Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US OUTLOOK/OPINION

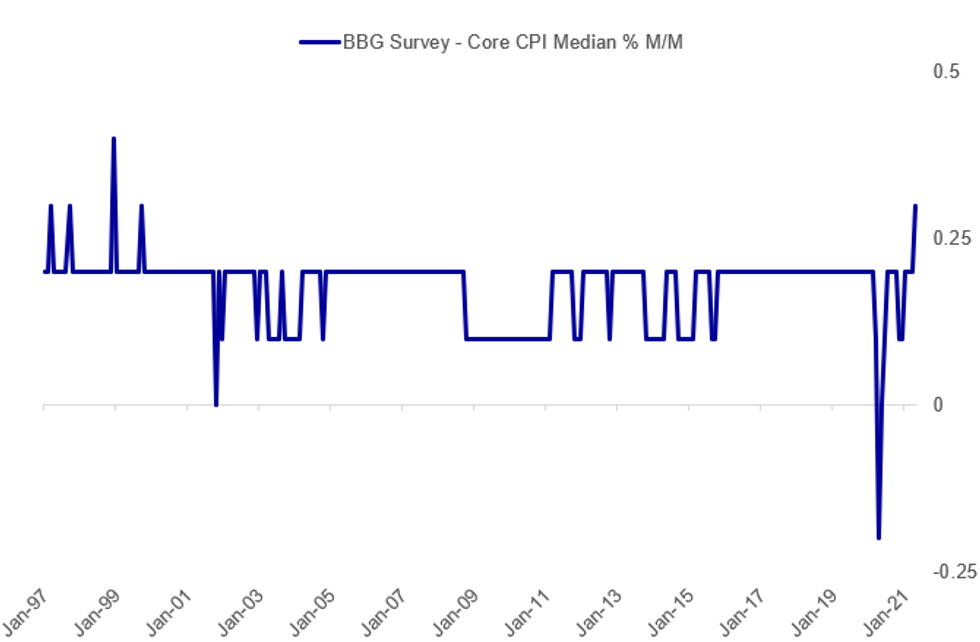

Re today's CPI release: repeating this from yesterday...and a few sell-side previews coming up.

- April headline CPI seen by BBG consensus coming in at +0.2% M/M (vs +0.6% prior), jumping to +3.6% Y/Y (+2.6% prior). And core seen +0.3% (vs 0.3% prior), likewise jumping to +2.3% Y/Y (+1.6% prior).

- The median estimates for the core CPI reading are at the very right-hand-tail of the historic distribution, at +0.3% M/M (per BBG estimates). That's the highest median expectation since the Sep 1999 consensus also hit +0.3% (see chart below). The survey high is +0.5%, joint-highest in the past 8 years with Aug-2020 (survey low is +0.1%).

- This comes after last week's large downside nonfarm payrolls miss, which was the largest for NFPs since at least 1998. There are good fundamental reasons to expect a big M/M jump in core prices, but with such lofty expectations (at least by historic standards), the bar is set lower for yet another downside miss in a key data release.

- Analysts' opinions on the core reading largely hinge on whether some of the outsized price gains in March repeat or - as usual in CPI reports - fade somewhat in the subsequent month.

BBG, MNI

BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok