Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

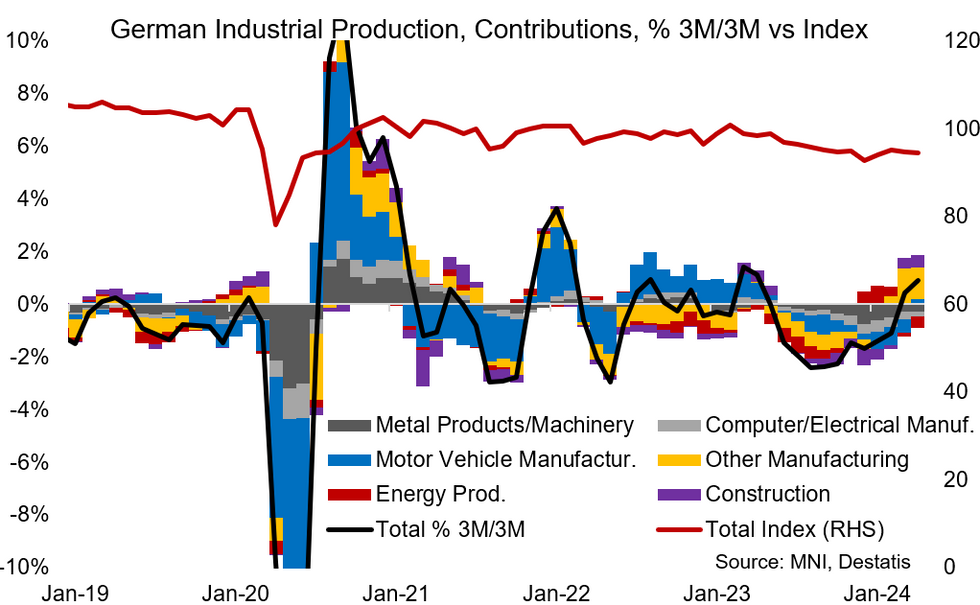

German industrial production came in short of expectations in April, printing -0.1% M/M (vs +0.2% cons; -0.4% unrevised prior). On a yearly comparison, industrial production continued to decline but at -3.9%Y/Y (vs -3.0% cons) this was less of a decline than the revised April print of -4.3% Y/Y (revised from -3.3%) amid base effects.

- Revisions driven by price index updates suggest that German industrial activity was weaker on the margin in Q1 than previously thought - with February's sequential growth further downwardly revised (by a further -0.5p to +1.2% M/M; the initial print was +2.1%).

- Taken by itself, April's stall in the headline rate came on the back of weaker construction production, which partly reversed its weather-related strength from earlier in the year, and stronger energy production. These two factors broadly net each other out. Manufacturing came in at +0.3% M/M (vs -0.2% prior).

- This suggests growth in the German industrial sector is still not really picking up, even though the 3M/3M measure increased for the fourth consecutive month and now printed a comparatively solid +0.9% (vs +0.4% prior).

- Looking at the individual categories within manufacturing, motor vehicles (+4.2% M/M vs +0.3% prior) and food (+3.4% vs -2.8% prior) stand out positively while wood (-2.9% M/M vs +2.2% prior) and glass production (-1.9% vs -1.0% prior) printed weaker.

- Looking ahead, MNI's collation of sellside analysts sees a recovery in IP for the next quarters, with the Q2 & Q3 median estimates standing at -3.5% Y/Y (consensus has been upwardly revised by 0.5pp during the last month), and -0.4% Y/Y (+0.2pp revision). The truck toll index, which is indicative of industrial activity, meanwhile printed lower again in May (-1.0% M/M vs +0.9% prior).

- Survey data continues to suggest that sentiment in German industry is starting to look a little less gloomy, although from a very low level.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok