Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

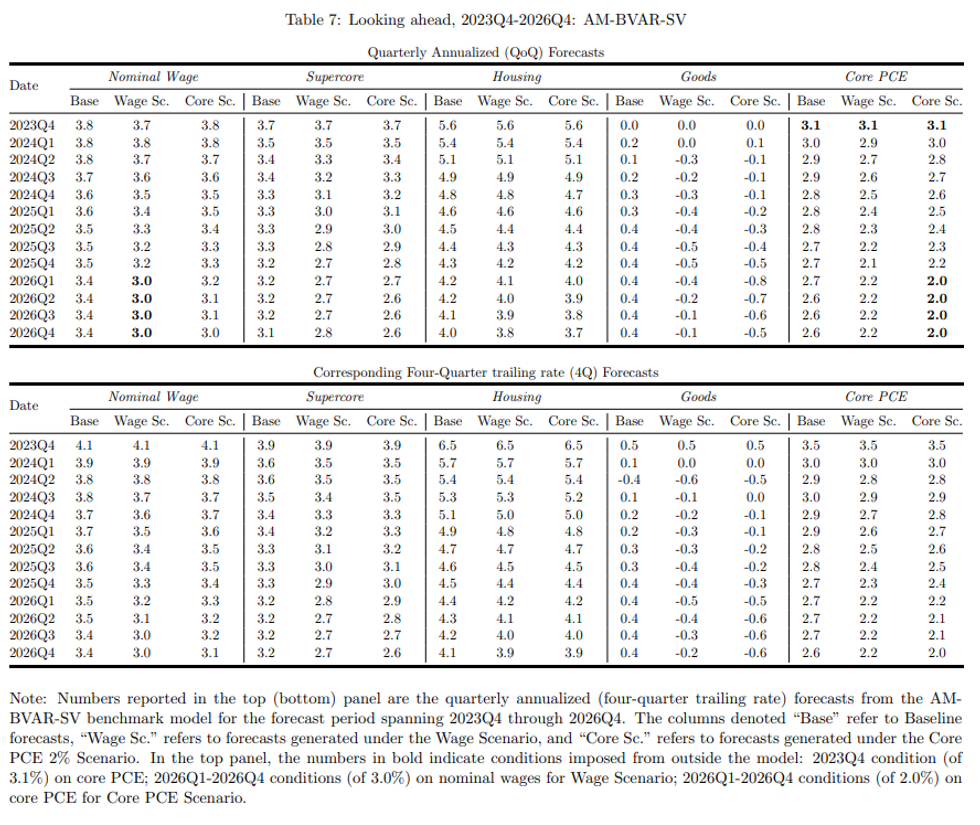

- Cleveland Fed staff economists (research here) have mapped out a baseline scenario which has core PCE inflation, after stepping down from 3.5% Y/Y in 4Q23 to 3.0% in 1Q24, then see limited further disinflationary progress to 2.9% Y/Y in 4Q24, 2.7% Y/Y in 4Q25 and 2.6% in 4Q26. (That compares with the FOMC median of 2.4, 2.2 and 2.0 for Q4/Q4 rates in 2024, 2025, and 2026).

- In this model, “supercore” inflation would still be running at 3.1% out in 4Q26, with housing at 4% and goods at 0.4%.

- Alternatively, if nominal wage growth settles at an annualized rate of 3.2% in 2025 and 3.0% in 2026 (rather than 3.5% and 3.4% in the baseline), it would help see core PCE inflation slow to 2.2%. Wage growth was estimated at 3.8% for 4Q23.

- Other findings: “Our historical results also indicate that aggregate inflation is best forecast directly; no consistent benefit can be achieved by aggregating disaggregate components.”

- “It is most likely the case that a return of core inflation to the Federal Reserve’s 2 percent target will be associated with all three components returning to near pre-pandemic levels.”

Source: Cleveland Fed

Source: Cleveland Fed

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok