Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWITZERLAND DATA

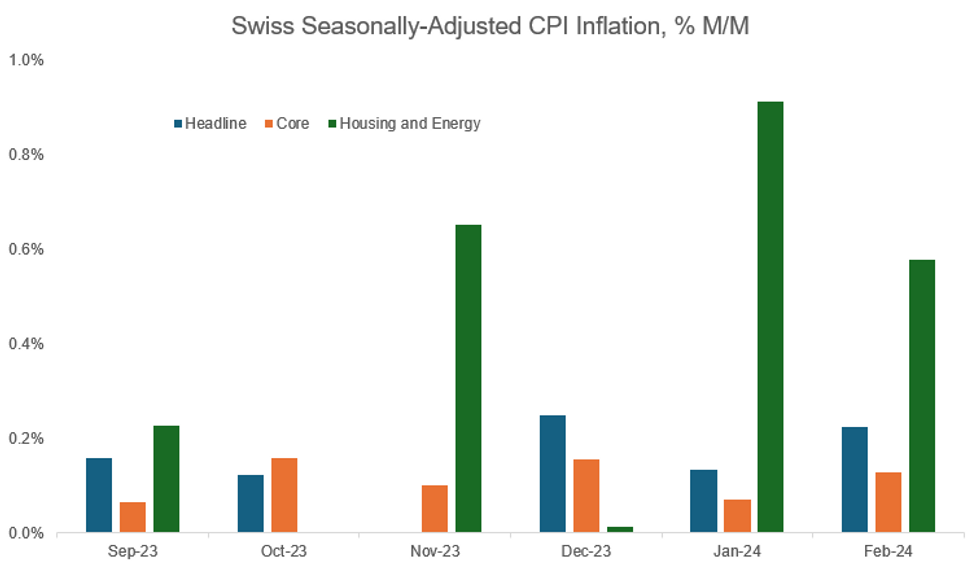

Looking at February's Swiss CPI inflation release on a more granular basis, MNI's calculations show that the closely-watched housing and energy category, within which the SNB projected inflation ticking up in Q1 2024, slowed but remained elevated on a sequential seasonally-adjusted basis.

- Specifically, MNI sees headline inflation at +0.22% M/M SA (vs +0.13% prior), core inflation at +0.13% M/M SA (vs +0.07% prior) and inflation in the housing and energy category at +0.58% M/M SA, clearly lower than January's +0.91% but still higher than the +0.25% average of the last 12 months.

- This comes alongside rental price inflation increasing on a yearly basis in February, to +2.7% Y/Y (vs +2.2% Y/Y prior) materializing the SNB's predictions from its December meeting at least partly, so the downtick in monthly seasonally adjusted inflation in the housing and energy category was driven by electricity prices, which inflated in January on a monthly comparison but stayed flat in February as electricity rates only change at the beginning of each year in Switzerland.

- Looking at other drivers of the headline figure, air transport contributed the strongest on a monthly basis (+0.13pp), but that uptick seems seasonally-driven as the category saw deflation on a yearly comparison in February (-3.2% Y/Y Feb vs +5.9% Jan).

- A selection of food items were the strongest negative monthly contributors in February (-0.02pp contr. of berries, -0.01pp of beef).

MNI, CH FSO

MNI, CH FSO

MNI London Bureau | +44 203-865-3809 | edward.hardy@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok