Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

BONDS

Japanese investors have been net buyers of foreign bonds for 5 consecutive weeks (based on data from the Japanese Ministry of Finance). While the weekly purchase sizes have not been particularly large in outright terms, the direction of net flows is at least consistent. Japanese investors have also been net sellers of foreign equities in 4 of those 5 weeks, pointing to the potential for at least a degree of maintenance re: target asset weights within portfolios among the data.

- Still, even when we adjust for sales of foreign equities, Japanese investors have allotted a net ~Y2.4tn to foreign assets over the aforementioned 5 weeks (per the MoF data), all of which has flowed into bonds.

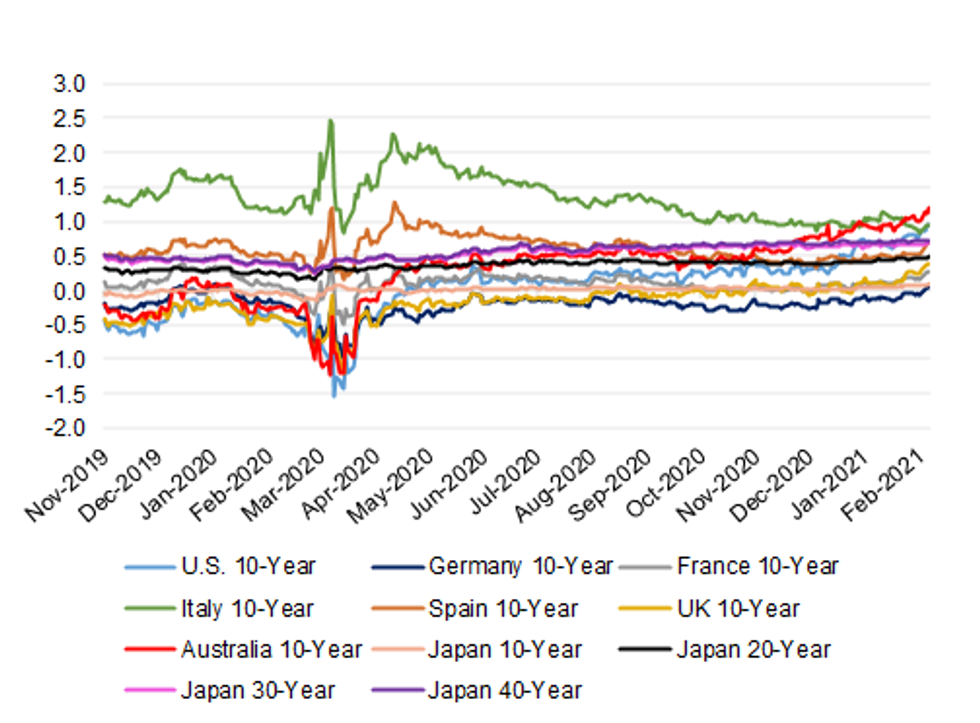

- A quick look at the FX-hedged yield backdrop for Japanese investors shows that the ECB/Draghi inspired decreditisation of BTPs and recent run of momentum behind the reflation trade leaves Australian 10-Year government bonds as a particularly attractive investment vehicle for Japanese investors.

- The same holds true in FX-unhedged terms, which is particularly important given that the sell-side points to widespread FX-unhedged positioning out of Japan when it comes to Australian assets.

Fig. 1: 3-Month Annualised Rolling FX-Hedged Yields From the Perspective Of A Japanese Investor

source: MNI - Market News/Bloomberg

source: MNI - Market News/Bloomberg

- Available via email now, for more details please contact sales@marketnews.com.

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok