Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

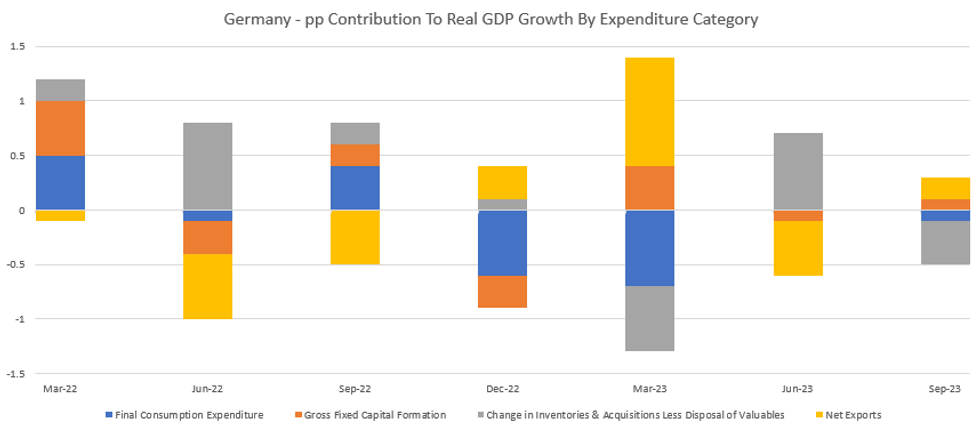

German Final Q3 GDP was unrevised as expected at a seasonally adjusted -0.1% Q/Q (+0.1% Q2), and -0.8% Y/Y (-0.4% prior). The final release includes a breakdown of GDP components that is unavailable in the initial print, and it showed that private consumption and inventories were the most significant drags in the quarter, as household savings remained elevated.

- Inventories subtracted 0.4pp from the quarterly growth figure, partially reversing from a 0.7pp positive contribution in the previous quarter. Private consumption fell, subtracting 0.1pp from GDP, partially offset by a 0.1pp contribution from government expenditure which saw an incline (+0.2% Q/Q) after 4 contractionary quarters.

- Fixed investment also saw a small jump (especially equipment at +1.1% Q/Q), though residential investment remained a weak spot, with dwellings construction negative for the 5th quarter in 6.

- Net exports contributed 0.2pp to growth, but that was driven by imports decreasing (-1.3%) even more strongly than exports (-0.8%), confirming weak domestic demand seen in other economic indicators including PMIs and the trade balance.

- On a sectoral basis (seasonally adjusted gross value added +0.1 Q/Q), industrial economic activity excluding construction decreased clearly (-0.9% Q/Q), driven by a weaker automobile industry. The services sector remained resilient.

- The savings rate was higher than last year at 10.3% (NSA, +0.7 pp Y/Y) as available private household income rose more ( +4.7% Y/Y nominal) than private consumption (+3.8% Y/Y), potentially indicating a weak economic outlook of private households.

- Survey data including PMIs and IFO provide a basis for a slightly more optimistic outlook for the coming months but the recent fiscal turmoil following the constitutional court ruling will potentially see government expenditure restrained, weighing on investment, and deteriorate private confidence, weakening domestic demand.

Source: Destatis, BBG, MNI

Source: Destatis, BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok