Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

RUSSIA

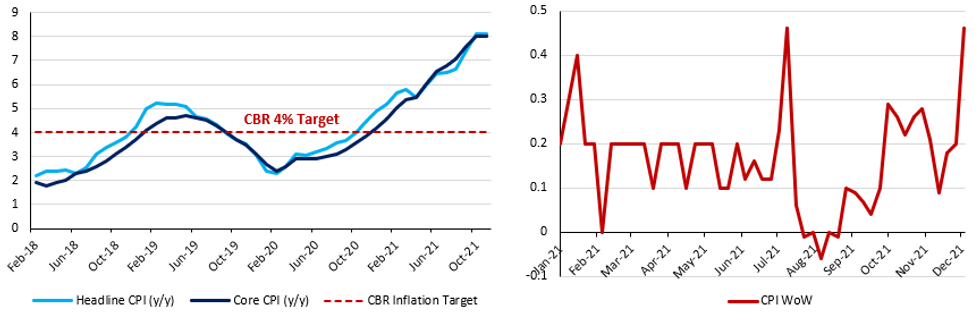

- Today’s CPI print will be monitored closely ahead of next Friday’s CBR meeting with analysts split over the size of the bank’s next potential hike. The range of expectations is currently +50-100bp, with most leaning towards the 75-100bp range.

- Headline CPI is expected to print in the 8.3-8.4% y/y range (bbg 8.35%), driven by non-core factors as the earlier shock from fruit and vegetable prices seems to have eased.

- The higher print is mostly a function of a weaker RU, higher retail prices of some imported goods (delays of supplies going through EU-Belarus borders), and traditional price increases ahead of the New Year holidays.

- Prices are expected to peak in December, however, with more favourable base effects, along with a firmer RUB, filtering through into the final reading for the year.

- Weekly inflation prints suggest headline momentum is slowing, but price pressures have broadened across the basket - which may prompt the CBR to target the upper end of the hiking range (+75-100bp) in keeping with its push to re-anchor inflation expectations.

MNI London Bureau | +44 020-3983-7894 | murray.nichol@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok