Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

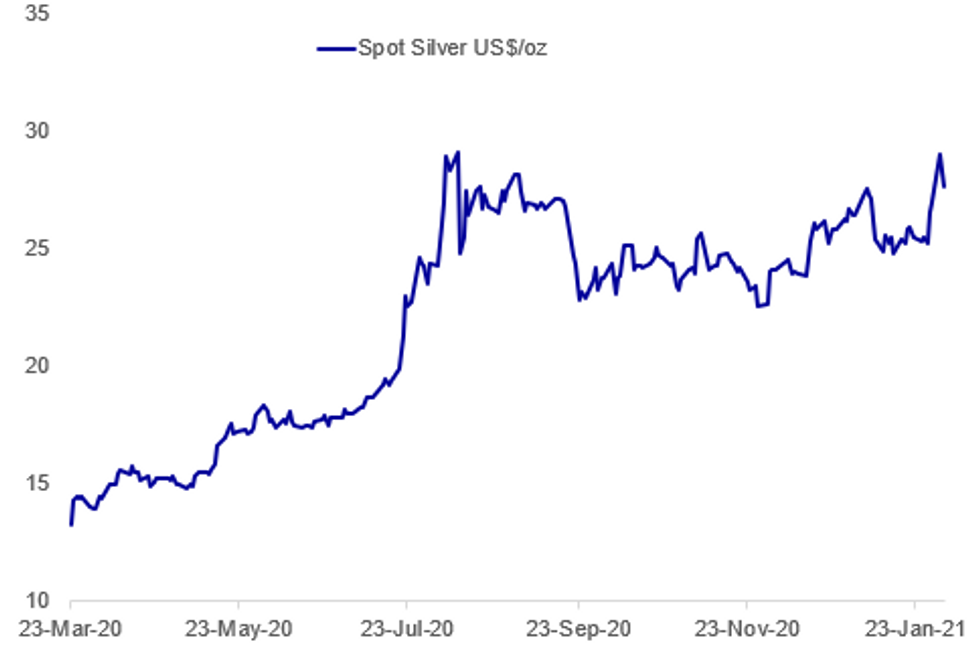

- SILVER, GAMESTOP SINK AS INVESTOR FRENZY SHOWS SIGNS OF COOLING

- ITALIAN AND EUROZONE GDP LOWER IN Q4 AS LOCKDOWNS BITE

- R.B.A. EXPANDS Q.E. BUT UPGRADES EMPLOYMENT VIEW (MNI STATE OF PLAY)

Fig. 1: Silver Takes A Breather

BBG, MNI

BBG, MNI

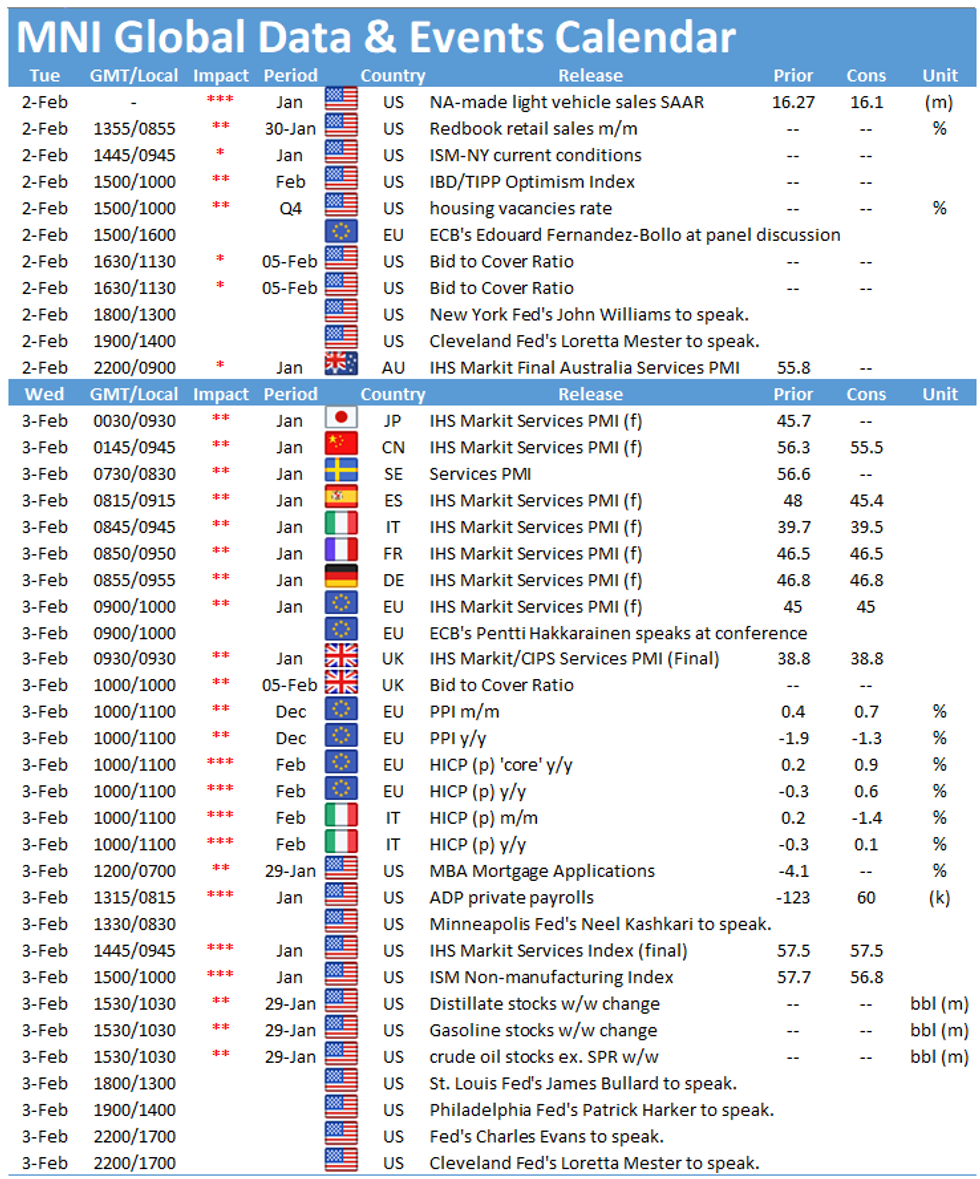

NEWS:

MARKETS (BBG): The investor frenzy that stoked wild gains in everything from GameStop Corp. to silver is showing signs of fatigue. The metal dropped more than 5% on the Comex Tuesday, sinking from an eight-year high after margin requirements were raised and analysts cautioned against chasing the rally. GameStop, whose Reddit-inspired surge set off a flurry of buying in other heavily shorted stocks, sank 16% in after-hours U.S. trading on Monday, extending a 31% plunge during the regular session. Other high-flyers including AMC Entertainment Holdings Inc. and Koss Corp. also slumped in late New York trading. Some of last week's biggest gainers in Asia, including China Literature Ltd., lagged behind benchmark indexes on Tuesday.

RBA: The Reserve Bank of Australia expanded its quantitative easing program by AUD100 billion despite upgrading its labour market forecast and said it will maintain current record low interest rates "until 2024 at the earliest." Although the recovery was "well under way and has been stronger than was earlier expected," the economy needed ongoing support, the RBA said as it left its cash rate unchanged at 0.10% on Tuesday. While the rate decision was widely expected, the move to double the size of its QE program announced last year came as a surprise. The first AUD100- billion QE program, set to end in mid-April, will now be extended with the central bank continuing to purchase AUD5 billion in longer dated Commonwealth and state government debt each week.

RIKSBANK (BBG): Sweden's Riksbank Governor Stefan Ingves says high level of household indebtedness makes the economy "very vulnerable" and reducing this vulnerability requires a "more extensive review of taxation and housing policy, rather than patching over when problems arise."

SNB (BBG): Swiss National Bank President Thomas Jordan says outlook for the economy remains uncertain amid the pandemic and gross domestic product won't reach its pre-crisis level until 2022, according to comments at a Le Temps conference in Lausanne. With inflation low, fiscal and monetary policy must stay expansionary

U.K. DATA (BBG): U.K. house prices fell last month for the first time since June as a temporary cut in the tax on purchases approached its expiration date.Values fell 0.3% from a month earlier to an average of 229,748 pounds ($314,000), Nationwide Building Society said Tuesday. They climbed 6.4% from a year earlier, slowing from 7.3% in December.

DATA:

EZ GDP Declines in Q4 As Second Covid Wave Hits

EZ Q4 PRELIM. FLASH GDP -0.7% Q/Q SA, -5.1% Y/Y WDA

EZ Q3 GDP +12.4% Q/Q SA; -4.3% Y/Y WDA

- The EZ economy narrowed in Q4 as the second wave of Covid-19 hit Europe, down 0.7%, beating market expectations (BBG: -1.2% q/q)

- This follows a historic increase in Q3 where the economy grew by 12.4%.

- Annual GDP deteriorated in Q4 to -5.1%, down from -4.3% seen in the previous quarter.

- Over the year of 2020, GDP fell by 6.8% in the eurozone and was down 6.4% in the EU.

- Among the member states for which data is available, Austria (-4.3%), Italy (-2.0%) and France (-1.3%) saw the largest quarterly decrease, while Lithuania (+1.2%) and Latvia (+1.1%) recorded the highest gains.

- The annual growth rate was negative in all countries with the highest level seen in Spain (-9.1%).

Italian GDP Lower In Q4 As Lockdowns Bite

- Preliminary 4Q20 GDP -2.0% q/q, -6.6% y/y, coming slightly better than markets expected (BBG: -2.2% q/q)

- 3Q20 GDP real SA WDA revised down +16.0% q/q; -5.1% y/y

- 4Q20 q/q industry, agriculture, services all down--ISTAT

- ITALY: 2020 average WDA GDP -8.9% y/y on preliminary data--ISTAT

- Italy prelim GDP -8.2% 'acquired' net growth for 2021--ISTAT

FIXED INCOME: Bear steepening on trend

A steady session for Core Bonds, with curves bear steeper this morning

- Bund has taken its cue from the better buying going through in Equities in early trading.

- Good vaccination pick up pace in the US as well as a more positive note on US stimulus has keep the lid on Bonds.

- Heavy supplies this week will also be a factor, with a huge heavy day on Thursday, when France look to sell EU10bn-EU11bn of 0% Nov-30 OAT, the 1.25% May-36 OAT, the 1.75% Jun-39 OAT and the 0.75% May-52 OAT

- Today sees German EU6bn Schatz 2yr (equates to 61k Schatz or 8k Bund).

- Also some syndication from Belgium, Finland and Cyprus.

- Peripheral are tighter, with Greece leading at 2.5bps.

- Gilts have traded in tandem with EGBs, and leading losses in Europe, down 40 ticks at the time of typing.

- Same story for the US treasuries, curve is bear steeper on the risk on tone, with the longer end underperforming

- Looking ahead, desk await news on the formation of a new Italian government, with PM Conte set to speak to Pres Mattarella again today.

- ECB's de Cos is also speaking.

FOREX: EUR/USD Touches New 2021 Lows

The single currency is extending recent losses, with the EUR again among the poorest performers in G10. EURUSD accelerated losses on the break through Monday's low to hit lowest levels of the year and lowest since early December. This has opened support at the Sep 1 low and former breakout level at 1.2011. Below here, the 100-dma undercuts as support at 1.1962.

CAD is the best performer in G10, with NOK not far behind as WTI and Brent crude futures post decent gains. Oil trades with gains of over 2% as USD weakness buoys commodities, helping crude futures chew through near-term resistance.

Data has been few and far between this morning, although Eurozone GDP for Q4 came in ahead of expectations, but still showed sharp contraction of 5.1% over the year.

There are no tier one data releases crossing later today, keeping focus on the speaker slate. This includes ECB's de Cos, Fed's Kaplan and Mester. US earnings could draw some focus, with Pfizer, ExxonMobil, Alphabet and Amazon all due today.

EQUITIES: Rebound Continues

Equities globally are higher, with big US earnings anticipated today (Amazon, Alphabet, UPS, Pfizer among them).

- Asian equity markets closed higher, with Japan's NIKKEI up 271.12 pts or +0.97% at 28362.17 and the TOPIX up 17.18 pts or +0.94% at 1847.02. China's SHANGHAI closed up 28.401 pts or +0.81% at 3533.685 and the HANG SENG ended 355.84 pts higher or +1.23% at 29248.7.

- European stocks are stronger, with the German Dax up 185.59 pts or +1.36% at 13722.03, FTSE 100 up 55.96 pts or +0.87% at 6466.42, CAC 40 up 108.55 pts or +1.99% at 5461.68 and Euro Stoxx 50 up 59.66 pts or +1.69% at 3563.4.

- U.S. futures are higher (led by tech), with the Dow Jones mini up 260 pts or +0.86% at 30370, S&P 500 mini up 34.5 pts or +0.92% at 3800.25, NASDAQ mini up 129.5 pts or +0.98% at 13366.

COMMODITIES: Silver Speculation Unwinds

- WTI Crude up $0.85 or +1.59% at $54.41

- Natural Gas up $0.12 or +4.35% at $2.971

- Gold spot down $8.05 or -0.43% at $1847.23

- Copper down $2.45 or -0.69% at $352.25

- Silver down $1.31 or -4.5% at $27.7472

- Platinum down $23.47 or -2.07% at $1109.11

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.