Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER CYCLICALS

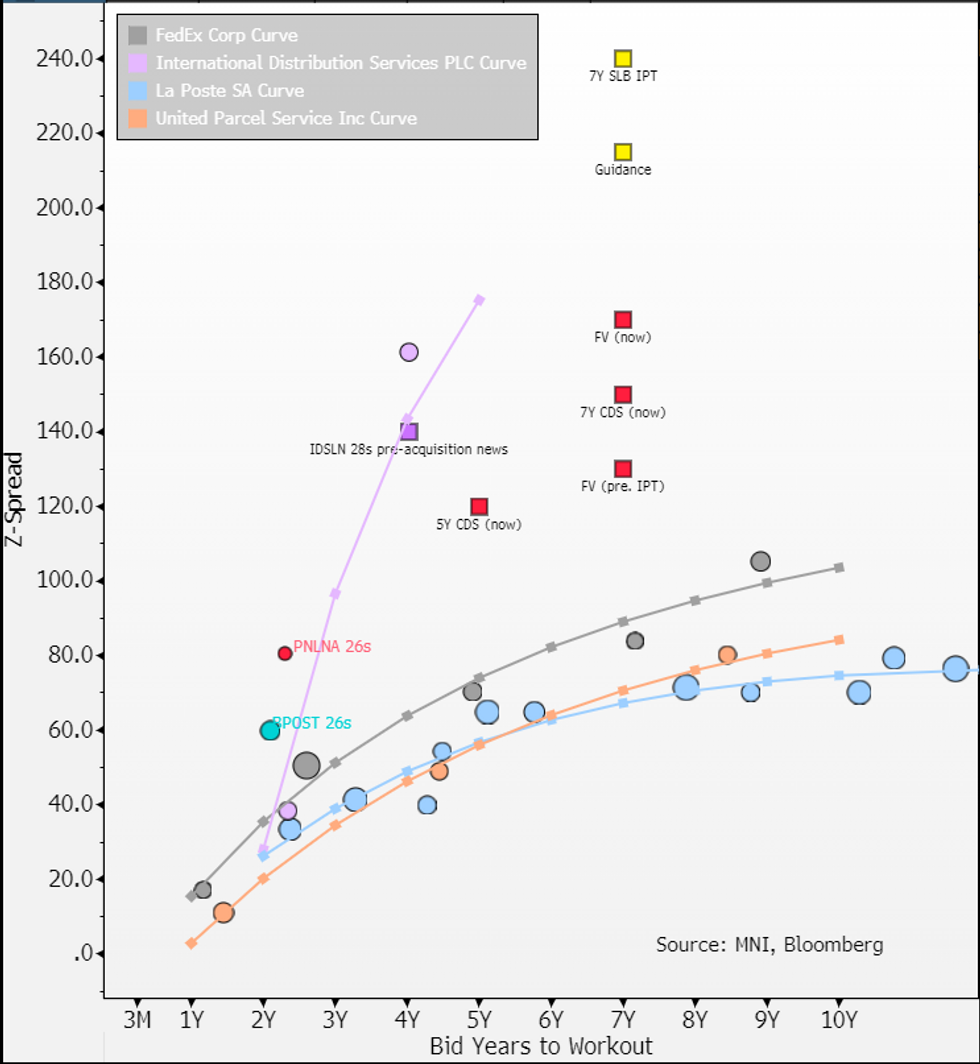

€300M 7Y SLB +215a vs. FV +170 (revised from +130), cheap view added.

- 25 in from IPT, books >€1.5b is healthy for size.

- All our thoughts are linked below. As we've said previously timing is the biggest issue for us; FY/CY24 guidance is for a firm recovery but we are still uncertain if it that will play out noting EBIT is seasonally back-loaded into Q4.

- 7Y CDS mids around +155 gives -60bps basis on guidance; attractive levels particularly for IG name.

- We said investors should eye this for value on anything above 200. In line with that we now add a cheap view on the deal. It is not on any expectation that the NIC will be being traded away in secondary but on carry & (hopeful) roll-down into 5Y CDS levels at ~120.

- We keep our cheap view as well on IDSLN28s that have held surprisingly well (-1 today) - of the two we prefer IDSLN28s.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok