Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US OUTLOOK/OPINION

Wherever core prices go next, the May CPI report made at least one thing clear: inflation hadn't peaked in March/April as many had expected. Whether core prices have scope to accelerate further or not, the Fed has an uncomfortable task when it meets next week.

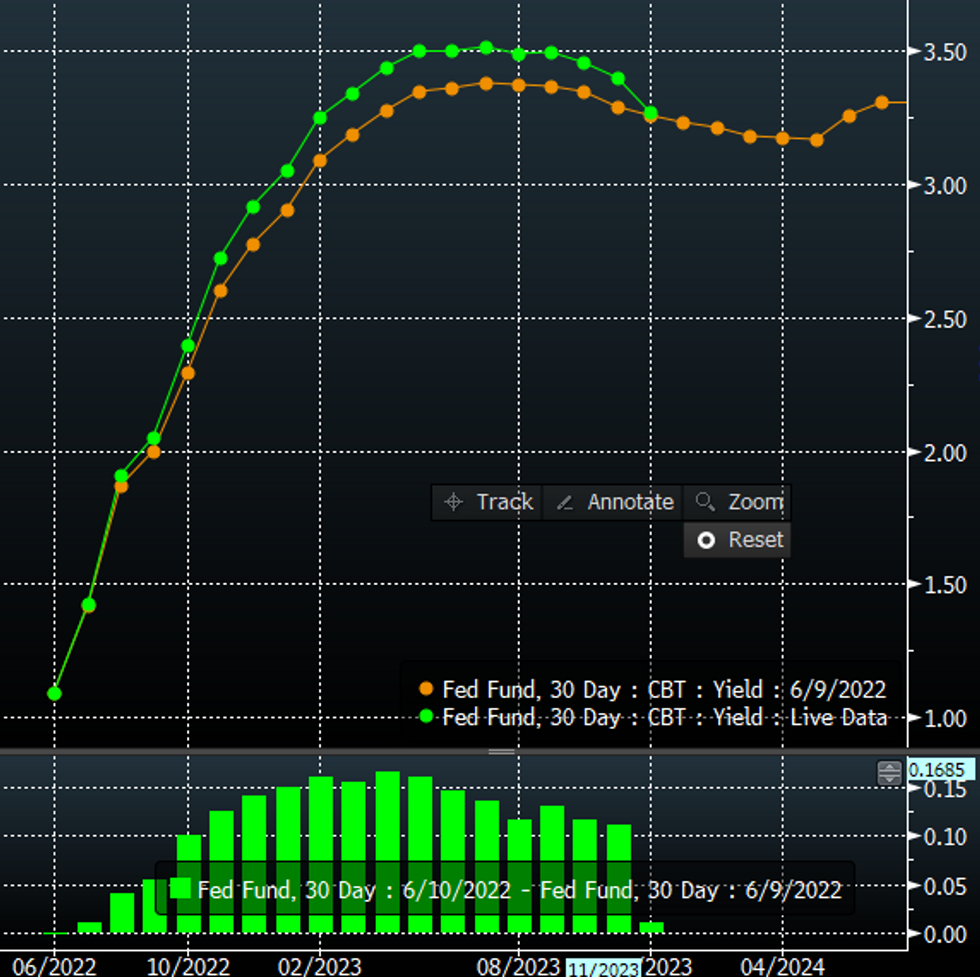

- Fed funds futures are implying a new peak rate of 3.5% in Q3/Q4 2023 (see chart) but real yields are flat on the day and negative out 5 years as implied breakevens rise - there will be questions next week to Powell of whether the Fed will have to run faster just to stand still (and also helps explain why the curve is increasingly implying recession fears).

- Inflation fund manager Michael Ashton (@inflation_guy on Twitter) estimates that median CPI came in at +0.63% M/M, which would be the highest since 1982. He also wryly observes: "good news is that alcoholic beverages inflation is only +4.04% y/y. We're gonna need it."

Fed Funds Futures Implied Rates, Yesterday vs TodaySource: BBG, MNI

Fed Funds Futures Implied Rates, Yesterday vs TodaySource: BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok