Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FRANCE

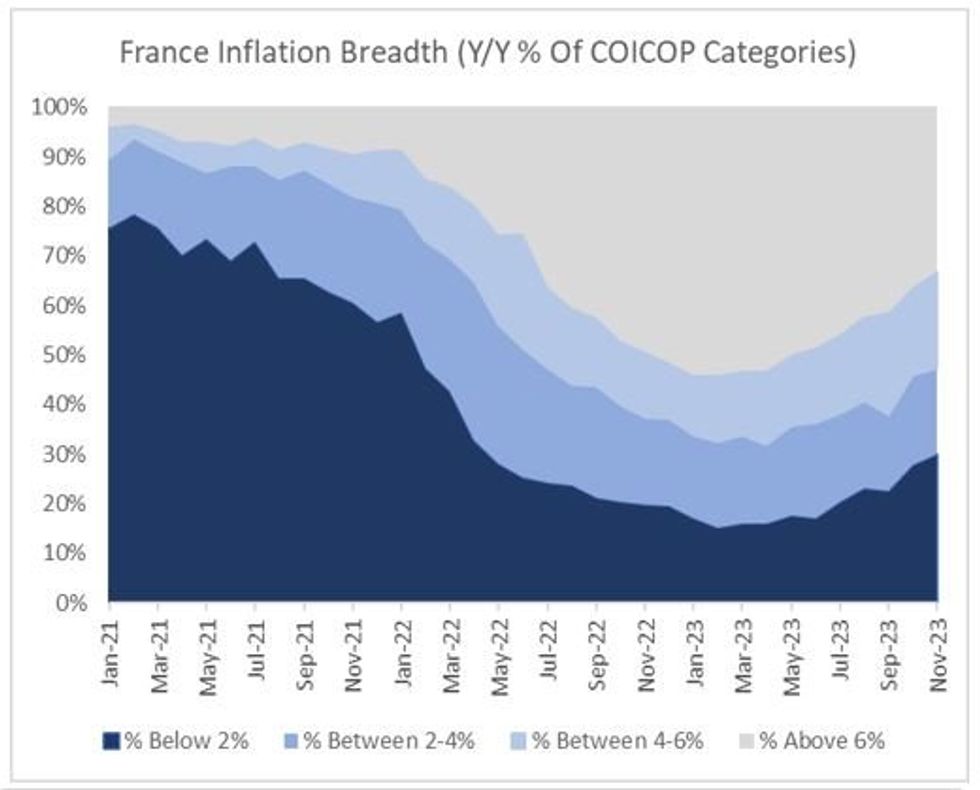

France (20% of EZ HICP) – 0745UK Thu 4 January

- Consensus expectations:

- HICP: 4.1% Y/Y (3.9% prior) / 0.3% M/M (-0.2% prior)

- CPI: 3.7% Y/Y (3.5% prior) / 0.2% M/M (-0.2% prior)

- November inflation printed below consensus, with core and headline prices moderating.

- Services inflation moderated to 2.7% Y/Y (vs 3.2% prior) while non-energy industrial goods prices rose 1.9% Y/Y (vs 2.2% prior). Monthly rises in unprocessed foods meant that the disinflation in overall food prices was smaller than other components (7.6% Y/Y vs 7.8% prior).

- This month, the headline rate is expected to pick up due to energy base effects, while travel-related services may push up services and core components.

- The November flash PMI noted softening inflationary pressures overall, but wage costs continued to drive up input costs amongst service sector firms.

- Barclays and Goldman Sachs see Y/Y HICP printing 4.1%; Nomura 4.2%.

Source: INSEE, MNI Calculations

Source: INSEE, MNI Calculations

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok