Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

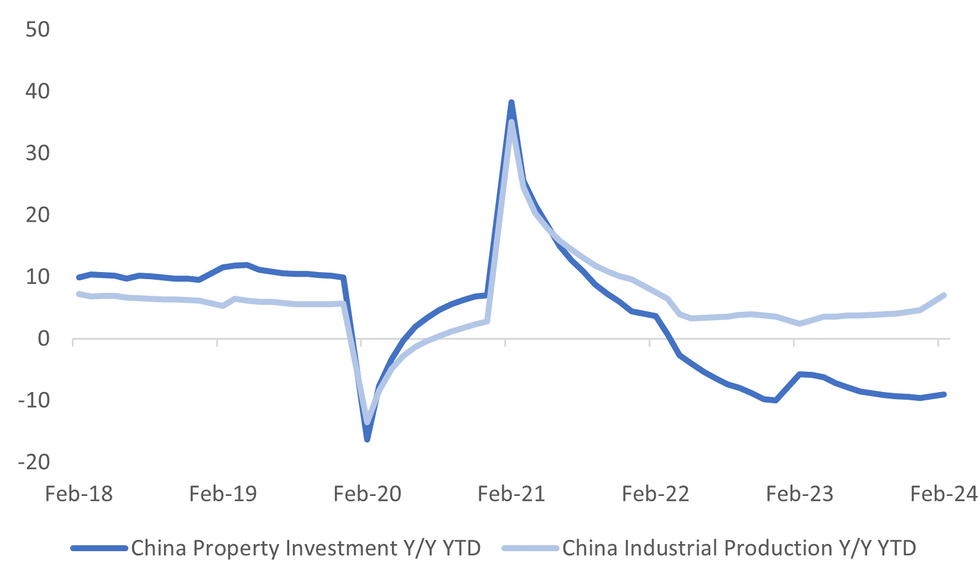

China Feb activity data was better than expected, with upside surprises recorded in terms of industrial production and fixed asset investment growth. Retail sales and property investment were slightly weaker than forecast, while the unemployment rate ticked higher.

- IP growth was 7.0% in ytd y/y terms, against a 5.2% forecast. Strength was notable in manufacturing and utilities (with mining weaker). Still parts of metals were strong, as were tech /computers. Auto production eased to 9.8% from 20.0%.

- It was a similar story across the fixed asset investment space. State-owned enterprises continued to outperform, up 7.3% ytd y/y, but private enterprises recorded much more modest growth of 0.4%, albeit out of negative territory where we spent much of 2023. Infrastructure spending rose 6.3%, so still a source of support for aggregate growth.

- Property indicators remain weak. Aggregate investment was down -9.0% ytd y/y, against a forecast of -8.0%. Under construction (-11% ytd y/y) and new construction (-29.7% ytd y/y) weakened further against Dec outcomes. Funds for property development were also down to -21.1% ytd y/y (versus -13.6% in Dec).

- Retail sales was close to expectations at 5.5% ytd y/y, versus 5.6% forecast. The detail was mixed, with a clear slowing in restaurant and catering to 12.5% ytd y/y, but last year's bounce reflected emerging from lockdown. Spending on household electronics and automobiles rose in ytd y/y terms for Feb.

- The unemployment rate edged up to 5.3% from 5.1% in Dec last year.

Fig 1: China IP & Property Investment YTD Y/Y

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok