Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

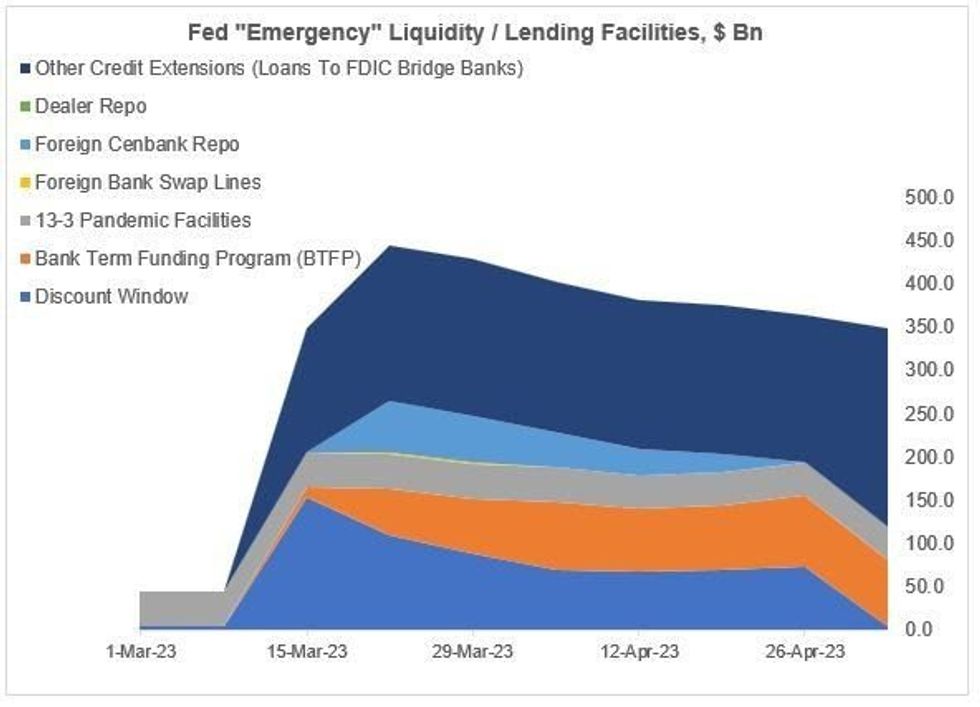

From our Fed Balance Sheet Tracker (full PDF here): Bank usage of Fed liquidity facilities continues to fade from March’s peak, with the latest weekly data to May 3 showing a pullback in key Fed asset categories including the discount window. Indeed this was the 6th consecutive week of declines.

- The Bank Term Funding Program saw takeup fall by $5.5B last week to $75.8B, and this is now down from the $81.3B peak. That's in spite of some expectations upon its announced launch that the BTFP could expand considerably, into the trillions of dollars. And discount window borrowing dropped by $68.5B, with the amount outstanding now down to just $5.3B.

- "Other credit extensions" - which is the line item for Fed lending to FDIC bridge bank entities for resolution purposes - saw a $57.8B jump to a new high of $228.2B. But that was to be expected given the First Republic Bank resolution the previous weekend (which follows SVB and Signature), and “other credit extensions” will eventually be wound down.

- The fall in discount window borrowing and the rise in other credit extensions is related – First Republic was a major borrower from the discount window (it had borrowed $63.5B), and so this borrowing basically shifted from one category to another. First Republic had also borrowed $13.8B via the BTFP. “Other credit extensions” is now the bulk of recent "emergency" lending, which currently totals $310B (when excluding the Pandemic 13-3 Programs).

- With FIMA foreign central bank repo takeup having previously dropped to zero from as much as $60B in March, foreign dollar swap line usage minimal (and moved back to a weekly schedule vs daily during most of March), there isn't much sign of financial system duress from the perspective of the Fed's assets ledger.

- That could change in coming weeks given that regional bank share prices remain volatile, which could portend a renewed bout of weakness underneath the surface.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok