Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Choppy Day For Few Surprises From Fed Chair Testimony

Choppy session for rates and equities, Tsy yields mixed, 5s30s curve making new high (162.463H, Aug 2014 levels) while equities manage to recover from broad losses to mildly higher (ESH1 -1.8% midmorning to +.26% by rates close).- Not much react to data: Feb consumer confidence better than exp: 91.3 vs 88.9 in Jan; DEC CASE-SHILLER SEAS ADJ HOME PRICE INDEX +1.3% M/M. Focus more on Fed chair Powell's semi annual testimony on economy to Sen Banking Comm -- though few surprises revealed.

- Tsy futures had started to reverse modest gains prior to Powell's testimony, support evaporated ahead the risk event coupled w/bounce in equities (weaker levels helped kick off bounce in Tsys in the first place). Some had hoped yield curve control would have been mentioned spurred sharp duration sell-off to new session lows (10YY 1.3875%H; 30YY 2.2144%H). Powell dismissed n/t inflation concerns, cautiously optimistic on outlook, has tools to keep funds rate in range. Stated central clearing and "digital dollar" being looked at.

- Heavy volumes tied to massive rolling of March to June, latter takes lead quarterly Friday (TYH/TYM>2M, >50% March volume by the close).

- US Tsy $60B 2Y Note (91282CBN0): draws 0.119% high yield (0.125% last month) vs. 0.118% WI, bid/cover 2.44 vs. 2.67 previous. Corp issuance hedging in the mix.

- The 2-Yr yield is up 0.4bps at 0.1149%, 5-Yr is down 2.1bps at 0.5777%, 10-Yr is down 0.5bps at 1.3602%, and 30-Yr is up 2.4bps at 2.1972%.

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N -0.00075 at 0.08050% (+0.00237/wk)

- 1 Month +0.00275 to 0.11763% (+0.00212/wk)

- 3 Month +0.01200 to 0.18750% (+0.01225/wk) ** (Record Low of 0.17525% on 2/19/21)

- 6 Month -0.00025 to 0.20375% (+0.00875/wk)

- 1 Year -0.00087 to 0.28463% (-0.00187/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $70B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $206B

- Secured Overnight Financing Rate (SOFR): 0.03%, $860B

- Broad General Collateral Rate (BGCR): 0.02%, $360B

- Tri-Party General Collateral Rate (TGCR): 0.02%, $327B

- (rate, volume levels reflect prior session)

- TIPS 1Y-7.5Y, $2.400B accepted vs. $4.852B submission

- Next scheduled purchases:

- Wed 2/24 1010-1030ET: Tsy 7Y-20Y, appr $3.625B

- Thu 2/25 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Fri 2/26 1010-1030ET: Tsy 0Y-2.25Y, appr 12.825B

EURODOLLAR/TREASURY OPTIONS: Summary

Eurodollar Options- +5,000 short Sep 95/96 put spds, 1.75

- +10,000 Blue Jun 92/95 call strip, 5.5

- 5,000 Green Apr 99.687/99.812 call spds

- +5,000 Blue Jun 83/86 put spds, 4.0

- +5,000 short Sep 96 puts, 4.0

- +8,000 Blue Sep 82/85 put spds 3.5 over 93 calls

- +5,000 Green Jun 91/93 put spds 0.5 over 96 calls

- Block +10,000 long Green Jun/Green Sep 97 call spds, 1.0

- Block 10,000 short Sep/long Green Mar 97 call spds, 1.0

- -20,000 long Green Mar 97 calls, 8.0 adding to shorts, OI>335k

- Overnight trade

- 3,000 Green Jun 99.562/99.625 call spds

- +5,000 Green Mar 99.687/99.75 1x2 call spds, 1.0

- +7,000 Blue Mar 87/88/90 put flys, 1.5

- -4,000 Blue Jun 86/88 put spds vs. 92 calls, 5.0-4.5

- Block: Adds to 2,500 traded Monday from 5-5.5: +15,000 short Sep 99.75 puts, 7.0 vs. -5,000 Blue Sep 98.625 puts, 15.5, 5.5 net on the 3x1 put spd post at 0712:01ET

- -10,000 TYJ 133.5/135.5 strangles, 37

- over 40,500 TYJ 135.5 calls, 13-15

- 3,300 TYK 136.5 calls, 11

- +1,000 FVM 125 straddles, 102.5

- Overnight trade

- +10,000 TYJ 135.5 calls, 14-12

- 5,200 TYJ 131.5 puts, 6

- 5,700 TYJ 132 puts, 10

- +2,500 TYJ 131.5/133.5 2x1 put spds, 16

- +2,500 TY wk4 133/133.5 put spds, 3

- 1,500 FVK 123.5/124 put spds

BONDS/EGBs-GILTS CASH CLOSE: Gilts Underperform As Long End Continues To Weaken

Gilts underperformed Tuesday with the long end getting hit hard, 30/40/50-year yields up 7+bps.

- German yields rose but in more subdued fashion.

- Periphery spreads widened as risk appetite proved mixed-to-lower.

- UK labour market data was mixed (strong earnings, weak employment).

- Germany sells 10-Yr Bund Wednesday; Haldane, Bailey among other BOE speakers.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is up 0.4bps at -0.682%, 5-Yr is up 1.4bps at -0.615%, 10-Yr is up 2.4bps at -0.315%, and 30-Yr is up 2.8bps at 0.195%.

- UK: The 2-Yr yield is up 0.1bps at 0.042%, 5-Yr is up 1.9bps at 0.284%, 10-Yr is up 4bps at 0.719%, and 30-Yr is up 7.3bps at 1.328%.

- Italian BTP spread up 2.3bps at 95.9bps / Spanish spread up 1.3bps at 67.9bps

OPTIONS EUROPE SUMMARY: Schatz And Bobl Downside

Tuesday's options flow included:

- DUJ1 112.20/112.10 1x2 put spread bought for 1.5 in 5k

- DUK1 112.20/10ps 1x2, bought for flat in 4k

- OEK1 134.25/135.75 RR, bought the put for 6.5 in 7k

- RXJ1 170/168.5ps 1x2, sold at 8.5 in 3k

- RXJ1 173/174cs 1x1.5, bought for 10 in 3k

- RXJ1 173/174cs vs 170.5/170ps, bought the cs for flat in 1k

- RXJ1 171/170/169put fly 1x1x1 ratio, sold at 73-71 in 3k

- 2LM1 99.62/99.37/99.12p fly sold down to 5 in 5k

- 2LM1 99.62/99.37/99.12p fly, sold at 4.75 in 4k

- 3LU1 9912/98.75ps, sold at 7.5 in 8k

- 3LZ1 97.62p, bought for half in 5k

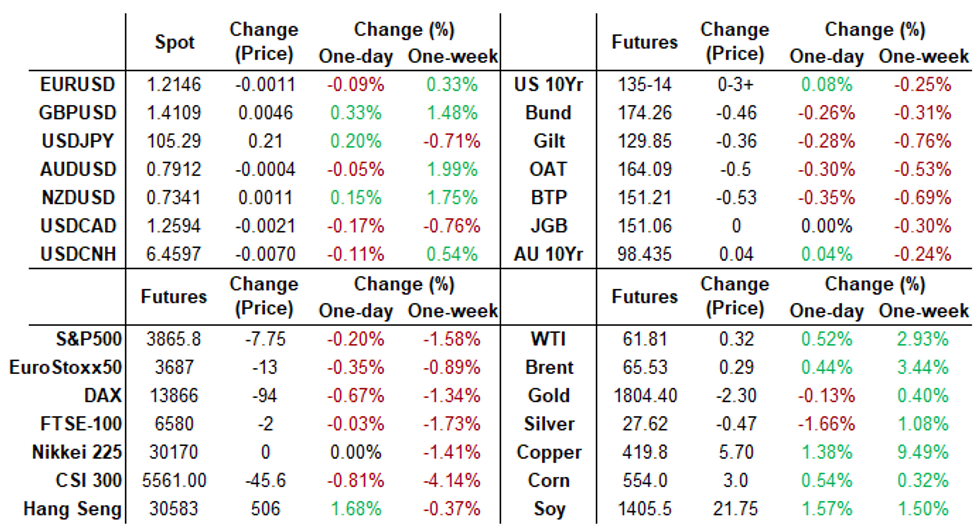

FOREX: Stellar Sterling as GBP/USD Tops 1.41 For First Time Since 2018

GBP's outperformance continued Tuesday, with the currency outperforming all others in G10. Today's moves are further evidence that the market is heavily endorsing the UK government's gradual, but solid, reopening plan which looks to remove all COVID-19 restrictions on June 21st. GBP/USD topped all near-term resistance ahead of the psychological handle, opening a move on the 1.4167 76.4% Fib retracement for the 2016 - 2020 sell-off.

- Elsewhere, the greenback was mixed, taking little from the appearance of Fed chair Powell in front of the Senate Banking Committee. The USD index was mixed-to-lower, but managed to steer clear of testing the key support at 90.05.

- The poorest performer Tuesday was CHF, which fell against all others in G10 despite a less than impressive turn out from equities. USD/CHF neared the 2021 highs of 0.9045.

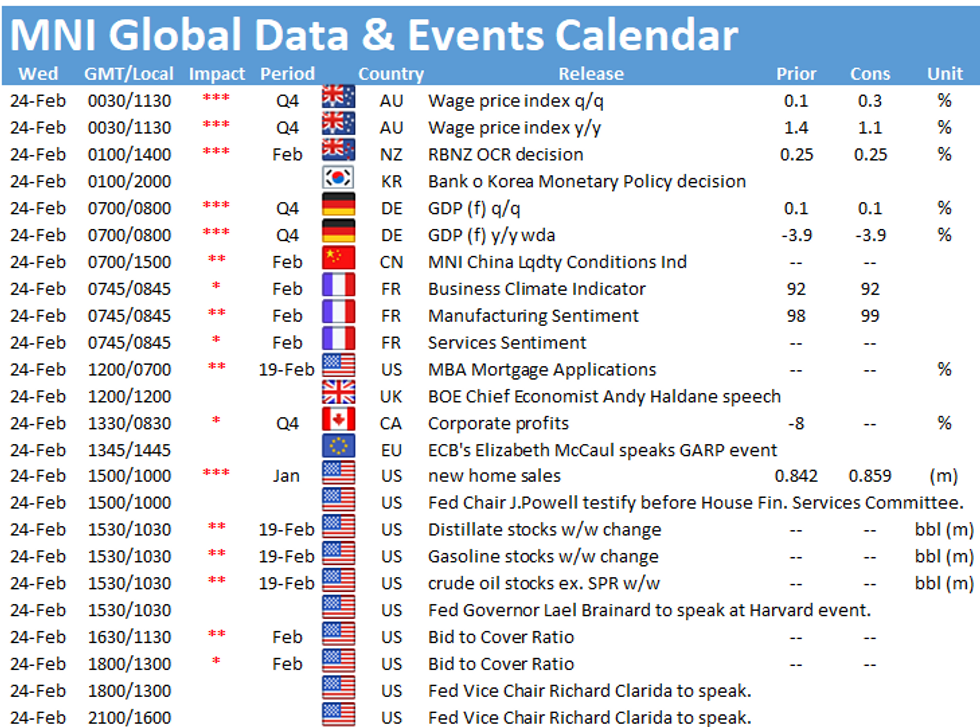

- Wednesday is a light session for data, with no tier releases due across the continent or the US. The speaker slate should be of more interest, with comments due from BoE's Bailey, Haldane, Broadbent, Vlieghe and Haskel as well as Fed's Powell (again), Clarida & Brainard.

FX OPTIONS: Expiries for Feb24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2000-05(E627mln), $1.2035-50(E768mln), $1.2090-1.2100(E1.1bln), $1.2130-35(E1.0bln), $1.2150-60(E1.3bln), $1.2170-85(E1.5bln-EUR puts), $1.2200-10(E728mln)

- USD/JPY: Y103.70-80($1.6bln), Y103.95-15($1.2bln), Y105.00(E1.7bln), Y105.65-80($3.2bln), Y105.95-15($1.3bln), Y107.00-05($1.0bln)

- EUR/GBP: Gbp0.8650(E534mln), Gbp.0.8700-20(E570mln)

- AUD/USD: $0.7700-15(A$1.2bln), $0.7800(A$1.4bln), $0.7850(A$529mln), $0.7865-75(A$1.7bln), $0.7910(A$939mln)

- USD/CAD: C$1.2690-1.2700($1.3bln)

PIPELINE: Waiting For Western Union Launch

- Date $MM Issuer (Priced *, Launch #)

- 02/23 $5.5B #Fidelity National Information 6-Part: $750M each: 2Y +30, 3Y +40, 7Y +75 and 20Y +110; $1.25 each: 5Y +60 and 10Y +95

- 02/23 $1B #Macquarie Bank 15NC10 +170

- 02/23 $1B #Interpublic $500M 10Y +105, $500M 20Y +135

- 02/23 $1B #Southern Company $600M 3Y +38, $400M 7Y +80

- 02/23 $Benchmark Western Union 5Y +80a, 10Y +140a

- 02/23 $Benchmark Bank of New Zealand investor calls

- 02/23 $Benchmark Peru, includes EUR issue investor calls

- Rolled to Wednesday:

- 02/24 $Benchmark KFW 3Y +2a

- 02/24 $Benchmark ADB 10Y +12a

EQUITIES: Tech Knocked, NASDAQ Suffers

Equity indices fell Tuesday, with the tech sector in particular taking a knock, leading the NASDAQ to underperform all others. The NASDAQ Comp fell over 2.5%, with big name stocks Apple, Tesla and Alphabet falling sharply.

A reversal in momentum names was largely responsible for the pullback in equities, with markets also expressing some caution in the move higher in nominal yields in recent weeks. The US 10y yield remains in close proximity to multi-month highs, with some market participants expressing some caution that any bleed into real rates could cause further equity market upset.

The 50-dma undercuts as support for the e-mini S&P, today crossing at 3790.09. A break through here would open 3772.15 Fib support - marking the 76.4% Fib of the February rally.

COMMODITIES: WTI Futures Drift Back To Flat, Consolidate Gains

- Contracts across the curve were north of $50/bbl for the first time since early 2020 this morning. Despite front month drifting lower throughout the second half of the session, recent gains are consolidating and indicate bullish longer-term expectations.

- The Bloomberg Commodity Index is almost exactly flat on the day, evidence of a lack of momentum in either direction as markets fell flat following Chairman Jerome Powell's congressional testimony.

- In precious metals, gold and silver both underperformed and came under pressure in the lead up to the speech. Silver, in particular, dropped through yesterdays lows to print $27.25 and despite a relief rally is currently posting losses of 1.8% on the day.

- Copper resilient as ever, up another 1%. Spot prices tagged above $9300/ton, another high since 2011 and continues to reflect the upbeat forecasts from sell-side analysts.

- Bitcoin remains towards the lower end of the day's range after considerable selling pressure overnight caused the cryptocurrency to shed 20% from high to low. Currently at $47,200 it remains down 14% on the day.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.