Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Inflation concerns mount further, 5-yr B/E rates narrow in on record high

- Tsy curve steepens amid sizeable corporate pipeline including $18.5bln Amazon deal

- Equities diverge, tech plummets on inflation threat

US TSYS SUMMARY: Curve Steepens, Markets Eye Sizeable Corp Supply

- US 10-yr yields opened the Monday session higher, before the belly of the curve saw some slippage through the Wall Street open, pressing 10-yr yields lower to touch 1.55%. This downward pressure eased as markets eyed sizeable supply from both the corporate pipeline as well as the busy auction schedule this week.

- The curve traded steeper as the long-end underperformed:

- 2-yr yield rose 0.6 bps to trade 0.151%

- 10-yr yield rose 2.3bps to trade 1.60%

- 30-yr yield rose 4.0bps to trade 2.317% - Tech sector fell sharply Monday, with the likes of Facebook and Alphabet leading losses after being downgraded at Citi. Citi forecast potential weakness in the online advert market, undercutting earnings growth for both firms. NASDAQ-100 fell as much as 2%.

- Corporate pipeline saw sizeable activity Monday, with $ deals amounting to as much as $45bln this week. Deals from Canada, JSW Hydro, Korea Expressway as well as talk of jumbo-sized issuance were in focus.

- Auction schedule kicks off tomorrow, with $58bln in 3-yr, $41bln 10-yr and $27bln 30-yr starting Tuesday.

Sizeable Move in Break-Evens Puts 5y B/E Rate Closer to Record High

- The inflationary outlook remains a focus for markets, with 10y break-evens continuing their march higher to touch new multi-year highs at 2.5857, highest since 2013. The 5-yr B/E rate topped the 2008 high on the way higher to 2.78. The series high 5-yr B/E rate was 2.9051 in 2005.

A few drivers/catalysts behind today's move:

- More Fed members doubling-down on stimulus plans (Fed's Evans: Fed has room to overshoot, will be a while before US has made enough progress to talk taper)

- Disappointing jobs gains on Friday further delaying any need to talk imminent withdrawal of stimulus

- NY Fed survey sees consumer inflation expectations at highest since Sept'13, with housing, rental expectations at new series highs.

- Sell-side eyeing upside risks to this week's CPI, PPI releases, with re-opening components to inflation baskets at risk of supply bottlenecks, driving up prices.

SHORT TERM RATES

USD LIBOR FIX:

- O/N 0.06338 (-0.00075)

- 1W 0.07150 (0.00212)

- 1M 0.09813 (-0.00325)

- 2M 0.13250 (0.00412)

- 3M 0.16750 (0.00762)

- 6M 0.19250 (-0.00025)

- 12M 0.26700 (-0.004)

NY Fed Operational Purchases

Accepts $3.601bn of 7-20Y Tsys, Total Submitted $11.272bn

Coming up:

- Tue 5/11 1010-1030ET: TIPS 1-7.5Y, appr $2.425B

- Wed 5/12 1500ET Update NY Fed Operational Purchase Schedule

EGBs-GILTS CASH CLOSE: Weaker But Yields Off Highs

Core FI traded weaker Monday with bear steepening in Bunds and Gilts, though yields ended off session highs as equities traded softer in the afternoon. Periphery spreads tightened.

- Fading odds of a Scottish independence referendum and further lockdown helped contribute to Gilt underperformance.

- ECB's Lane discussed possibility of slowing or hastening bond purchases in June; afternoon weekly purchase data showed a PEPP slowdown (but overall asset buying accelerated).

- DMO made some Jun-Sep qtly announcements ahead of May 17 consultation

- Tuesday sees sales of Dutch DSL and 2x UK Gilts, with Germany set to syndicate 30-Yr Green bund.

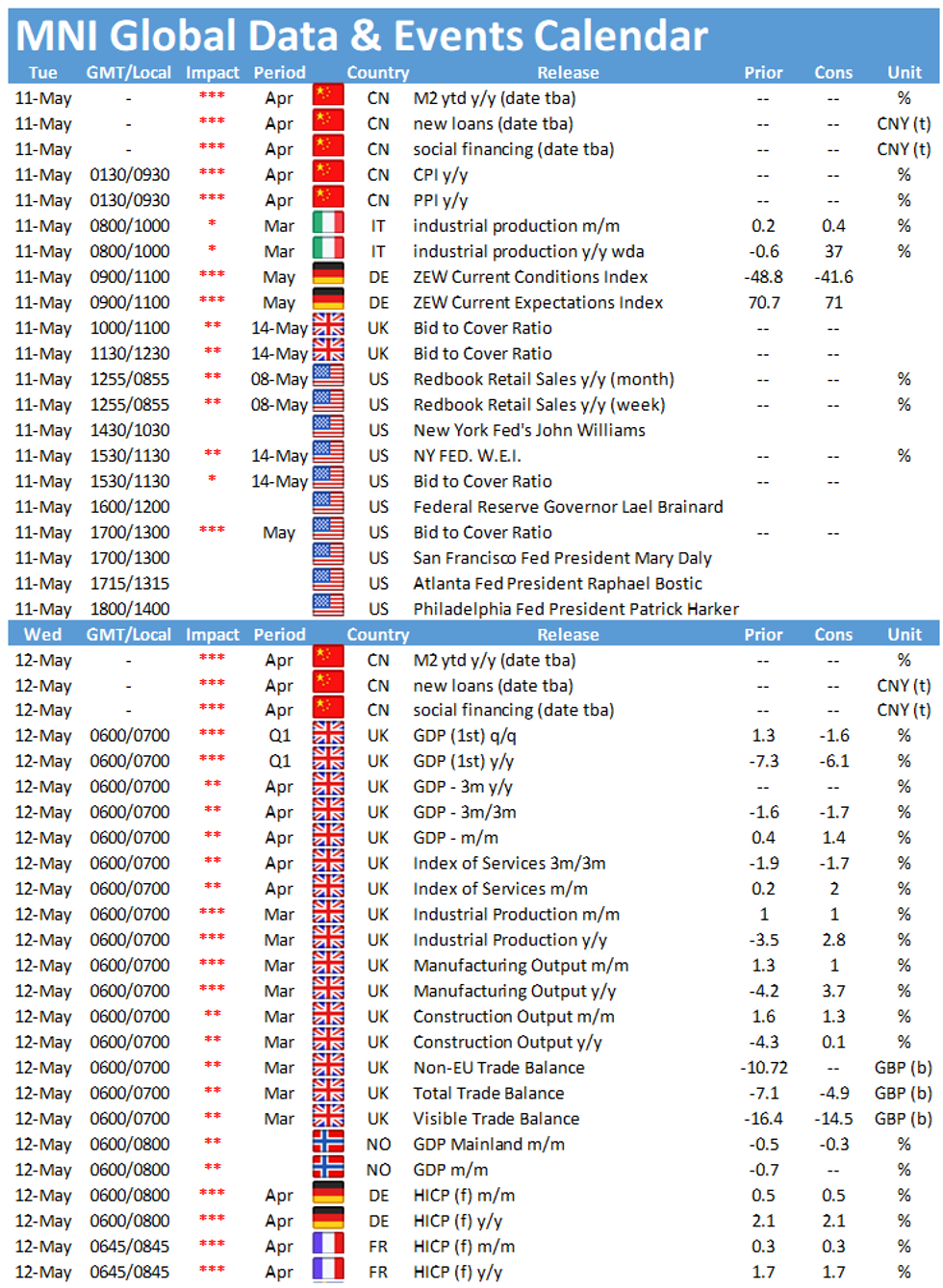

- We also hear from BoE's Bailey and ECB's Knot / de Cos, with some CPI (Netherlands) and IP (Italy) data, as well as German ZEW.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is unchanged at -0.686%, 5-Yr is down 0.4bps at -0.591%, 10-Yr is up 0.3bps at -0.212%, and 30-Yr is up 0.8bps at 0.359%.

- UK: The 2-Yr yield is up 0.5bps at 0.038%, 5-Yr is up 0.8bps at 0.321%, 10-Yr is up 1.3bps at 0.788%, and 30-Yr is up 1.5bps at 1.329%.

- Italian BTP spread down 4bps at 114bps / Spanish spread down 2.3bps at 67.9bps

EUROPE SUMMARY: Sizeable Sep Straddles (In Euribor)

Monday's options flow included:

- OEM1 134.5/134.25/134.00p fly, bought for 2.5 in 1k

- 2RZ1 100p, sold at 3.75 in 3k (ref 100.315)

- 2RH2 100.25^, bought for 28 in 1k

- 3RU1 100.12^ vs 99.87p, bought for 18.25 in 2k

- 3RU1 100.12^ vs 99.87p (v 16.5, 40d) WITH 2RU1 100.375^, buys the strip for 33 in 1.5k

- 3RZ1 100.125/99.875 put spread (v 100.12) bought for 8.75 in 5k

FOREX: GBP Consolidates Strong Rally Following 1.40 Breakout

- GBPUSD extended gains today to confirm a break of the 1.4000 handle, surging 1.2% to trade at 1.4150. Following the build up of a cluster of daily highs and constant rejection of the psychological level on a closing basis, GBPUSD shot higher on the open and never looked back.

- Contributing fundamental factors include:

- UK politics seeing the Tories make further inroads into traditional Labour strongholds

- Prime minister Johnson also confirmed that the next stage of re-opening will go as planned on the 17th, following last week's headline that two thirds of UK adults have received a first vaccination.

- A close above 1.4141 will represent the highest daily close since April 2018. The move higher negates the recent bearish focus and resumes a technical bullish theme with attention turning to 1.4237 High Feb 24 and a key resistance.

- USDCAD (-0.45%) continued its most recent descent, trading below 1.21 for the first time since September 2017.

- Elsewhere G10 currencies were confined to tighter ranges with the US dollar index retreating by just 0.1%. The Commodity complex sharply reversed lower during the US session, prompting AUD, NZD and EUR to all trade off their best levels, but the quick moves were unable to ignite any meaningful dollar strength.

FX OPTIONS: Expiries for May11 NY cut 1000ET (Source DTCC)

- EUR/USD: May13 $1.2100(E1.0bln), $1.2150-70(E2.4bln), $1.2235-50(E1.8bln)

- AUD/USD: May13 $0.7760-65(A$1.0bln), $0.7780-95(A$1.7bln)

EQUITIES: Fortunes Diverge, Tech Sags as Dow Jones Hits New Record

- Markets diverged sharply Monday, with tech and communication services names falling sharply while the Dow Jones extended recent outperformance to strike a new all time high. The e-mini NASDAQ fell close to 2%, with big name tech firms including Facebook, QUALCOMM, Tesla and Paypal off 3% or more.

- The index turned toward first support at last week's Tuesday/Thursday lows, which come in just ahead of the 50-dma at 13,365.

- Tech weakness occurred for a number of idiosyncratic reasons, with QUALCOMM hit following reports that Apple will bring modem production in-house, while Facebook and Alphabet slipped after downgrades at Citi.

- Perhaps unsurprisingly, the tech and comm services sectors were at the bottom of the pile for the S&P 500, while utilities and consumer staples made decent headway.

COMMODITIES: Punchy Open Before Profit-Taking Prompts Sluggish Trade

- Lumber rolled higher at the open to hit a new cycle high, further stoking market-wide inflation fears, before prices rolled over shortly following the open, with profit-taking knocking prices off by near 4%.

- This seemed to undercut the broader commodity complex as the likes of gold, silver, WTI and Brent crude futures followed suit to edge off recent highs in a move largely pinned on profit-taking and position-squaring ahead of key Fed speakers and US inflation releases this week.

- WTI and Brent crude futures came under pressure ahead of the close, before reports of warning shots fired at Iranian fast boats from US Coast Guard vessels helped stem the losses slightly.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok