Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Strong Stocks, Rebound for Oil Weighs on Tsys

No data Monday (Fed in blackout), geopolitical tension between Russia and US over Ukraine ahead Tue's remote conf between Pres's Biden and Putin, did little to stem the apparent risk-on tone.- Rates extended session lows from the noon hour, near lows on moderate overall volumes (TYH2 just over 1.1M after the bell), short end yield curves steepened. Equities climbed (ESZ1 +60.0 to 4597.0 late), WTI crude crested 70.0, gold off 4.20 to 1779.09 late).

- Of note, 2Y/10Y Ultra curve steepener blocked in first half: +14,000 TUH2 109-06, buy through 109-05.75 post-time offer at 1012:25ET vs. -4,700 UXYH2 147-22, sell-through 147-22.5 post-time bid, off the CME's 4:1 spd ratio for the pair.

- Likely to ebb later in the week, Monday's total corporate debt issuance was robust, $6B Roche helped lead total high-grade debt issuance to $17B.

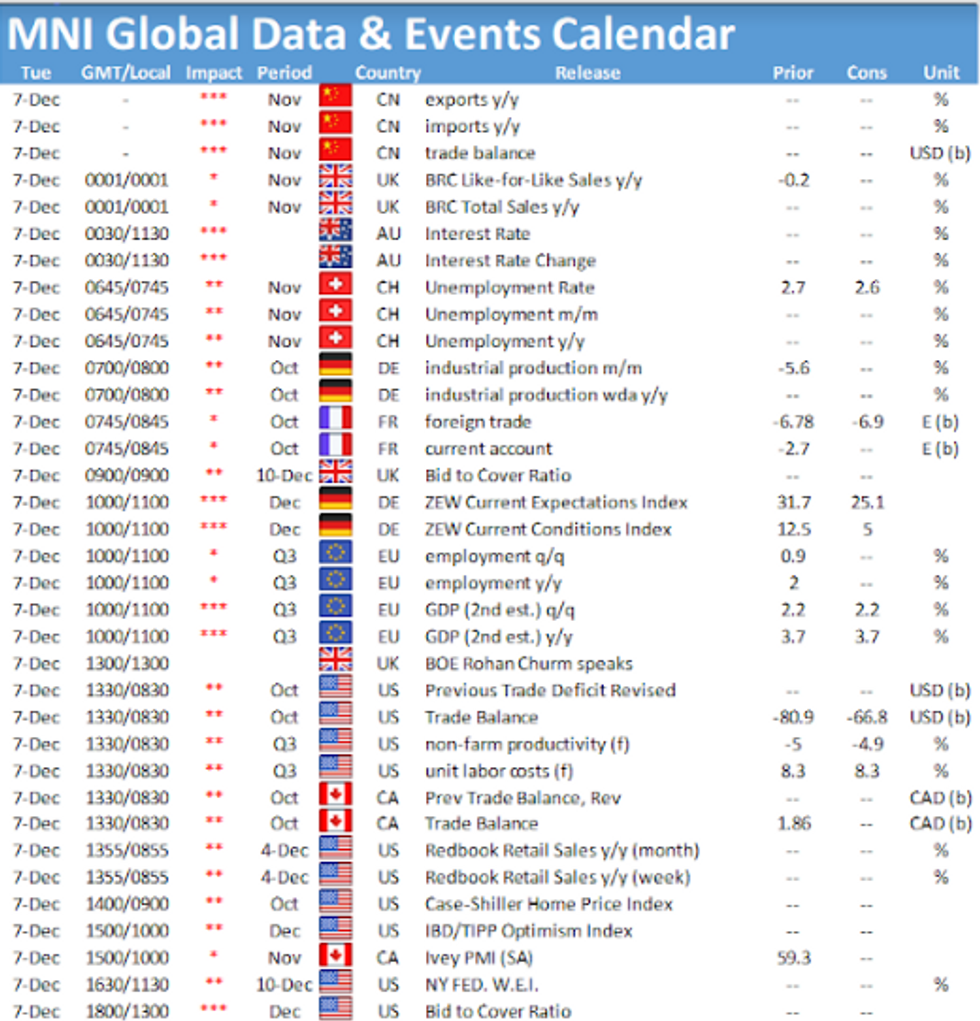

- Tuesday focus: Unit Labor Costs (8.3% est), Trade Balance (-$66.9B vs. -$80.9B prior)

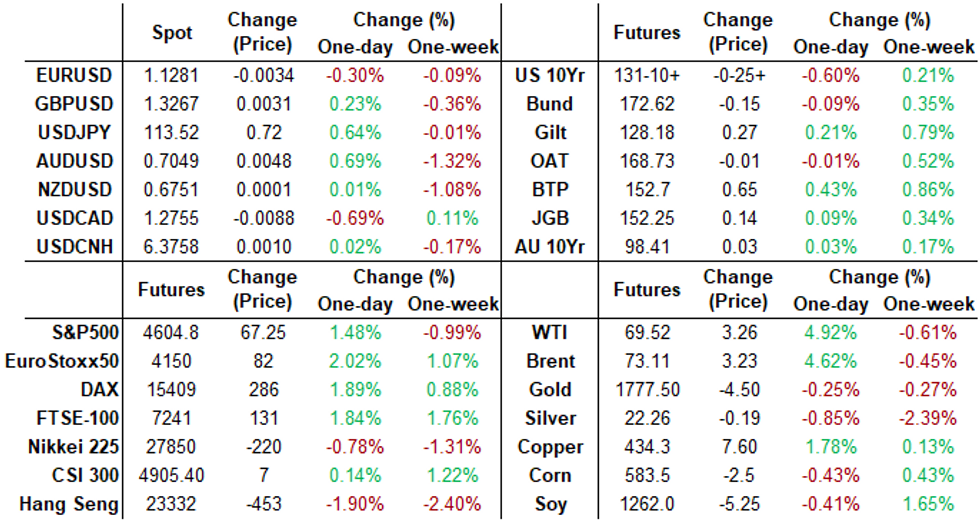

- The 2-Yr yield is up 4.2bps at 0.6292%, 5-Yr is up 7.9bps at 1.2111%, 10-Yr is up 9.5bps at 1.4376%, and 30-Yr is up 8.8bps at 1.7611%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00537 at 0.07113% (+0.00238 total last wk)

- 1 Month -0.00100 to 0.10313% (+0.01425 total last wk)

- 3 Month +0.00237 to 0.19000% (+0.01225 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00512 to 0.27625% (+0.00512 total last wk)

- 1 Year +0.00400 to 0.46550% (+0.05112 total last wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $77B

- Daily Overnight Bank Funding Rate: 0.07% volume: $261B

- Secured Overnight Financing Rate (SOFR): 0.05%, $1,015B

- Broad General Collateral Rate (BGCR): 0.05%, $361B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $338B

- (rate, volume levels reflect prior session)

- TIPS 1Y-7.5Y, $1.751B accepted vs. $4.660B submission

- Next scheduled purchases

- Tue 12/07 1100-1120ET: Tsy 22.5Y-30Y, appr $1.600B

- Wed 12/08 1010-1030ET: Tsy 2.25Y-4.5Y, appr $7.375B

- Thu 12/09 1010-1030ET: Tsy 0Y-2.25Y, appr $10.875B

- Thu 12/09 1100-1120ET: Tsy 10Y-22.5Y, appr $1.425B

- Fri 12/10 1010-1030ET: Tsy 7Y-10Y, appr $2.825B

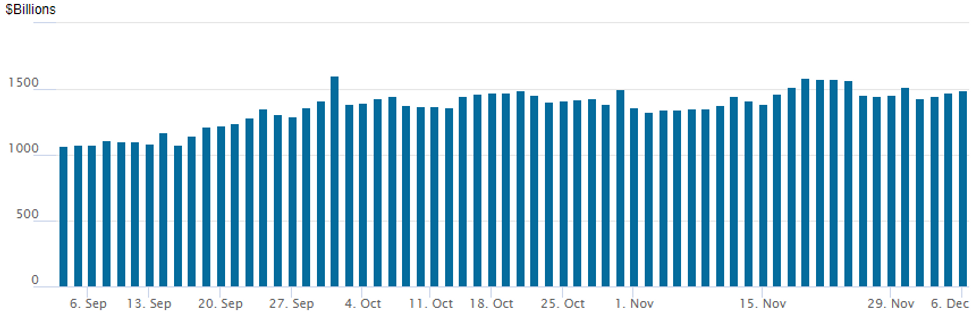

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $1,487.996B from 74 counterparties vs. $1,475.464B on Friday. Record high remains at 1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- Block, 12,000 long Green Mar'24 98.12 puts, 47.5 vs. 98.325/0.42%

- +2,000 short Mar 98.37/98.56/98.75 put flys, 2.25

- +3,000 Red Dec 98.50 puts, 15.5 vs. 99.02/0.30%

- +16,500 Red Dec'22 98.37/98.62/98.87/99.12 put condors, 5.0

- +2,500 short Jun 98.00/98.50 3x2 put spds, 18.5

- Overnight trade

- +7,500 short Dec 98.18 calls, 1.0

- 3,000 short Dec 98.93 puts, 3.5

- 5,400 TYF 132/133 call spds, 5

- 10,000 FVF 122/122.5 call spds, 4

- +5,000 FVH 119.5 puts, 18, >10.1k total on day

- -5,000 TYG 129/133 strangles, 38 earlier

- 8,700 TYG 128/129 put spds, 10

- +1,500 USG 159 puts, 49 vs. 163.15/0.22%

- Overnight trade

- 15,000 TYF 127.5 puts, 1

- -10,500 FVF 121 calls, 32-35.5

- -11,100 FVF 121.25 calls, 25.5-23.5

- 2,900 TYH 131 puts, 116

- +10,000 TUH 109 puts, 17

- +2,500 USF 161.5/162 2x1 put spds, 0.0

EGBs-GILTS CASH CLOSE: Italy Easily Outperforms

BTPs impressed to start the week, with Gilts and Bunds little changed, and futures rolling remaining a key theme going into the Eurex last trade date Wednesday.

- Italian 10Y spreads fell sharply following Friday's after-hours surprise ratings upgrade from Fitch (to BBB from BBB-). Conversely, Greek spreads widened following today's announcement of an exchange/buyback with bid deadline Friday.

- 10Y Gilt yields dipped to fresh post-Sept lows; 30s to post-Jan lows. BoE Broadbent's comments today don't suggest he will vote imminently for a hike; little market reaction.

- Bunds were little changed, with early weakness (despite weak factory orders data) reversing.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.7bps at -0.726%, 5-Yr is up 0.8bps at -0.626%, 10-Yr is unchanged at -0.388%, and 30-Yr is up 0.6bps at -0.09%.

- UK: The 2-Yr yield is down 0.7bps at 0.468%, 5-Yr is down 1bps at 0.576%, 10-Yr is down 0.9bps at 0.738%, and 30-Yr is down 1.5bps at 0.825%.

- Italian BTP spread down 3.6bps at 126.7bps / Greek up 5.5bps at 165.6bps

EGB Options: German Puts, Feb Expiries

Monday's Europe rates / bond options flow included:

- RXG2 172/170 put spread bought for 34.5 in 6k

- RXF2/RXH2 173.00/174.00 call diagonal sold at 31 and 29 in 4.45k (sold March, bought Jan)

- RXG2 172.00/169.00 put spread vs 178.00 call sold at 7 in 1.5k (sold ps,bought call)

- DUG2 112.20/112.00 put spread sold at 6.25/6.75 in 10k

- SFIZ1 99.80/99.85 call spread sold at 1.5 in 2k - (note contract expiry Friday)

FOREX: USDCHF and USDJPY Rise As Risk Recovers, AUD Bounces From Support

- The greenback is broadly stronger to start the week as the USD index shows gains of 0.2%. The strong performance is largely down to firm rallies in both USDCHF (+0.98%) and USDJPY (+0.62%). With Omicron fears subsiding for now, there is a generally supportive tone for risk across the G10 currency space.

- Initial resistance is seen at 113.74 in USDJPY, the 20-day EMA. A breach would ease bearish concerns and signal a possible S/T base. Key resistance though is unchanged at 115.52, the Nov 24 high.

- Despite the general US dollar strength, AUDUSD is in firm positive territory to start the week, recovering 0.65%. Broad AUD gains are noted given the significant bounce against the euro and especially the Yen – AUDJPY +1.33%.

- Naturally, the firmer global equities/oil prices have created more benign conditions for risk-tied FX, however, the outperformance is notable and was likely bolstered by the PBOC easing in the form of a RRR cut. AUDUSD low overnight at 0.6995 came within 4 pips of the November 2020 lows and a key support.

- The Canadian dollar reacted well to the recovery in crude futures, with USDCAD retreating 0.6%, however NZD underperformed the session, extending the NZDUSD decline to 13-month lows.

- China trade data overnight along with the December RBA meeting. Germany will post their ZEW sentiment data before Canada’s Ivey PMI. Markets will remain focused on Wednesday’s Bank of Canada meeting before Friday’s release of US CPI.

FX: Expiries for Dec07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1325-30(E518mln), $1.1350-70(E1.6bln), $1.1535-50(E650mln)

- USD/JPY: Y113.90-00($1.0bln)

- GBP/USD: $1.3250(Gbp452mln)

- AUD/USD: $0.7100(A$1.0bln), $0.7200(A$606mln)

- USD/CAD: C$1.2735-55($1.4bln)

EQUITIES: Stocks Solid as South Africa Data Better Than Feared

- COVID re-opening names including the likes of Norwegian Cruiselines, American Airlines and Live Nation Entertainment stormed higher Monday, with (admittedly very early) data suggesting the new Omicron variant may be more infectious, but may result in fewer hospitalizations and fatalities.

- Wall Street traded uniformly higher, with the bluechip-led Dow Jones adding near 2%. The utilities and real estate sectors supported headline indices, although tech names underperformed, with semi-conductors a particular spot of weakness.

- European trade was similarly positive, with gains of 1.4-2.4% uniform across continental indices. Spain's IBEX-35 led gains, with Germany's DAX lagging slightly - although still booking gains of 1.4%.

COMMODITIES: Oil Up As Saudi Raises Prices, Omicron Fears Subside

- Oil futures are up 3% on the day, slowly grinding higher throughout the day in a narrow corridor after moving higher at open. It has been led by Saudi Aramco raising Jan oil prices for all crude grades to Asian and US buyers along with subsiding fears on the severity of Omicron.

- WTI is +3.43% at $68.53. Thursday’s rebound from the session low has defined $62.43 as a key short-term support, with initial support at $65.60. Resistance is seen at $69.22 (Dec 3 high) after which we could see a short-term recovery towards the low $70s.

- Brent is +3.16% at $72.09. Similarly, the rebound from Thursday’s low suggests potential for a short-term recovery that would allow an oversold condition to unwind. Next firm resistance is $74.35 (Nov 30 high), key short-term support is $65.72 (Dec 2 low).

- Conversely, natural gas prices have continued to drop sharply, down -11.5% to $3.65 and a four-month low as record-high seasonal temperatures in the US have seen domestic stockpiles rebound.

- Gold is down -0.1% at $1781, with attention remaining on the base of a bull channel at $1762.1 drawn off the Aug 9 low and an important support. Initial firm resistance is set $1815.6 (Nov 26 high).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok