Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CZECHIA

MNI (London)

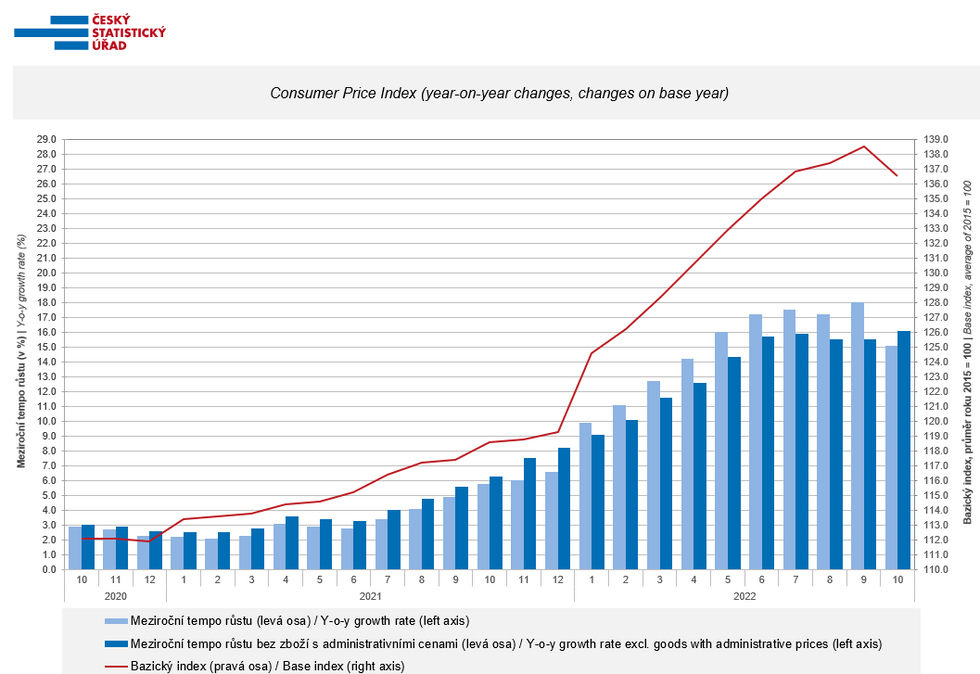

CZECH OCT CPI -1.4% M/M (FCST +0.9%); SEP +0.8% M/M

CZECH OCT CPI +15.1% Y/Y (FCST +17.9%); SEP +18.0% Y/Y

- Czech CPI decelerated in October as prices contracted by -1.4% m/m and annualised inflation slowed by 2.9pp to +15.1% y/y. This is a marked deviation from consensus expectations of +0.9% m/m and +17.9% y/y.

- On the month, food prices and transport fuels accelerated sharply (+3.0% m/m and +4.9% m/m).

- State household support for energy costs largely underpinned the decrease in price pressures. Electricity prices fell by 38.2% y/y in October as a result, in stark contrast to +37.8% in September.

- This translated into a lower total goods inflation of +16.0% y/y, down from 20.7% y/y in September.

- Core CPI saw some relief in October. CPI ex. domestic heating and lighting oils, automotive fuel slowed to +14.8% y/y from +17.9% in September, implying that the deceleration in goods prices is applying additional downward pressure to the headline print.

- The lower-than-expected print will view of the majority that already-instituted tightening will be sufficient to contain prices going forward, leaving Holub and Mora as the only outstanding hawks on the board. The next CNB decision is due December 21st.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok