closed weaker: Japan's NIKKEI closed down 364.85 pts or -1.28% at 28124.28 and the TOPIX ended 27.92 pts lower or -1.39% at 1977.66. China's SHANGHAI closed down 34.003 pts or -0.96% at 3521.256 and the HANG SENG ended 46.45 pts lower or -0.19% at 24383.32

- European stocks are lower, with the German Dax down 102.16 pts or -0.64% at 16031.59, FTSE 100 down 5.6 pts or -0.07% at 7563.85, CAC 40 down 46.44 pts or -0.64% at 7201.14 and Euro Stoxx 50 down 36.27 pts or -0.84% at 4315.9.

- U.S. futures, conversely, are a little stronger. with the Dow Jones mini up 84 pts or +0.23% at 36073, S&P 500 mini up 8.5 pts or +0.18% at 4660.5, NASDAQ mini up 17.5 pts or +0.11% at 15507.75.

COMMODITIES: Oil Leading Gains

- WTI Crude up $0.57 or +0.69% at $82.23

- Natural Gas down $0.1 or -2.41% at $4.153

- Gold spot up $1.45 or +0.08% at $1827.77

- Copper down $0.75 or -0.17% at $451.9

- Silver up $0.05 or +0.21% at $23.213

- Platinum up $6.2 or +0.64% at $983.98

LOOK AHEAD:

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/01/2022 | 1315/1415 |  | EU | ECB Lagarde speech at COSAC | |

| 14/01/2022 | 1330/0830 | *** |  | US | Retail Sales |

| 14/01/2022 | 1330/0830 | ** | | US | import/export price index |

| 14/01/2022 | 1415/0915 | *** | | US | Industrial Production |

| 14/01/2022 | 1500/1000 | *** | | US | University of Michigan Sentiment Index (p) |

| 14/01/2022 | 1500/1000 | * | | US | business inventories |

| 14/01/2022 | 1500/1000 | | US | Philadelphia Fed's Patrick Harker | |

| 14/01/2022 | 1600/1100 | | US | New York Fed's John Williams | |

| 14/01/2022 | 1700/1200 |  | CA | BOC releases climate risk paper |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.