Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- MNI: Macklem Says Canada Turning Corner On Inflation

- BOC: THERE IS GROWING EVIDENCE THAT RESTRICTIVE ECONOMIC POLICY IS SLOWING ACTIVITY, ESPECIALLY HOUSEHOLD SPENDING, Bbg

- ECB'S MAKHLOUF: NEED SIMILAR HIKE TO DEC. IN FEB. AND MARCH .. INFLATION TOO HIGH, ECB DETERMINED TO MEET 2% TARGET, Bbg

- ECB'S NAGEL: MUSTN'T SOUND ALL CLEAR ON INFLATION TOO SOON .. but WOULDN'T BE SURPRISED IF RATES ROSE FURTHER AFTER MARCH, Bbg

- EU ANTITRUST ENFORCERS OPEN PROBE INTO MICROSOFT: POLITICO

Key links: MNI BOC WATCH: Macklem Hikes 25, Sees Pause If Growth On Track / MNI BRIEF: 50bp Hikes in Feb, March, Then We'll See - Nagel / US Treasury Auction Calendar

US TSYS: Late Market Summary: Dovish Take on Expected BOC 25Bp Hike

Whipsaw action in US FI markets Wednesday, finishing mildly higher, near middle of session range. Early volatility, rates rallied after Bank of Canadas 25bp hike to 4.5% and dovish inflation language. “Slower demand growth, combined w/ improvements in the supply chain, lead the economy into modest excess supply in 2023” MPR.

- BOC-tied support evaporated aby midmorning, yield curves bouncing off deeper inversion (and holding): 2s10s +8.092 at -68.087 (-77.338 low).

- While monthly core inflation suggests core has peaked rather than early indicator price pressures may be losing momentum helped drive early bid, reversal less a function of active sellers than support has waned following BOC Macklem's "conditional" pause comment.

- "Overall, we view the risks around our inflation forecast as balanced, but with inflation still well above our target, we continue to be more concerned about the upside risks. If these upside risks materialize, we are prepared to raise interest rates further."

- Trading desks reported prop and fast$ buying 10s as sector climbs back to steady/mildly higher, pre-auction short sets in 5s ahead today's $43B 5Y auction. Tsy futures gain slightly after strong $43B 5Y note auction (91282CGH8) stops through: 3.530% high yield vs. 3.555% WI; 2.64x bid-to-cover vs. 2.46x the prior month.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00057 to 4.30800% (+0.000286/wk)

- 1M +0.00129 to 4.50729% (-0.00599/wk)

- 3M -0.00729 to 4.81457% (-0.00100/wk)*/**

- 6M -0.00028 to 5.10829% (+0.00629/wk)

- 12M -0.00471 to 5.33929% (-0.00800/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.82971% on 1/12/23

- Daily Effective Fed Funds Rate: 4.33% volume: $104B

- Daily Overnight Bank Funding Rate: 4.32% volume: $287B

- Secured Overnight Financing Rate (SOFR): 4.30%, $1.163T

- Broad General Collateral Rate (BGCR): 4.27%, $464B

- Tri-Party General Collateral Rate (TGCR): 4.27%, $441B

- (rate, volume levels reflect prior session)

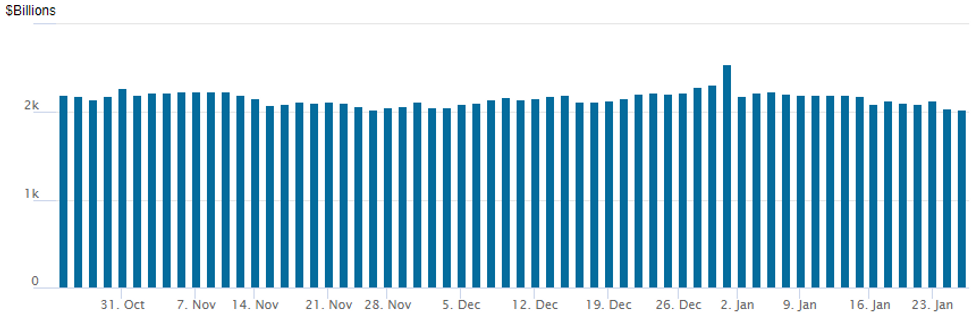

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,031.561B w/ 99 counterparties vs. prior session's $2,048.386B. Compares to Friday, Dec 30 record/year-end high of $2,553.716B (prior record high was $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

While the Asia Lunar New Year holiday has kept overall volumes muted this week - SOFR option volume remains robust with focused on low-delta puts/spds (hedging extended rate but smaller hikes). Wednesday is the first time since last week where a shift in low delta call and call spds after more consistent put trade has been noted.

Salient trades in the list below include +60,000 SFRZ3 97.00/97.50/98.00 call flys, 1.5 and 19,500 SFRZ3 96.25/97.00/97.50 broken call flys, 6.5 vs. 95.59/0.10%. Puts include 20,000 SFRU3 95.37/95.62 put spds, 17.5 ref 95.30.

- SOFR Options:

- Block, 8,000 SFRJ3 95.37/95.50 call spds, 1.25 ref 95.13

- Block, +8,000 SFRJ3 95.31/95.56 call spds, 2.5 vs. 95.135/0.15%

- BLOCK, 20,000 SFRU3 95.37/95.62 put spds, 17.5 ref 95.30

- Block/screen, +60,000 SFRZ3 97.00/97.50/98.00 call flys, 1.5

- Block, 5,000 SFRU3 96.25/96.75 call spds, 2.5 ref 95.295

- 3,250 SFRJ3 95.25/95.37/95.31/95.37 call condors

- 3,000 SFRZ3 94.75/95.00/95.25 put flys, 3.0

- -10,000 SFRU3 95.62 calls, 12.0 vs. 95.275/0.28%

- Block, 5,000 OQM3 97.25/3QM3 97.75 call spd, 1.5 short Jun over

- Block, 5,000 SFRZ3 97.00/97.50 call spds, 3.0 vs. 95.665/0.05%

- Block, 5,000 SFRJ3 95.25/95.37 call spds, 1.75 vs. 95.09/0.11%

- 2,500 SFRK3 95.18/95.31/95.50 call trees

- 2,000 SFRH3 96.75/97.50/98.00 broken call flys ref 96.15

- Block/screen, 19,500 SFRZ3 96.25/97.00/97.50 broken call flys, 6.5 vs. 95.59/0.10%

- 1,250 SFRK3 95.25/95.31 call spds vs. SFRN3 95.06/95.18/95.25/95.37 call condors

- 1,250 SFRN3 95.06/95.18/95.31/95.50 call condors ref 95.265

- 3,000 SFRM3 95.12/OQM3 96.12 call spds

- Treasury Options:

- 8,500 TYG3 114/114.5 put spds vs. TYH3 111/112 put spds

- 1,800 TYH 112.5/113.5/115.5/116 broken put condors ref 115-06

- 12,000 TYG 114.75/115 put spds, 5

- 2,500 TYG3 115.75/116.25 call spds

- 2,500 FVH3 111 calls, 11 ref 109-20.75

- 7,500 TYG3 116 calls, 4 ref 115-06

- 8,500 TYG3 114/114.5 put spds, 4 ref 115-03.5 -04

- 2,000 TYG3 115.75 calls, 4 ref 115-02.5

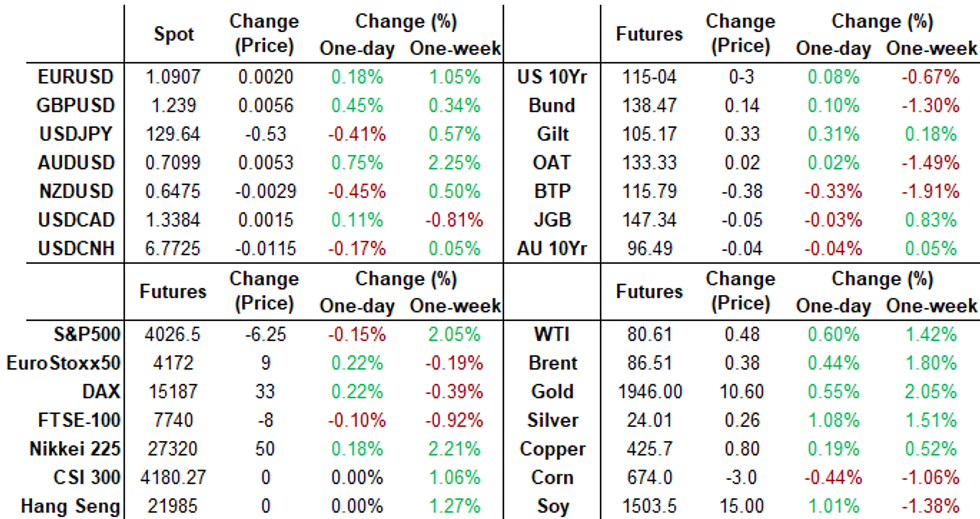

EGBs-GILTS CASH CLOSE: Early Rally Peters Out

Bund and Gilt yields finished well off their session lows Wednesday, with periphery EGB spreads likewise re-widening.

- Soft UK PPI data helped Gilts rally early, with BoE hike expectations dialled back and end-year cut pricing picking up.

- Hawkish commentary from ECB's Vasle, Makhlouf, and Nagel helped turn yields higher in early afternoon.

- After briefly ticking higher in mid-afternoon as the Bank of Canada signalled it was pausing its hiking cycle, the sell-off resumed.

- 10Y BTP spreads to Bunds fell below 174bp in the morning, but headed above 180bp in the afternoon amid the broader sell-off.

- Fairly limited data and speaker slate Thursday.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.5bps at 2.529%, 5-Yr is down 1.3bps at 2.176%, 10-Yr is up 0.3bps at 2.158%, and 30-Yr is up 1.6bps at 2.127%.

- UK: The 2-Yr yield is up 2.9bps at 3.407%, 5-Yr is down 3.9bps at 3.133%, 10-Yr is down 3.4bps at 3.243%, and 30-Yr is down 2.9bps at 3.593%.

- Italian BTP spread up 3bps at 179.1bps / Spanish up 0.9bps at 95.3bps

EGB Options: Mostly Upside In Euribor

Wednesday's Europe rates / bond options flow included:

- DUH3 1105.60/105.30ps vs 106.40c, bought the ps for -0.5 (receive) in 3k

- ERG3 97.00p, bought for 2.25 in 7.1k (ref 97.04)

- ERJ3 96.37/96.25ps vs 96.62/96.87cs, bought the cs for 6.75 in 5k

- ERJ3 96.625/96.75 cs vs ERJ3 96.375/96.25ps, bought the cs for 3.5 in 7.5k.

- ERM3 96.625/96.50/96.375p ladder bought for flat in 5k

FOREX: USD Index Hovering Close To Cycle Lows Approaching US GDP Data

- Greenback pressure resumed on Wednesday with the USD index gravitating towards the worst levels of the week and nearing fresh trend lows set last Wednesday. A light data calendar overall has seen the path of least resistance remain lower for the greenback ahead of key US growth data on Thursday.

- AUD strength remains the standout in G10, following a stronger set of inflation data in Australia, helping to push market pricing towards a 25bps hike for the February RBA meeting. In the process of rallying, AUDUSD has cleared resistance at 0.7063, the Jan 18 high. The breach confirms a resumption of the uptrend and maintains the bullish price sequence of higher highs and higher lows. Attention is on the next key resistance at 0.7137, the Aug 11 high where a break would strengthen underlying bullish conditions.

- Conversely, New Zealand inflation came in below RBNZ expectations, which has worked against the NZD (-0.32%), a key underperformer on the session.

- The Bank of Canada hiked 25bp but signalled that they should be in the position to pause rate hikes which also worked against the Canadian dollar. USDCAD had a firm spike from 1.3365 to 1.3425 following the release of the statement, however, broad USD weakness had seen the pair trade back close to the unchanged mark approaching the APAC crossover.

- EURUSD sits just shy of Monday’s high of 1.0927 with moving average studies continuing to highlight positive market sentiment. Sights remain on 1.0954, the Apr 11 2022 high.

- Despite Lunar New Year and the Fed’s blackout period continuing, markets will receive the advanced reading of Q4 US GDP tomorrow which will likely be a key indicator for US policy makers as we near the end of the tightening cycle. Friday’s release of US Core PCE Price Index will round off the week’s major data releases.

FX: Expiries for Jan26 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0890-00(E526mln), $1.0950(E825mln), $1.0980-00(E718mln)

- USD/JPY: Y127.00($1.6bln), Y127.50($755mln), Y130.00($2.0bln)

Late Equity Roundup: Late Recovery, Banks, Autos and Airlines Gaining

Major indexes recover off midmorning lows, Utilities still lagging while Financials and Consumer Discretionary sectors making late gains. SPX eminis currently trades -2 (-0.05%) at 4030.5; DJIA +10.79 (0.03%) at 33744.21; Nasdaq -17.4 (-0.2%) at 11317.78.

- SPX leading/lagging sectors: Utilities underperforming (-1.62%) specifically electrical: NextEra Energy: NEE -8.21% despite reporting better than expected profit/rev's, though bottom line disappointed. Next up: Communication Services (-0.50%) and Industrials (-0.46%), interactive media & services weighing on the former (Google -2.95%, Meta -0.75%).

- Leaders: Financials sector (+0.60%) gained in the second half w/ insurance and banks outperforming diversified financials (USB +5.12%, Key +1.90%, WFC +1.51%. Consumer Discretionary (+0.30%) next up - lead by autos (TSLA +1.11%, GM +0.44%, F +0.35%).

- Dow Industrials Leaders/Laggers: Boeing (BA) reversed early losses (203.18 low) to 213.84 (+1.5), McDonalds (MCD) +1.27 at 270.84, and Disney (DIS) +1.29 at 107.29. Laggers: AMGN -3.54 at 256.16, Travelers (TRV) -2.85 at 190.40, Chevron (CVX) -2.09 at 178.74.

E-MINI S&P (H3): Directional Triggers defined

- RES 4: 4194.25 High Sep 13

- RES 3: 4180.00 High Dec 13 and the bull trigger

- RES 2: 4090.75 High Dec 14

- RES 1: 4056.75 High Jan 23

- PRICE: 4032.5 @ 1505ET Jan 25

- SUP 1: 3901.75/3891.50 Low Jan 19 / Low Jan 10

- SUP 2: 3788.50/78.45 Low Dec 22 / 61.8% of Oct 13-Dec 13 uptrend

- SUP 3: 3735.00 Low Nov 3

- SUP 4: 3670.00 76.4% retracement of the Oct 13 - Dec 13 uptrend

S&P E-Minis are trading lower today. A key S/T resistance has been defined at 4056.75, the Jan 23 high. A break of this level would confirm a resumption of recent bullish activity and signal scope for a climb towards the 4100.00 handle and key resistance at 4180.00 further out, the Dec 13 high. The key short-term support to watch lies at 3901.75, the Jan 19 low. A break would be bearish. 4056.75 and 3901.75 represent important directional triggers.

COMMODITIES: Mixed Session For Crude, Gold Tests Resistance With Softer USD

- A mixed session for crude oil, quickly sliding ahead of the BoC decision before guidance of a pause helped risk assets recover with the USD weakening and equities firming.

- This was then followed by more idiosyncratic and mixed price action, with crude markets gaining and product markets falling after EIA data showed a smaller recovery in refinery utilisation than expected, strong crude exports and weak product demand.

- Elsewhere in oil news, Crude flows from Russia to India are set to top 1.5 million barrels a day this month, up from virtually zero less than a year ago according to Bloomberg vessel tracking and setting a new record monthly pace.

- WTI edges +0.4% higher at $80.46. Resistance remains at $82.66 (Jan 18 high) and support at $78.45 (Jan 19 low).

- Brent +0.2% at $86.31 and as with WTI, resistance remains at $89.18 (Dec 1 high) with support at $84.27 (20-day EMA).

- Gold is +0.2% at $1941, gaining later in the session as the dollar continues to weaken. A high of 1942.04 sees it come close to testing resistance at yesterday’s high of $1942.5, after which sits $1963.0 (76.4% retrace of Mar -Sep 2022 bear leg).

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/01/2023 | 0800/0900 | ** |  | SE | Economic Tendency Indicator |

| 26/01/2023 | 0900/1000 | ** |  | IT | ISTAT Business Confidence |

| 26/01/2023 | 0900/1000 | ** | | IT | ISTAT Consumer Confidence |

| 26/01/2023 | 1100/1100 | ** |  | UK | CBI Distributive Trades |

| 26/01/2023 | 1330/0830 | * |  | CA | Payroll employment |

| 26/01/2023 | 1330/0830 | ** |  | US | Jobless Claims |

| 26/01/2023 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 26/01/2023 | 1330/0830 | ** | | US | durable goods new orders |

| 26/01/2023 | 1330/0830 | *** | | US | GDP (adv) |

| 26/01/2023 | 1330/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 26/01/2023 | 1500/1000 | *** | | US | New Home Sales |

| 26/01/2023 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 26/01/2023 | 1600/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 26/01/2023 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 26/01/2023 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 26/01/2023 | 1800/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

| 27/01/2023 | 2350/0850 | ** |  | JP | Tokyo CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.