Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

MNI (London)

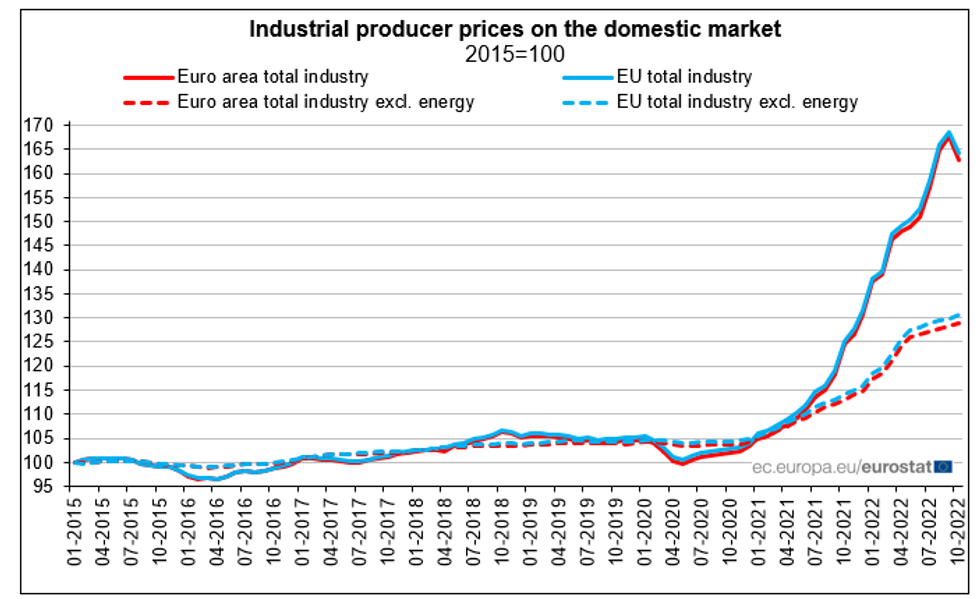

EUROZONE OCT PPI -2.9% M/M (FCST -2.0%); SEP +1.6% M/M

EUROZONE OCT PPI +30.8% Y/Y (FCST 31.7%); SEP +41.9% Y/Y

- Factory-gate inflation cooled more than anticipated in the October data, contracting by -3.9% m/m in a significant turn-around from +1.6% m/m recorded in September.

- The annualised PPI rate slowed by over 11pp to +30.8% y/y, distancing further from the August peak.

- Falling energy-sector prices drove the decline, down -6.9% m/m alone.

- Yet the October print should be taken with only cautious optimism. Core PPI showed no relief; ex-energy PPI was up +0.5% m/m.

- Volatile Irish data will have also skewed the print to the downside, implying that factory-gate inflation was less improved than the headline figure suggests. However, the fall in energy prices is a step in the right direction, and signals an imrpovement in outlooks for the energy-intensive industrial sector.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok