Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

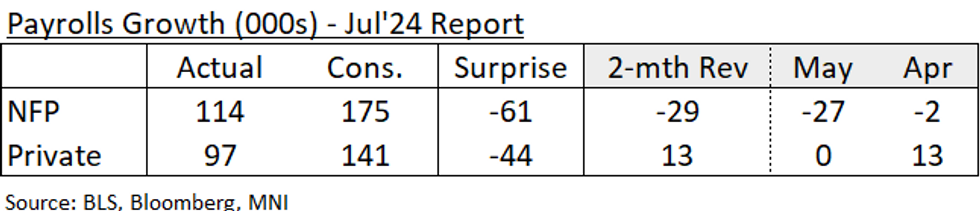

The July employment report was much weaker than had been expected in almost every respect, and with only a few mitigating factors based on a closer look at the underlying numbers.

- The 114k of payroll gains was 61k below the median expectation, and was effectively a 90k "miss" with the 2-month downward revisions to May (-27k) and April (-2k).

- Private payrolls missed badly, at +97k (141k consensus), though enjoyed a 13k upward revision (accounted for entirely by April).

- The rise in the unemployment rate from 4.1% 4.3% was due in part to a rounding effect (unrounded was 4.25%), but this still represented a 0.2pp increase in the rate (4.05% unrounded prior, unrevised).

- While headline payrolls and unemployment were worse than foreseen by any primary dealer in MNI's preview, earnings also came in at the low end of expectations at an unrounded 0.229% M/M (down from a downwardly revised 0.287%).

- A downside surprise to job gains had been flagged as a major risk on account of Hurricane Beryl, but the BLS specifically noted that it "had no discernible effect on the national employment and unemployment data for July, and the response rates for the two surveys were within normal ranges".

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok