Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Pres Biden Rules Out Omicron-Tied Lockdown This Winter

Mkts still skittish to Omicron/Covid variant related headlines that sent bond soaring last Friday. Rates rebounded on the Asia session open, pared gains and held narrow range into early London trade.- Otherwise the Tsy week opener was rather muted on light volume (TYZ1 <875k) w/ some desks still lightly staffed after Thanksgiving holiday. Tsys extended lows (30YY 1.9087%H) back to around the middle of Fri's range -- rebounded after mixed data: Pending Home Sales +7.5% vs. 1.0% exp; Dallas Fed Mfg 11.8 vs. 15.0 exp.

- Sources report domestic Real$ acct buying in 10s pick up after central bank buying in 5s and 10s earlier, not to mention over 21,000 Block buys in FVF from 121-02 to 121-07.

- Buying waned: Yield curves held steeper as support for 5s-10s evaporated, equities making new session highs (ESZ1 +74.0 to 4469.75) after Pres Biden ruled out lockdowns this winter to combat spd of Omicron-Covid variant.

- Fed Chairman Powell spoke briefly today/gives testimony on CARES Act with Tsy Sec Yellen on Tue-Wed, unlikely much will be conveyed to upset markets prior to Fed media/policy blackout that starts Midnight Friday, final 2021 FOMC annc on Dec 14-15.

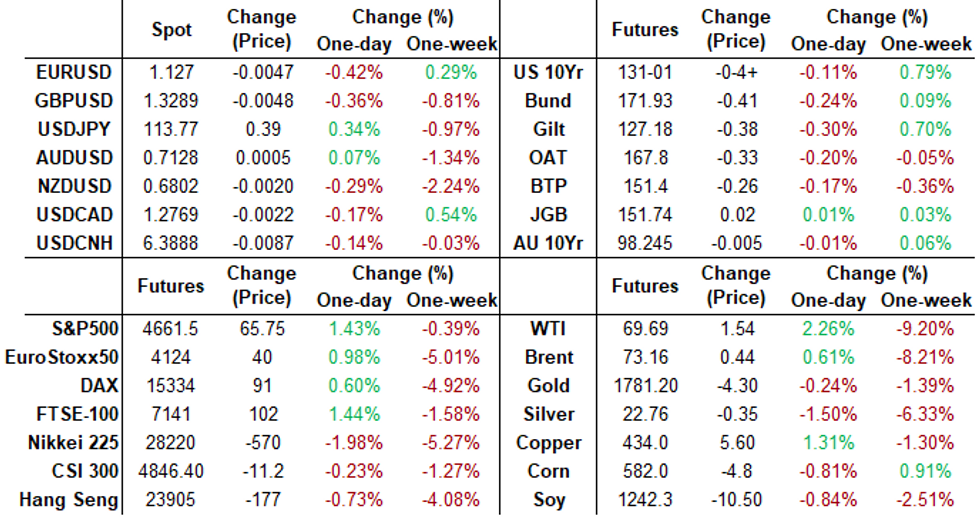

- The 2-Yr yield is up 1.8bps at 0.5157%, 5-Yr is up 2.7bps at 1.1871%, 10-Yr is up 5.5bps at 1.5277%, and 30-Yr is up 5.5bps at 1.8764%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00225 at 0.07638% (-0.00187 total last wk)

- 1 Month +0.00887 to 0.09925% (-0.00300 total last wk)

- 3 Month -0.00450 to 0.17088% (+0.01138 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00000 to 0.24600% (+0.01662 total last wk)

- 1 Year +0.00950 to 0.41988% (+0.01863 total last wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $85B

- Daily Overnight Bank Funding Rate: 0.07% volume: $268B

- Secured Overnight Financing Rate (SOFR): 0.05%, $895B

- Broad General Collateral Rate (BGCR): 0.05%, $334B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $327B

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, $7.351B accepted vs. $22.425B submission

- Next scheduled purchases

- Tue 11/30 1010-1030ET: Tsy 7Y-10Y, appr $2.825B

- Tue 11/30 1100-1120ET: Tsy 22.5Y-30Y, appr $1.600B

- Wed 12/01 1100-1120ET: Tsy 4.5Y-7Y, appr $5.275B

- Thu 12/02 1010-1030ET: TIPS 7.5Y-30Y, appr $1.075B

- Fri 12/03 1100-1120ET: Tsy 10Y-22.5Y, appr $1.425B

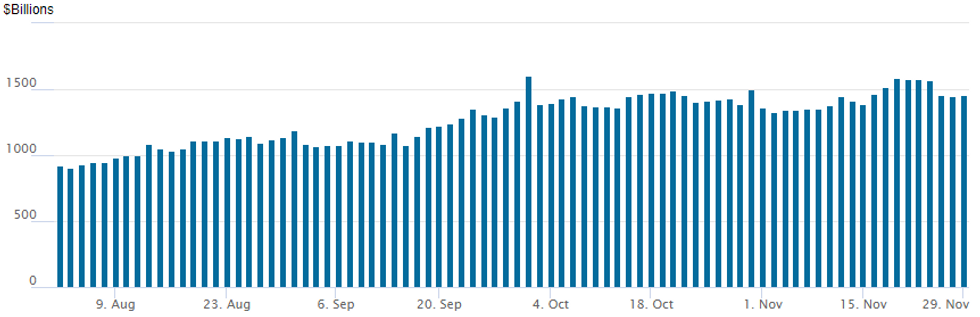

FED Reverse Repo Operation Bounce

NY Federal Reserve/MNI

NY Fed reverse repo usage bounces slightly: $1,459.339B from 79 counterparties vs. $1,451.108B on Friday. Record high remains at 1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +20,000 short Dec 98.87 puts, 1.0

- +4,000 short Feb 98.56/98.62/98.75 broken put flys

- Blocks, +25,000 Green Dec 98.75/99.12 put spds 20.0 over 99.62/100.00 call spds vs. 98.385/0.20%

- -15,000 short Dec 99.12 calls, 6, part tied to 99.12/99.37 put spds

- Overnight trade

- 6,000 short Jan 98.50/98.62/98.75 put flys

- 7,500 Blue Mar 98.50 puts

- 1,500 Blue Mar 97.50/97.75 3x2 put spds

- 3,000 Blue Jun 96.50/97.12 5x4 put spds

- Block, 5,000 short Jan 99.00/99.18/99.37 call flys, 3.5 vs. 98.93/0.05%

- 12,000 Green Dec 97.93/98.12/98.31 put flys

- 3,000 Green Dec 98.56 calls, 3.5

- 8,800 short Dec 98.87 puts, 2.0

- +10,000 TYG 128.5/132.5 put over risk reversals, 16

- 10,000 FVF 121.5 calls, 17.5, total over 32k on day most from 17-18

- +6,000 TYF/TYG 128 put calendar spd, 14

- Overnight trade

- 2,100 USH 155 puts, 107

- over 24,000 TYF 127.5 puts, 5-7, 6 last on 10k

- 10,000 TYF 131.25 calls, 15

- 12,000 TYF 128 puts, 10

- 2,000 TYF 128.5/129.5 put spds, 16

- 31,000 wk1 TY 128.5 puts, 2

- Block, 5,000 TYF 130.5 calls, 30

EGBs-GILTS CASH CLOSE: Partial Reversal

European FI partially reversed Friday's huge rally on Monday, though the emphasis is on "partially", with continued concerns over potential European lockdowns putting a lid on yield rises.

- German Nov CPI came in at the highest since 1992 and well above expected, after which Bunds weakened to session-worst levels. But they regained ground later amid a fade in the oil price rally, and reports that the gov't sought an "emergency brake" to deal with Covid.

- Gilt yields underperformed; as expected, UK authorities are set to expand vaccination efforts to head off the Omicron variant threat.

- Spain also saw strong price gains (as expected); Eurozone flash CPI out tomorrow.

- Periphery spreads tightened, with Spain outperforming.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.5bps at -0.751%, 5-Yr is up 1.5bps at -0.625%, 10-Yr is up 1.8bps at -0.317%, and 30-Yr is down 0.1bps at 0.019%.

- UK: The 2-Yr yield is up 3.3bps at 0.505%, 5-Yr is up 3.5bps at 0.652%, 10-Yr is up 3.6bps at 0.861%, and 30-Yr is up 1.9bps at 0.946%.

- Italian BTP spread down 1.5bps at 129.4bps / Spanish down 2.5bps at 73.9bps

EGB Options: Schatz And Bobl Puts Feature

Monday's Europe rates / bond options flow included:

- DUF2 112.20 straddle sold at 14.5/15 in 2k

- DUF2 112.30/112.10ps, vs 112.40c, bought for 6.5 in 2k

- OEF2 133/132.75ps, bought for 5 in 2.5k

- OEF2 134.00/133.00 1x2 put spread bought for 14 in 5k

- OEG2 133.50/133.00 put spread vs 135.50 call, bought for net -3.5 in 3.65k (bot ps)

- RXF2 171.50/170.5ps, bought for 14, 14.5, 15 in 30k. Rolling up strikes

- RXF2 171/168.5ps, sold at 19.5 in 3k

- 2RH2 99.75/99.50ps, bought for 2.25 in 8k

- 3LZ1 99.00/98.87ps, sold at 10.25 in 8.8k

FOREX: Greenback Regains Poise As Risk Sentiment Recovers

- Global equity indices are firmly in the green on Monday having retraced a significant portion of Friday’s losses as Omicron-variant fuelled panic subsided.

- The dollar index is up roughly 0.3% and has recovered over a half of a percent from Friday’s worst levels.

- EURUSD remained under pressure throughout the trading day and finds itself comfortably back below the 1.13 handle with multiple prints at 1.1258 providing some intra-day support.

- A more volatile session for USDJPY. Despite some initial strength following the open, a fresh wave of selling as Europe sat down prompted a marginal new low from Friday at 112.99. Since the early dip lower, price action has remained supportive, in line with broadly improved sentiment which saw USDJPY grind all the way back to session highs just below the 114 mark.

- NZDUSD has now fallen for a seventh consecutive trading session, notably breaching the August and yearly lows through 0.6805.

- In emerging markets, the improved risk backdrop did little to support the Turkish Lira with TRY weakness firmly back in the spotlight. USDTRY is currently up over 4% as the pair re-approaches 13.00 amid President Erdogan saying he will never advocate for a rate hike. As a reminder, last week’s highs reside at 13.45.

- Chinese Manufacturing PMI due overnight before the Eurozone publish their Flash estimates for November CPI. Canadian CPI and the MNI Chicago business barometer headline the North American docket. It is also worth noting the potential for increased volumes and volatility related to month-end rebalancing.

- Markets will also keenly await Friday’s November US employment report.

FX: Expiries for Nov30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1250-55(E905mln),$1.1350(E550mln), $1.1445-50(E1.5bln)

- USD/JPY: Y113.80($1.2bln), Y115.00($2.8bln)

- USD/CNY: Cny6.3800($525mln), Cny6.3900($552mln), Cny6.4300($891mln)

EQUITIES: Growth Over Value as NASDAQ Bounces Through Friday High

- US equity indices surged Monday, bouncing well off the Friday lows and erasing the drop for a number of markets - most notably the NASDAQ 100. Tech and growth stocks led the rebound, with the likes of Tesla, NVIDIA, and Live Nation Entertainment rallying sharply, despite being among the hardest hit on Friday.

- Stocks rallied alongside an appearance from President Biden, who talked down the need for further lockdown measures in the face of the new Omicron COVID variant, with the White House taking confidence in the higher levels of vaccine immunity reducing the need for activity restrictions.

- Moderna shares were also a highlight, with the company rallying sharply having stated that a new variant-targeting jab could be headed into production as soon as early 2022. Their stock price now sits as much as 40% off last week's lows.

- Across Europe, markets traded similarly positively, but rallies were slightly shallower, reflecting the more modest pullback in prices on Friday. The UK's FTSE-100 added around 1% thanks to strength across commodities, while Germany's DAX lagged after Goldman Sachs downgraded their view on Continental AG.

COMMODITIES: Oil Sees A Dead Cat Bounce?

- Oil has bounced after Friday’s rout as markets further assess the impact of the Omicron variant. WTI is back above $70 but remains more than $8 below Wednesday’s high. The bounce has been concentrated in front-ended contracts and is more modest further out the curve, suggesting there hasn't been a sea change in sentiment.

- WTI is up +4.2% on the day at $71.0 but remains clearly vulnerable. It cleared $69.58 on Friday (61.8% retracement of Aug-Oct rally), which potentially opens up the first firm support level of $67.4 (Nov 26 low).

- Brent is up +3.1% on the day at $75.0. First support is $71.9, the 61.8% retracement of the Aug – Oct rally, whilst first resistance is $77.58 (Nov 22 low).

- There has been little immediate reaction to Biden saying “the US won’t need shutdowns, lockdowns this winter”, potentially offset by the US Energy Envoy saying just beforehand that further releases from the oil reserve are possible.

- Earlier, Iran’s Foreign Minister said Tehran will not accept any request beyond JCPOA, helping support the bounce rather than driving it.

- Separately but as expected, the Saudi Energy Minister said the OPEC+ meetings have been shifted, with the technical meeting now on Wed and the ministerial committee on Thu.

- Additional USD risk tomorrow with Powell testifying before the Senate at 1000ET/1500GMT. Biden will unveil a strategy for dealing with the variant on Thursday.

- Gold meanwhile remains under pressure, down -1% at $1784. It’s towards the lower end of last week’s range and closing in on the support level of $1778.7 (Nov 24 low).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok