Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Last week was a big week for UK data. We talk through the major releases but note that markets are back to pricing in around a 90% probability of a February hike, this is the same level as the beginning of last week but down from the peak of around 105% seen after the inflation data on Wednesday. Similarly we are back to around 4 hikes fully priced in by the November meeting, again the same as a week ago, down from around 4.4 hikes on Wednesday.

- Looking ahead to this week, we have flash PMI data due for release today which will be interesting (but is of lesser importance to the MPC than last week’s data). Outside of that we only have tier 2 data like public sector borrowing, CBI data and Nationwide house price data.

- This week also has no scheduled MPC speakers ahead of next week’s Monetary Policy Report and policy decision. We discuss the comments from Bailey, Cunliffe and Mann last week.

- We also touch on external drivers for UK markets and "partygate".

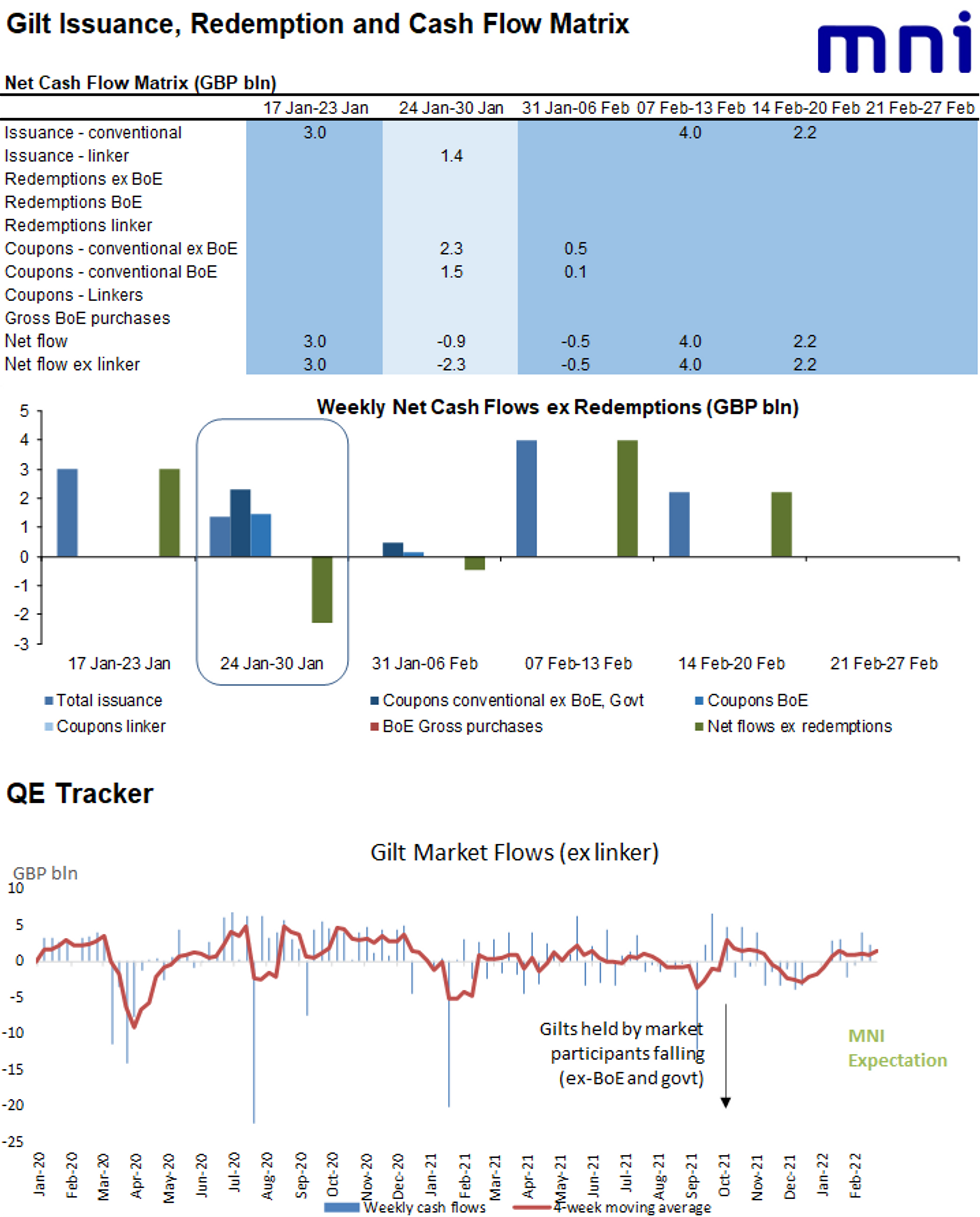

- See the full document for gilt supply previews for the week ahead, QE tracker and BOE purchase analysis, cash flow matrix and issuance calendar.

For the full document click the link below:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok