Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- ECB'S VILLEROY, MULLER INDICATE NO CHANGE IN TOTAL PEPP VOLUMES

- B.O.J. IS SAID MULLING ANALYSIS TO SUPPORT SCOPE FOR RATE CUT

- ITALY TO TIGHTEN COVID-RELATED RESTRICTIONS

- UK GDP LOWER IN JANUARY, BUT BEATS EXPECTATIONS

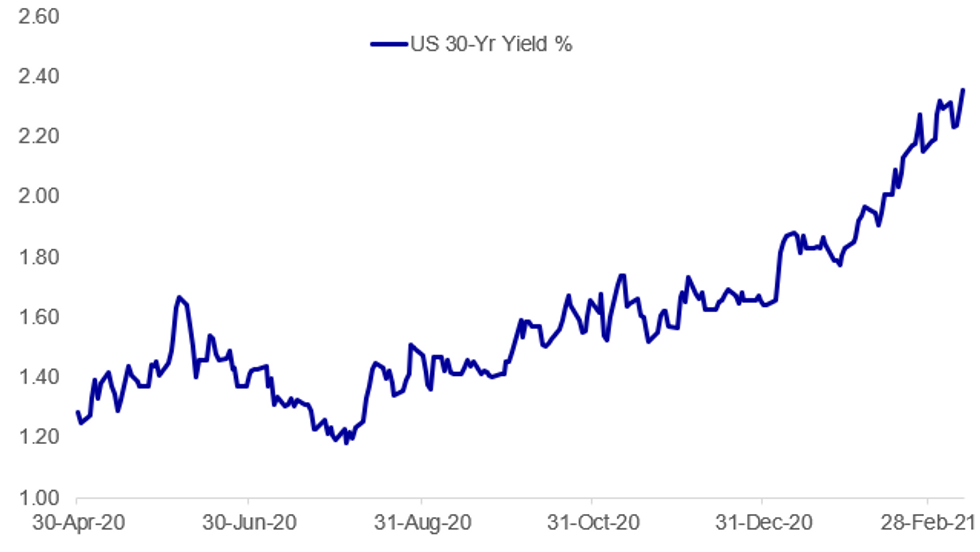

Fig. 1: Treasury Yields On The March Higher...Again

BBG, MNI

BBG, MNI

NEWS:

ECB (BBG): Bank of France Governor Francois Villeroy de Galhau says there was no discussion of changing the size of the PEPP asset purchase program at the European Central Bank's meeting Thursday"There was no discussion yesterday on the total amount of the envelope. We simply repeated there would be flexibility if necessary," Villeroy says in an interview on Boursorama website"When financing conditions are naturally favorable we can buy less. When there is a tension, we must buy more. That is what flexibility means"

ECB (BBG): European Central Bank Governing Council member Madis Muller says on Estonian central bank website that asset purchases under the ECB's pandemic program will be increased "temporarily." "But their planned total volume will remain the same"

ECB (RTRS): Struggling under the third wave of the COVID-19 pandemic, the euro zone economy will need at least until the autumn to turn a corner, outgoing Lithuanian central bank chief Vitas Vasiliauskas told reporters on Friday. Asked when the European Central Bank could dial back emergency bond purchases, Vasiliauskas said this could only happen when the recovery is underway and the economy is off life support. "The turning the turning point would be when we see clearly that growth returns to track and the economy breathes on its own," Vasiliauskas, a member of the ECB's Governing Council said. "It's difficult to see this before the autumn."

B.O.J. (BBG): At next week's policy review, the Bank of Japan is considering releasing an analysis of the potential impact of lowering its negative interest rate to show its determination to use this option if needed, according to people familiar with the matter.BOJ officials say the assessment would hint at the likely results of a lower negative rate on commercial banks, and would serve as a basis for measures the central bank could take to alleviate the side effects of such a move, the people said.The BOJ will release details of its review on March 19.

B.O.J. (RTRS): The Bank of Japan will likely insert clearer guidance in its policy statement on what it sees as an acceptable level of fluctuation in long-term interest rates, sources said, in an effort to show it won't tolerate rises that hurt the economy. The move would be part of the BOJ's review of its policy tools next week, which aims to make its stimulus programme more sustainable as the coronavirus pandemic pushes inflation further away from the bank's 2% target.

ITALY (ANSA): The government intends to make almost the whole of Italy a COVID-19 'red zone' from April 3 to 5, a period which includes Easter Sunday and Easter Monday, sources said Friday as Premier Mario Draghi's administration held talks with regional governments and other local authorities on new restrictions. Draghi's government is set to impose a new regime of measures in force from March 15 until April 6, with COVID-19 cases rising sharply in Italy, the sources said. Red is the maximum level in Italy's tired system of coronavirus restrictions.

UK GILTS: No real surprises in the gilt auction calendar, coming in line with ourexpectations. The DMO has left the option to decide what new linker it launches viasyndication in May and broadened the range from 15-25 years (as opposed tothe 20-25 years it had mentioned ahead of the consultation). MNI expects this could be because there was demand for both a 2039 and a2043/2045 linker. Our base case would be we get a 2039 and 2045 launched at the next two linker syndications but that the DMO will look more into the demand for both to decide which is launched first.

DATA:

UK Monthly GDP Falls As Lockdown Kicks In

JAN GDP -2.9% M/M (PREV +1.2%), -9.2% Y/Y (PREV -6.5%)

JAN INDEX OF SERVICES -3.5 % M/M; -10.4% Y/Y; PRV +1.7% M/M, MED -5.8%

JAN IND PRODUCTION -1.5% M/M, PRV +0.2%, MED -0.5%

JAN MANUFACTURING -2.3% M/M, PRV +0.3%, MEDIAN -0.8%

JAN CONSTRUCTION +0.9% M/M, PRV -2.9%, MEDIAN -1.0%

The national lockdown in Jan led to a sharp drop in m/m GDP, falling by 2.9%, coming in stronger than expected (BBG: -5.0%). This marks the lowest reading since Apr where GDP fell by 18.3% and it was slightly worse than Nov's 2.3% drop. The decrease was led by the service sector which contracted by 3.5% m/m. Within services, accommodation and food services saw the largest fall of 28.1%, while health services saw the largest uptick, up 5.9%, mainly driven by the vaccine rollout and increased testing. Other services, including hairdressers, plunged by 20.7%, while Education output dropped by 16.3% in Jan as schools remained closed. While industrial production slipped 1.5%, manufacturing output dropped 2.3%, both coming in weaker than anticipated. Both indicators show the first decline since Apr with car manufacturing decreasing significantly.

Imports and exports to the EU declined sharply in Jan due to temporary factors such as delivery delays, stockpiling, a change of reporting at the end of the transition period, etc. Early indicators suggest a recovery towards the end of the month.

EZ production rebounded in Jan

EZ JAN IND PROD +0.8% M/M, +0.1% Y/Y; DEC -0.1% M/M

- EZ IP rebounded in Jan, rising 0.8% and coming in stronger than markets expected (BBG: 0.3%)

- Jan's uptick was driven by a recovery of capital goods production, up 1.1pp to 0.4%, and non-durable consumer goods output increasing by 1.5pp to 0.6%.

- Meanwhile, intermediate goods production and energy output decelerated markedly to 0.3% and 0.4%, respectively.

- Durable-consumer goods output eased as well by 0.1pp to 0.8% in Jan.

- Annual output shifted into positive territory, up 0.1% which is the first y/y increase since Oct 2018.

- Among the member states, Luxembourg (+3.8%), Greece and France (both +3.4%) showed the largest m/m gains, while Estonia and Latvia (both -1.5%) and Portugal (-1.3%) recorded the biggest declines.

GERMANY FEB FINAL HICP +0.6% M/M, +1.6% Y/Y; JAN +1.6% YY

MNI: SPAIN FEB FINAL HICP -0.6% M/M, -0.1% Y/Y; JAN +0.4% Y/Y

FIXED INCOME: Futures lower, curve steeper

Core fixed income futures are lower this morning while curves have steepened. Moves started around 6:10GMT/1:10ET this morning with little in the way of headline drivers and have continued through the European morning session.

- Gilt futures touched their lowest levels of the month this morning, while Treasury futures their lowest levels since Tuesday. Bund futures have erased all of the gains seen after the ECB announced yesterday but peripheral spreads remain tighter, so BTP futures remain above yesterday's pre-ECB levels.

- Looking ahead the highlights of the calendar are largely US PPI, Michigan confidence. With both the BoE and Fed in their blackout periods and the ECB having announced its policy decision yesterday, there is little expected to come from policymakers today.

- TY1 futures are down -0-19+ today at 132-00 with 10y UST yields up 6.4bp at 1.603% and 2y yields up 1.2bp at 0.154%.

- Bund futures are down -0.23 today at 171.41 with 10y Bund yields up 1.8bp at -0.317% and Schatz yields down -0.1bp at -0.697%.

- Gilt futures are down -0.46 today at 128.07 with 10y yields up 5.3bp at 0.786% and 2y yields up 0.6bp at 0.077%.

FOREX: Dollar Bouncing as Yields Roll Higher

- The greenback is erasing late Thursday weakness in relatively one-directional trade in G10 this morning. The USD is comfortably the best performer so far Friday, heading into the open higher by 0.5-0.7% against most others.

- The USD is following the US yield curve's march higher that began in late US trade and persisted throughout both Asia-Pacific and European hours. The Treasury curve is steeper, with 10y yields higher by close to 7bps and well above 1.60%. Moves follow the passage of Biden's $1.9trl stimulus bill late yesterday, with the fiscal expansion pressuring Treasuries and raising speculation that a swifter return to growth will bring sharper inflation pressure into the economic mix.

- USD strength has pressured EUR/USD back below the $1.19 level, with GBP/USD on track to test $1.39 in the near-term.

- Focus turns to US PPI & Uni of Michigan data as well as the Canadian jobs report for February.

EQUITIES: Tech Sharply Lower

- Asian stocks closed mixed, with Japan's NIKKEI up 506.19 pts or +1.73% at 29717.83 and the TOPIX up 26.14 pts or +1.36% at 1951.06. China's SHANGHAI closed up 16.247 pts or +0.47% at 3453.078 and the HANG SENG ended 645.89 pts lower or -2.2% at 28739.72.

- European stocks are lower, with the German Dax down 99.16 pts or -0.68% at 14349.69, FTSE 100 down 17.44 pts or -0.26% at 6712.62, CAC 40 down 9.39 pts or -0.16% at 5895.36 and Euro Stoxx 50 down 25.36 pts or -0.66% at 3763.32.

- U.S. futures are lower, led by the NASDAQ: the Dow Jones mini down 36 pts or -0.11% at 32443, S&P 500 mini down 25.5 pts or -0.65% at 3911.25, NASDAQ mini down 246 pts or -1.89% at 12802.25.

COMMODITIES: Precious Metals Retreat As Dollar Gains

- WTI Crude down $0.13 or -0.2% at $65.66

- Natural Gas down $0.02 or -0.9% at $2.637

- Gold spot down $21.16 or -1.23% at $1699.22

- Copper down $5.45 or -1.32% at $407.75

- Silver down $0.6 or -2.3% at $25.6807

- Platinum down $23.91 or -1.99% at $1181

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.