Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

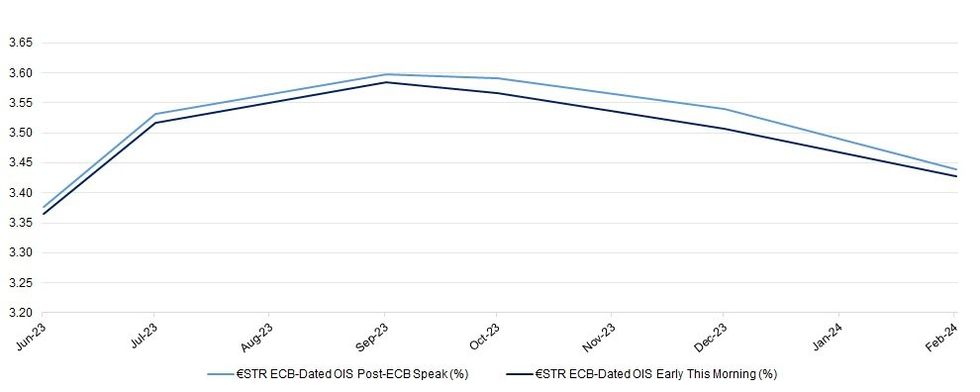

Hawkish rhetoric from the ECB, including that from Lane late yesterday (noting there is still “a lot of momentum” in inflation, albeit with a hat tip to the disinflation expected later in ’23), as well as the usually hawkish Kazimir (highlighting plenty of ground left to cover, while noting that the battle against inflation is far from won & the ability to hike for longer given its downshift to 25bp hiking increments) & Kazaks (noting quite some ground left to cover, while stressing that the risk of doing too little dominates, pushing back against market pricing of rate cuts in early ’24) has biased ECB-dated OIS 1-3bp higher today, although the market remains reluctant to fully price in 2 further 25bprate hikes. Comments from Schnabel, Villeroy, Vujcic & Vasle are still due to cross through the remainder of the day.

| ECB Meeting | €STR ECB-Dated OIS Post-ECB Speak (%) | €STR ECB-Dated OIS Early This Morning (%) |

| Jun-23 | 3.377 | 3.365 |

| Jul-23 | 3.532 | 3.517 |

| Sep-23 | 3.597 | 3.585 |

| Oct-23 | 3.591 | 3.567 |

| Dec-23 | 3.54 | 3.507 |

| Feb-24 | 3.439 | 3.427 |

source: MNI - Market News/Bloomberg

source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.