Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER CYCLICALS

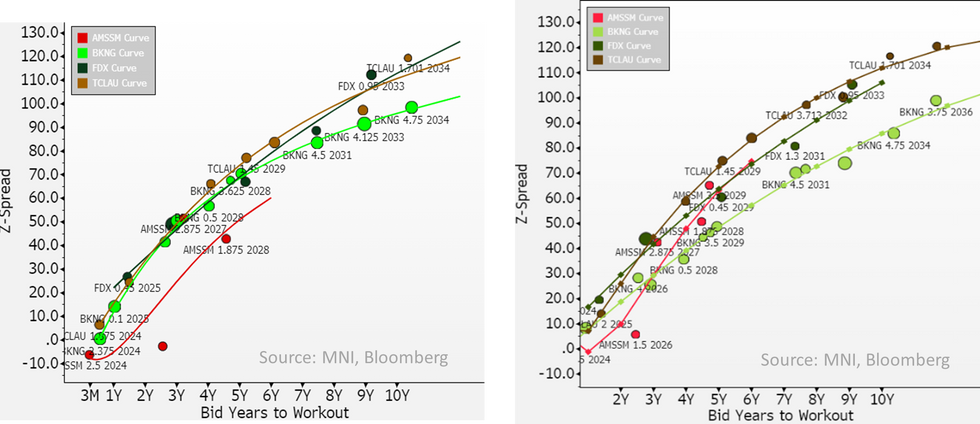

Curve screens fair to us now after a ~20bp rally over the last month (including against close comp's). Next event of interest for us is 1Q24 earnings in early May - we are keen to hear mgmt's take on any impact from Italian regulators' & any updates on Spain regulator draft fine. Cash lines strong 2-5bps tighter today.

- BKNG has always screened wide to us - not a new phenomena for it but we are starting to see some signs of that finally reversing.

- It came to primary in late Feb, we liked the name then but markets didn't take it well - secondary selling off +7-11bp on €2.7b/4-part deal. It was then trading well wide of 2-notch lower close comp Amadeus (Baa2, BBB) & in-line with FedEx and Transurban (which we included solely to highlight the size of the reverse yankee discount). Its since moved firmly tighter to all 3 - before and after below.

- As we've highlighted there is some overhanging uncertainty on the draft Spain regulator (CNMC) fine for ~$530m which it said it would appeal & any fines on recently launched investigation from Italian competition watchdog (AGCM) - fines unlikely to impact BS ($13b cash on hand & $7b/yr in FCF) but changes to business practices could. Company reports 1Q24 results on 2nd of May - we expect it to comment on Italian investigation then.

- Curve screens fair to us now and as we've mentioned before we see better opp's in certain tenors; on the 34's the equal rated & short-tenor Wesfarmers/WESAU 33's that only gives away -2bps screens cheaper (likely on single Aussie issuer discount) - it does seem to trade - & on the newly issued 44's, ABIBB 44's are only -4bps inside/screening more value.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok