Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

MNI (London)

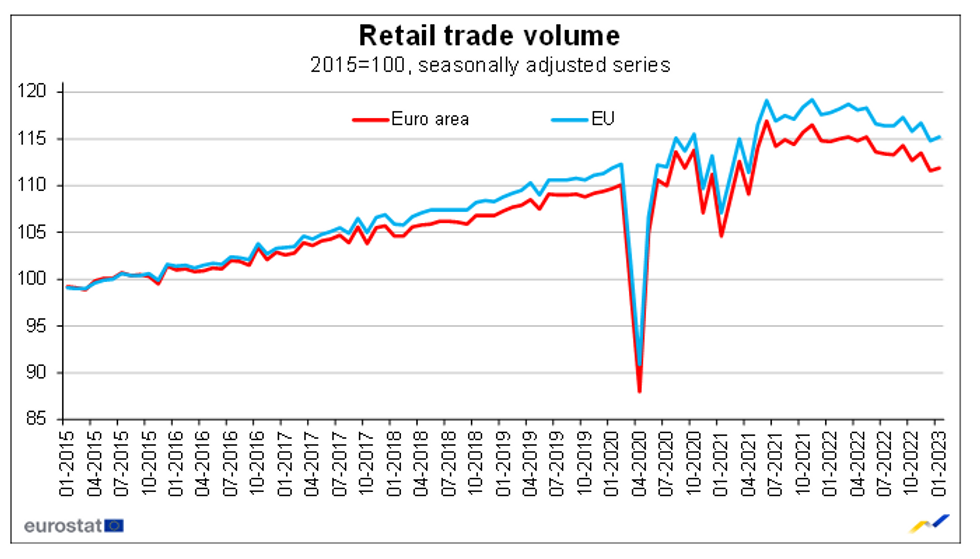

EUROZONE JAN RETAIL SALES +0.3% M/M (FCST +0.6%); DEC -1.6%r M/M

EUROZONE JAN RETAIL SALES -2.3% Y/Y (FCST -1.8%); JAN -2.8% Y/Y

- Euro area retail trade was weak in January, rising a modest +0.3% m/m after the upwardly revised -1.6% m/m contraction in December. Sales remained -2.3% lower than January 2022 levels.

- With both headline prints below consensus expectations, the January data implies a weak start to 2023 after a contractive Q4.

- Yet January weakness on the month was largely due to the -1.5% m/m fall in auto fuel. Both food/tobacco and and non-food sales rose, by +1.8% m/m and +0.8% m/m respectively. This signals a marginal improvement in underling spending in line with slowly recovering consumer confidence in recent months.

- Looking forward, eurozone consumer confidence continued to recover for a fifth month in the February survey, with promising signs of purchasing intentions improving. The European Commission retail trade index edged up to only marginally negative in February. With inflation remaining elevated, improved consumer sentiment seeing a rebound in retail demand remains unlikely for the time being.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok