Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

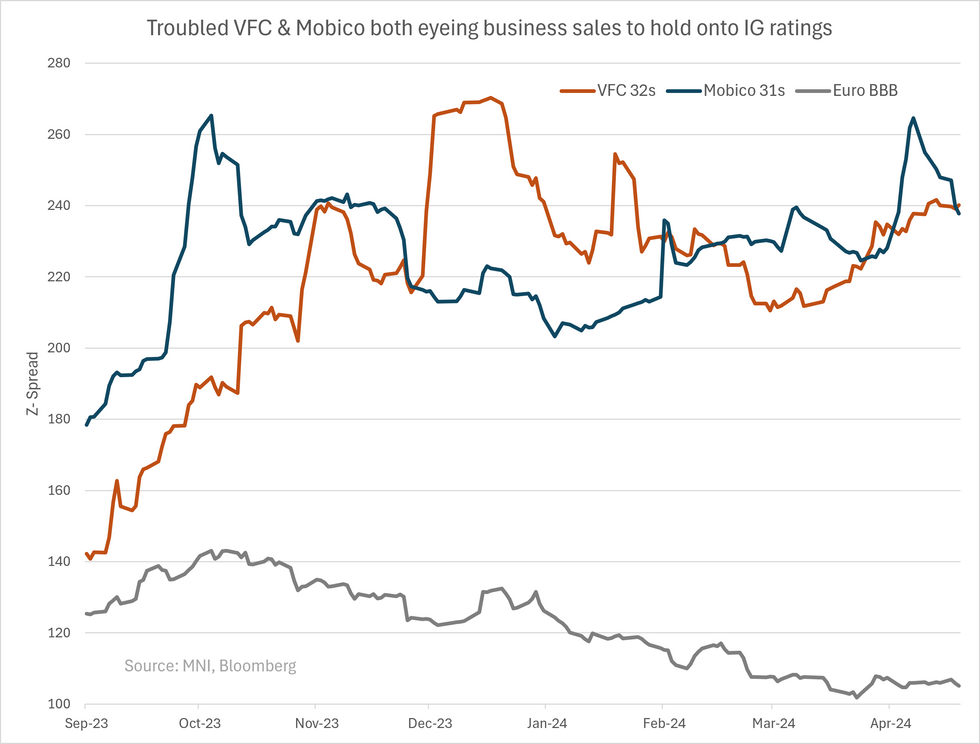

Mobico (branded as National Express on long-haul coach services) is facing crossover rating risk after a Moody's downgrade last night (which it based on FY23 results). 1Q results were directionally positive; revenues at £802m up net +3.5% and 6.7% in cc terms but it still left FY24 EBIT guidance unch at £185-205m - latter leaves the downgrade into HY likely. North America school bus business (23% of revenues, lower margin) tabled for sale could put-off a downgrade - timing & use of proceeds remains uncertain & would increase exposure to ALSA business (mostly Spain, already 80% of EBIT).

The €500m 31s trade well wide already at G+273/Z+237/€98, no firm view on the co yet but fallen angel Elo & troubled IG VFC offer equal to higher carry on shorter lines & may see a recovery before Mobico does (we have no view on either till that happens). We don't expect Mobico supply till earliest Nov '25 (first call on £ perp). FY23 results below.

- Revenue at £3.2b, EBITDA £386m (12% margin) & operating cash flows at £252m. Reported EBIT was £169m (5.4% margin) while statutory was -£21m on impairments on contracts from Covid (-£113m), onerous contract provisions in Germain rail (-£100m) & restructuring costs (-£30m).

- On BS covenant gearing was at 3x (from 2.8x previous year, limit in covenants is 3.5x). Net debt was £1.2b, covenant net debt (used on quoted leverage) at £1b. It pushed out reaching target of 1.5x-2x from '24 to '27 on expected poor operating performance/EBITDA. FY24 EBIT guidance is for £185-205m.

- To alleviate pressure on BS it announced in Oct '23 the North America School bus business would be sold - in 1Q results in April it said it was "progressing well".

- Liquidity not a issue with £300m in cash & £600m in undrawn revolver. No near-term risk on the £500m perps (now Ba2 rated) loosing 50% equity treatment - first call is Nov 2025. Near term maturities (next 3yrs) are negligible outside the perp (small bank loans & leases totalling <£100m).

Background on co; most revenues from long-haul, shuttle & charter/private hire bus services in UK, Europe & NA (70%) with remainder from NA school bus services (23%) & German rail (8%). Moody's says ~70% of revenues are contracted & concession based which shields it somewhat from passenger demand fluctuations (but as above exposes it to contract renewal risk).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.