Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR FUTURES

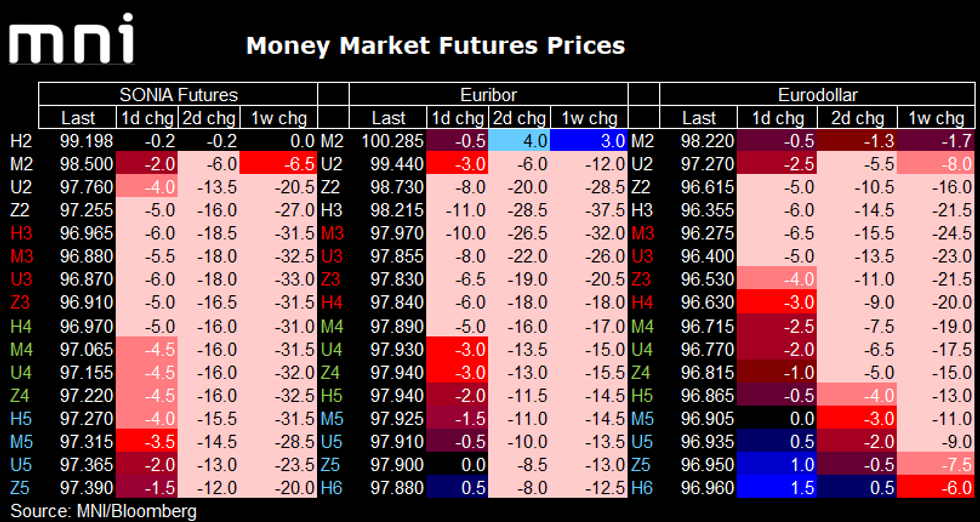

Ahead of the release of US CPI (the day's main event) STIR markets have continued to march lower as the US starts to get into the office.

- Euribor futures have seen the biggest moves of the day with the Dec-22 contract 11 ticks lower on the day (and now 28.5 ticks lower than Wednesday's close). The rest of the Euribor strip has pivoted around this, steepening in the front-end but flattening thereafter but all Whites, Red and Green contracts are lower on the day. Markets are now pricing 36bp for the July ECB meeting and 76bp cumulatively by September with 150bp priced by year-end (in 4 meetings) and 209bp priced by March 2023 (6 meetings).

- A recalibration of ECB hike probabilities has also seen SONIA futures dragged lower with Reds up to 6 ticks lower. Markets continue to price around 29bp for next week's meeting and then 70bp cumulatively by August and 165bp by year-end (5 meetings). The curve then flattens a bit but there is still 200bp priced in by March 2023.

- Eurodollar futures are also lower going into CPI with Whites/Reds generally down 3-6 ticks on the day. 52bp is priced for next week, 105bp (cumulatively) by July, 149bp by September (3 meetings) and 211bp by year-end.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok