Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

DATA REACT

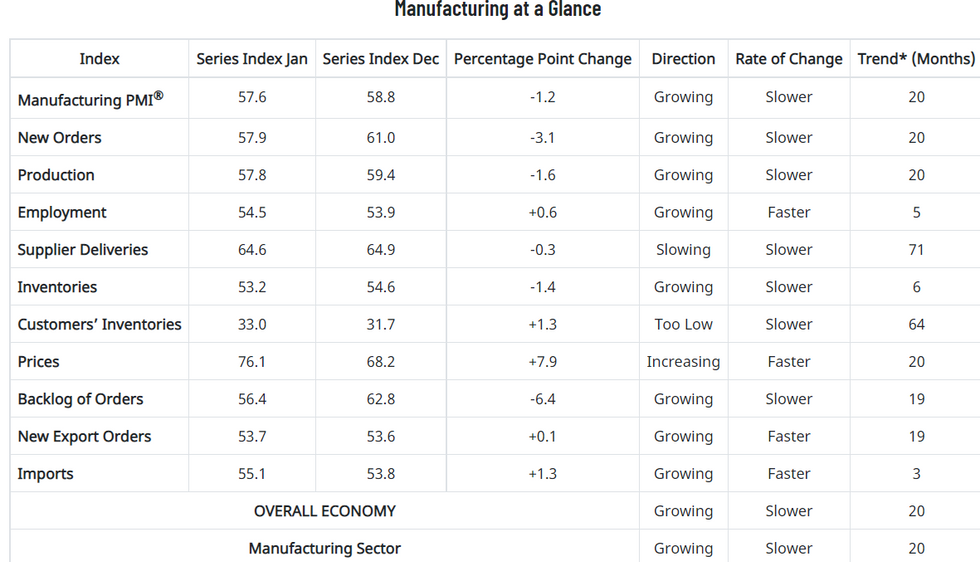

Headline US January ISM Manufacturing and New Orders came in line with expectations for a softening vs December, but arguably the most-watched item of the day - prices paid - unexpectedly accelerated and fairly significant fashion (76.1 vs 67.0 exp and 68.2 prior).

- Employment better than expected (54.5 vs 53.0 exp., 53.9r prior), but maybe not enough to move the needle for Friday's January payrolls report.

- The weakest new orders and production since mid-2020, combined with growing backlogs, suggest that the headline figure belies continued problems with supply chains.

- The report maintains the prevailing narrative of a strong labor market and supply chain issues weighing on growth potential, combined with stubborn price pressures, and will do nothing to derail expectations for increasingly aggressive Fed tightening policy this year.

- Front Eurodollar futures dipped to session lows before bouncing, with the Tsy curve flattening but then re-steepening; the USD continues to gain from session lows.

Source: Institute For Supply Management

Source: Institute For Supply Management

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok