Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

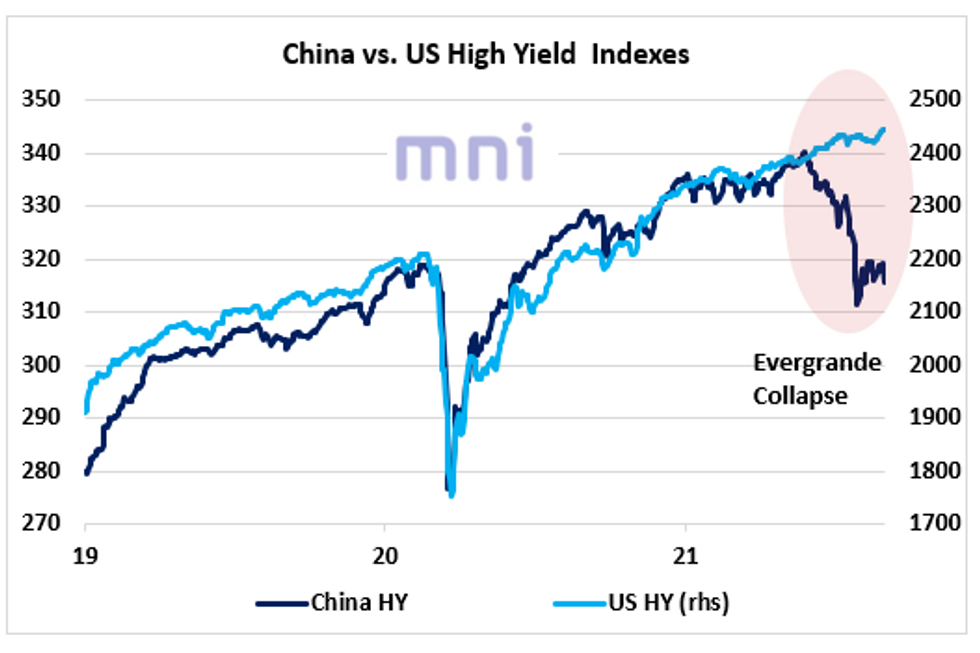

- Selling pressure has been growing in the Chinese credit market as Evergrande contagion fears returns.

- The company has been trying to sell its assets to meet its short-term obligations, but the default risk has been surging with the June 2025 bond currently trading below 30 cents on the dollar.

- Evergrande mentioned this week that its total liabilities rose to a record 1.97tr CNY, the world's most indebted real estate developer.

- With the share price falling to HKD 4, its lowest level since June 2015, its price-to-book ratio has collapsed to 0.23 (from a high of 4.5 in 2017), weighing on the entire real estate sector.

- Interestingly, the fall in Chinese high yield bond market has not been weighing on Western HY bond indexes.

- The chart below shows the significant divergence between Markit iBoxx China High Yield Index, which has been plunging in the past few weeks, and the Bloomberg Barclays US Corporate HY bond index (which continues to reach new highs).

- Markit iBoxx China High Yield Index reflects the performance of a subset of USD denominated bonds issued by entities domiciled specifically in China.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok